Lennar (LEN) Could Be 6% Undervalued As New Communities Expand Its Reach

Lennar Corporation Class A LEN | 0.00 |

Lennar (LEN) has just outlined two new communities that expand its reach on both coasts: The Towns at West End in Lancaster City, Pennsylvania, and Manhattan Square in Carson, California, drawing fresh attention to the stock.

Despite these new communities drawing interest, Lennar's recent share price performance has been weak. The stock closed at US$82.84 and recorded a year to date share price decline of 20.51%, alongside a 1 year total shareholder return decline of 25.14%.

If Lennar's expansion has you thinking about where housing related demand might intersect with infrastructure needs, this could be a good moment to scan 34 power grid technology and infrastructure stocks

Lennar is rolling out new communities on both coasts while the stock trades well below recent levels. The key question for investors is whether it makes more sense to enter a position now, or wait for a potentially lower price as the valuation picture becomes clearer.

Most Popular Narrative: 6.4% Undervalued

Based on the most followed narrative, Lennar's fair value of $88.54 sits a little above the last close at $82.84. This frames the current pullback as a valuation gap rather than a pricing outlier.

The acquisition of Rausch Coleman and the expansion into new markets are expected to increase Lennar's market share and facilitate growth in community count and volume, positioning the company for future revenue growth as market conditions stabilize or improve.

Read the complete narrative. Read the complete narrative.

Want to see what is baked into that higher fair value for Lennar? Revenue stepping up, margins adjusting, and a future earnings multiple that assumes disciplined capital returns and an asset light land model working as intended. The full narrative explains how those moving parts are modeled against a higher discount rate and softer recent performance, and which assumptions matter most for that $88.54 figure.

Result: Fair Value of $88.54 (UNDERVALUED)

However, that fair value story for Lennar can quickly look different if higher mortgage rates persist or if land banking costs put more pressure on margins and cash flow.

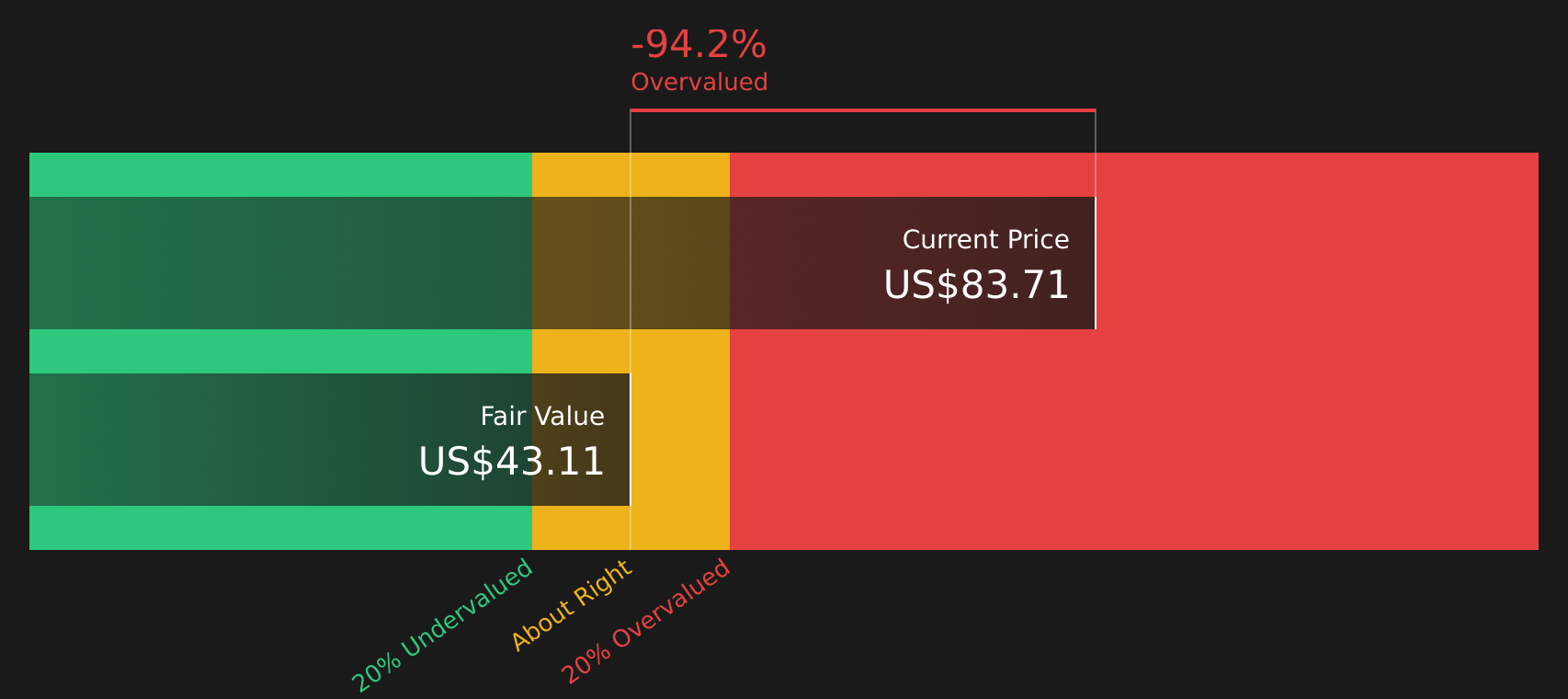

Another View: Lennar Through A Cash Flow Lens

The consensus narrative frames Lennar as about 6.4% undervalued at $88.54 based on earnings. However, the SWS DCF model using future cash flows points in the opposite direction, with an estimate of $43.15 per share, indicating the stock is trading well above that level and could be overvalued on this measure. Which story do you think better matches how Lennar actually converts its land light model into cash over time?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Lennar for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Seeing mixed signals around Lennar and not sure how to weigh them? Move quickly to review the full picture of potential risks and upsides with 3 key rewards and 1 important warning sign

Looking for more ideas beyond Lennar?

If Lennar has sharpened your focus on where to put fresh capital, this is a smart time to widen the lens and line up a few more opportunities.

- Target stability first by checking stocks in the 80 resilient stocks with low risk scores that may suit a more defensive corner of your portfolio.

- Spot potential value by scanning the 46 high quality undervalued stocks and see which companies currently trade below their assessed worth on key fundamentals.

- Get ahead of the crowd by reviewing the screener containing 20 high quality undiscovered gems before others start paying closer attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.