LendingClub (LC): Exploring Valuation After Recent Volatility and Long-Term Shareholder Gains

LendingClub Corp LC | 0.00 |

LendingClub’s share price has been fairly subdued this year, but long-term investors have seen a meaningful benefit, with a 1-year total shareholder return of roughly 33%. Recent momentum may be uneven. However, the broader outlook supports a cautious sense of optimism for investors keeping an eye on growth potential and shifting sentiment.

If you’re scanning for more stocks with compelling growth and insider conviction, it might be the perfect moment to broaden your horizons and discover fast growing stocks with high insider ownership

With LendingClub’s share price lagging behind analyst targets and strong long-term gains in its history, the question is whether the market is overlooking further upside, or if future growth is already reflected in today’s valuation?

Most Popular Narrative: 16.6% Undervalued

LendingClub's current price sits well below the most popular fair value estimate, drawing plenty of attention to the powerful growth elements driving this narrative. Major catalysts appear baked in, but the real story lies beneath headline figures.

The hybrid digital marketplace/bank model continues to scale. Marketplace originations and balance sheet loans are growing in tandem, with the former providing high-margin, capital-light revenue and the latter building durable recurring net interest income. This dual engine offers operating leverage for sustained growth in earnings and tangible book value.

Curious what bold assumptions make up this valuation? Analysts in the narrative are betting on a radical transformation in LendingClub's earnings power and an aggressive margin leap most wouldn't guess. Find out which future financial milestones unlock the target price and why they could rewrite the company's growth story.

Result: Fair Value of $17.95 (UNDERVALUED)

However, fierce competition and LendingClub’s continued reliance on personal loans could quickly challenge current profit expectations as well as the long-term growth narrative.

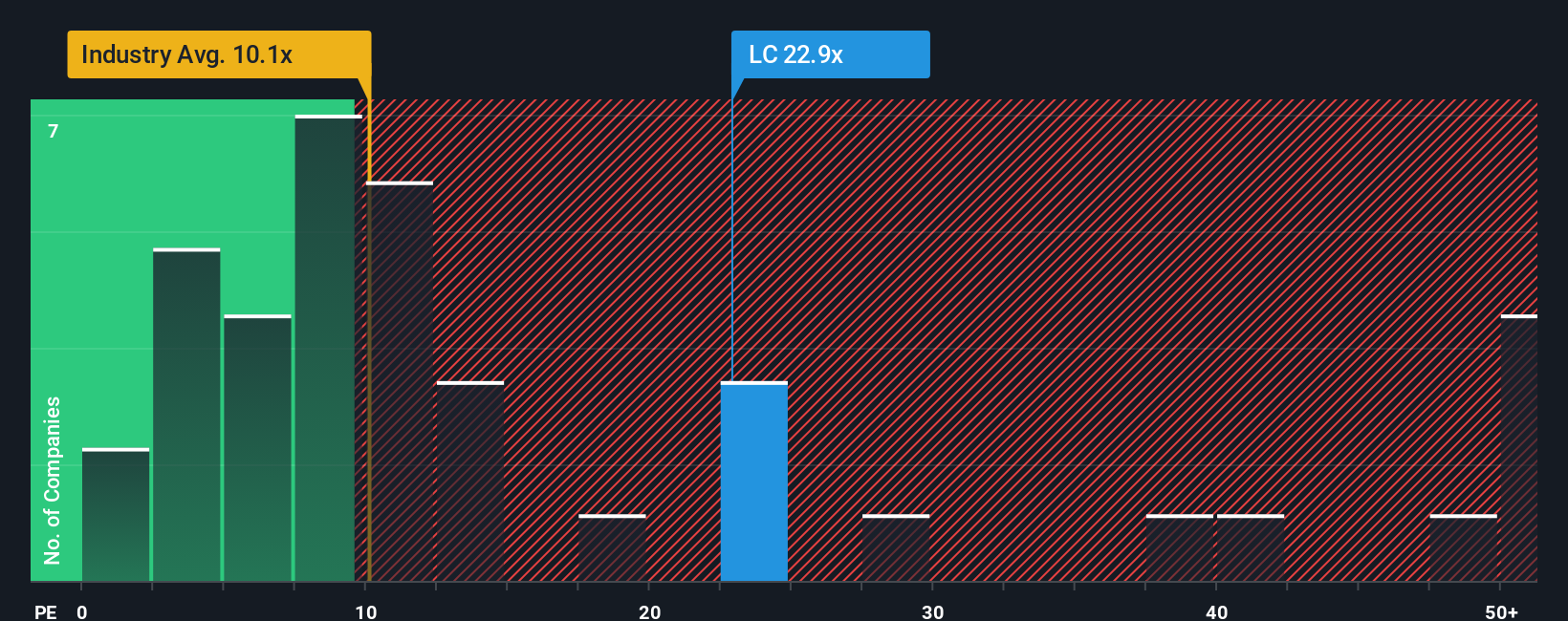

Another View: Market Ratios Send a Different Signal

Looking through the lens of the price-to-earnings ratio, LendingClub stands out as expensive compared to both industry peers and its own fair ratio. At 23.2 times earnings, the market is valuing the company much higher than the industry average of 10 times and above a fair ratio of 21.3 times. This suggests investors need more conviction in LendingClub’s future growth to justify the current premium. Could the optimism priced in set up future disappointment, or is the market right to look past near-term volatility?

Build Your Own LendingClub Narrative

If you see the story differently or want to dig into the numbers yourself, tap into the data and build your own perspective in just minutes with Do it your way

A great starting point for your LendingClub research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Opportunities?

Boost your research toolkit beyond LendingClub by tapping into powerful stock strategies others overlook. Don’t wait until the next trend passes you by. Get ahead with these three handpicked ideas:

- Uncover untapped potential by sizing up these 909 undervalued stocks based on cash flows with prices not yet reflecting their true worth, setting you up for possible outsized returns.

- Capitalize on income potential and grow your portfolio with these 19 dividend stocks with yields > 3% that deliver strong yields above 3% and proven reward strategies.

- Harness the explosive momentum of digital currencies and blockchain tech by reviewing these 78 cryptocurrency and blockchain stocks geared to shake up the financial world.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.