LendingClub (LC): Assessing Valuation After Recent Shifts in Share Price Momentum

LendingClub Corp LC | 0.00 |

Over the past year, LendingClub's momentum has been choppy, with a recent 90-day share price return of 0.19% suggesting some renewed interest but not yet a solid upward trend. Despite these fluctuations, the 1-year total shareholder return of 0.34% points to only modest long-term gains.

If you’re looking to widen your search beyond LendingClub, now is a good time to discover fast growing stocks with high insider ownership.

LendingClub's current share price sits 22% below the average analyst target. This raises an important question for investors: Is the market overlooking potential upside, or has all anticipated growth already been priced in?

Most Popular Narrative: 16.6% Undervalued

LendingClub’s estimated fair value from the most widely followed narrative sits $2.98 above the last close price. This valuation gap is drawing attention, inviting discussion around strategic catalysts and future performance.

The hybrid digital marketplace/bank model continues to scale. Marketplace originations and balance sheet loans are growing in tandem, with the former providing high-margin, capital-light revenue and the latter building durable recurring net interest income. This dual engine offers operating leverage for sustained growth in earnings and tangible book value.

Want to know what’s fueling this price target? The real story is a mix of innovation, a clever business model, and a surprising twist in future profit margins. Discover the bold financial projections behind this valuation, and see what could set LendingClub apart from the crowd.

Result: Fair Value of $17.95 (UNDERVALUED)

However, increased competition and LendingClub’s reliance on personal loans could present challenges for future earnings growth and may put pressure on profit margins.

Another View: Multiples Suggest a Different Story

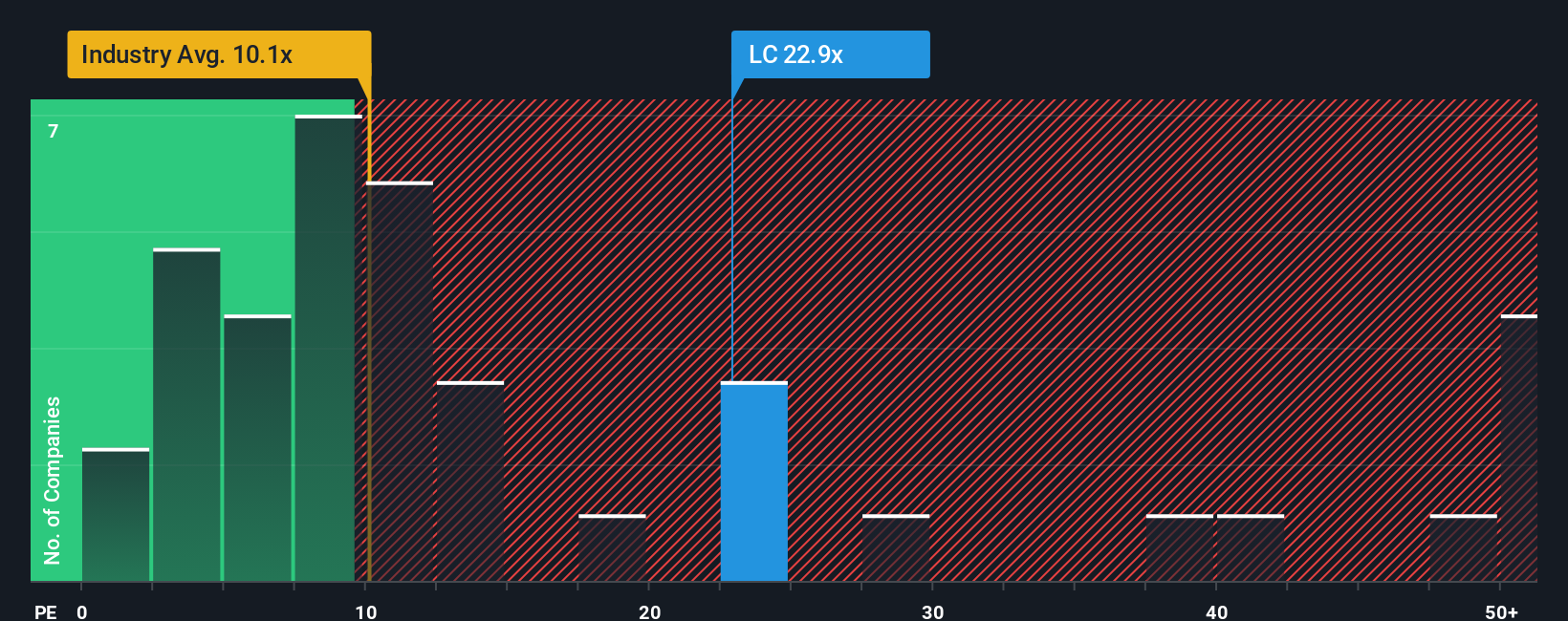

Looking at LendingClub through the lens of its price-to-earnings ratio, the situation shifts. The current ratio of 23.2x sits noticeably higher than both the industry average of 10x and the peer average of 6.4x, and it is also above the fair ratio of 21.3x. This higher multiple can signal optimism but also raises the risk that expectations for growth are already built into the share price. Are investors getting ahead of themselves, or is there more upside to be captured?

Build Your Own LendingClub Narrative

If LendingClub’s story looks different to you or you prefer to follow your own path, you can build a narrative yourself in just a few minutes, and truly make it yours. Do it your way.

A great starting point for your LendingClub research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Stop waiting on the sidelines. Spark your investing journey by checking what else is setting trends right now with these unique stock opportunities below.

- Capitalize on AI-driven disruption and get ahead of market shifts by checking out these 24 AI penny stocks that are boosting innovation in artificial intelligence and automation.

- Secure your financial future by considering these 19 dividend stocks with yields > 3% which offer reliable income streams and stability in volatile times.

- Position yourself for growth by evaluating these 900 undervalued stocks based on cash flows that are trading at compelling valuations based on strong cash flows and potential upside.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.