Lexicon Pharmaceuticals, Inc.'s (NASDAQ:LXRX) Shares Climb 28% But Its Business Is Yet to Catch Up

Lexicon Pharmaceuticals, Inc. LXRX | 0.00 |

Lexicon Pharmaceuticals, Inc. (NASDAQ:LXRX) shares have had a really impressive month, gaining 28% after a shaky period beforehand. The last 30 days bring the annual gain to a very sharp 86%.

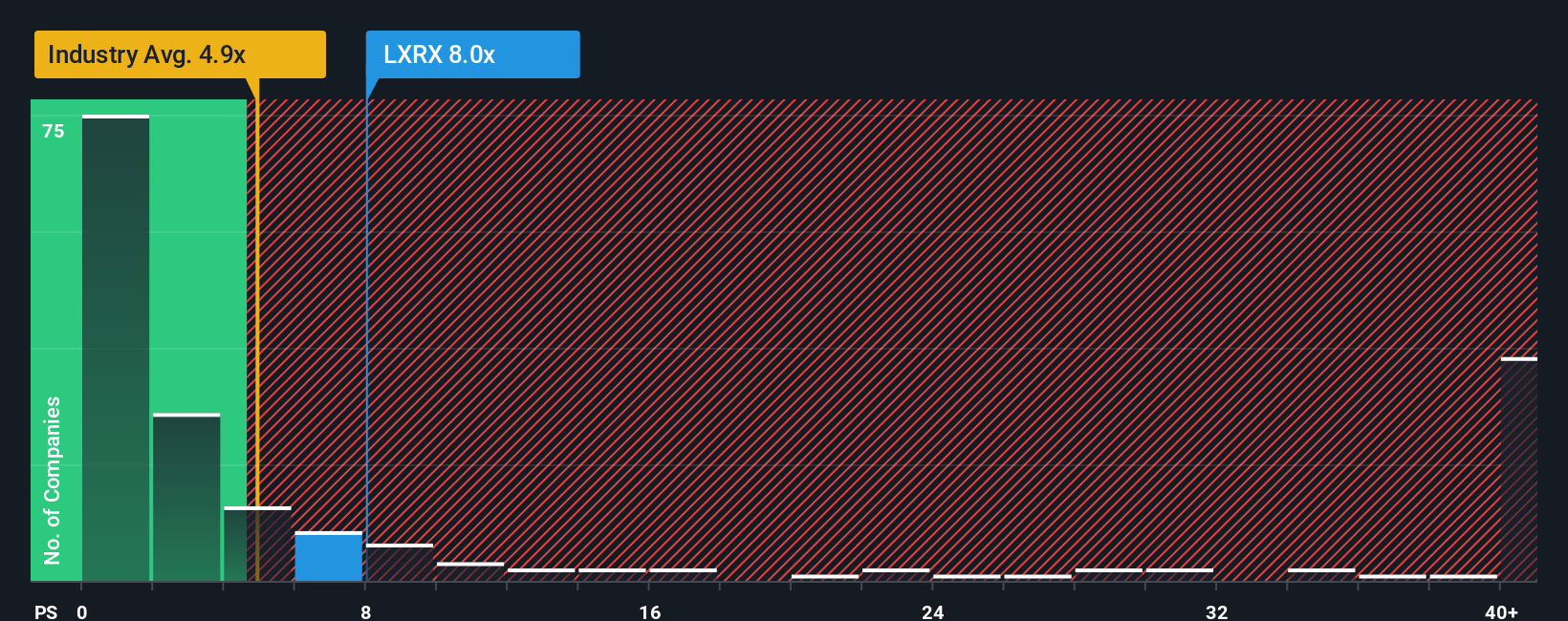

After such a large jump in price, Lexicon Pharmaceuticals may be sending strong sell signals at present with a price-to-sales (or "P/S") ratio of 8x, when you consider almost half of the companies in the Pharmaceuticals industry in the United States have P/S ratios under 5x and even P/S lower than 1.2x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

How Lexicon Pharmaceuticals Has Been Performing

Lexicon Pharmaceuticals certainly has been doing a good job lately as it's been growing revenue more than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Keen to find out how analysts think Lexicon Pharmaceuticals' future stacks up against the industry? In that case, our free report is a great place to start.What Are Revenue Growth Metrics Telling Us About The High P/S?

The only time you'd be truly comfortable seeing a P/S as steep as Lexicon Pharmaceuticals' is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered an explosive gain to the company's top line. The amazing performance means it was also able to deliver huge revenue growth over the last three years. Accordingly, shareholders would have been over the moon with those medium-term rates of revenue growth.

Turning to the outlook, the next three years should bring diminished returns, with revenue decreasing 11% per annum as estimated by the five analysts watching the company. With the industry predicted to deliver 33% growth per year, that's a disappointing outcome.

In light of this, it's alarming that Lexicon Pharmaceuticals' P/S sits above the majority of other companies. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as these declining revenues are likely to weigh heavily on the share price eventually.

The Final Word

Shares in Lexicon Pharmaceuticals have seen a strong upwards swing lately, which has really helped boost its P/S figure. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that Lexicon Pharmaceuticals currently trades on a much higher than expected P/S for a company whose revenues are forecast to decline. Right now we aren't comfortable with the high P/S as the predicted future revenue decline likely to impact the positive sentiment that's propping up the P/S. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

You should always think about risks.

If these risks are making you reconsider your opinion on Lexicon Pharmaceuticals, explore our interactive list of high quality stocks to get an idea of what else is out there.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.