Lexicon Pharmaceuticals (LXRX) Joins Russell Indexes, Is The Stock Still A Bargain?

Lexicon Pharmaceuticals, Inc. LXRX | 0.00 |

Index additions put Lexicon Pharmaceuticals in focus

Lexicon Pharmaceuticals (LXRX) has just been added to multiple Russell indexes and growth benchmarks, a move that can influence trading activity as index tracking funds adjust their portfolios.

This wave of index inclusions places Lexicon Pharmaceuticals on the radar of a broader set of institutional and retail investors. For you, the key question is how this new exposure interacts with the company’s fundamentals and recent share price performance.

The index additions come after a period of strong share price momentum for Lexicon Pharmaceuticals, with the stock delivering a 69.23% 3 month share price return and a 131.58% year to date share price return. The 1 year total shareholder return stands at 179.16%, set against a more modest 13.79% total shareholder return over three years and a decline of 35.92% over five years.

If this kind of index driven move has caught your attention, it can be a good time to scan the wider market for similar opportunities using the 41 healthcare AI stocks

With Lexicon Pharmaceuticals now sitting in multiple Russell indexes, recent gains and analyst targets raise a sharp question for you: Is the stock still undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 30% Undervalued

At a last close of $2.64 versus a fair value narrative of $3.77, the current Lexicon Pharmaceuticals share price sits below what this widely followed storyline assumes.

Lexicon Pharmaceuticals is focused on advancing its pipeline of novel medicines, including progressing pilavapadin into pivotal trials as a first novel oral non-opioid treatment for diabetic peripheral neuropathic pain in over two decades. This development could significantly impact future revenue growth and market share. The company is developing LX9851, a first-in-class oral ACSL5 inhibitor for obesity and related cardiometabolic disorders, with promising preclinical data. This program could open new revenue streams and target high-demand markets once the IND is submitted in 2025.

Want to understand why this narrative sees room above today’s price? It leans heavily on future revenue expansion, margin improvement, and a bold earnings multiple. The exact mix of assumptions might surprise you.

Result: Fair Value of $3.77 (UNDERVALUED)

However, this Lexicon Pharmaceuticals narrative still leans on uncertain milestones, including dependence on partners like Novo Nordisk and higher R&D spend that could weigh on losses.

Another view on Lexicon Pharmaceuticals valuation

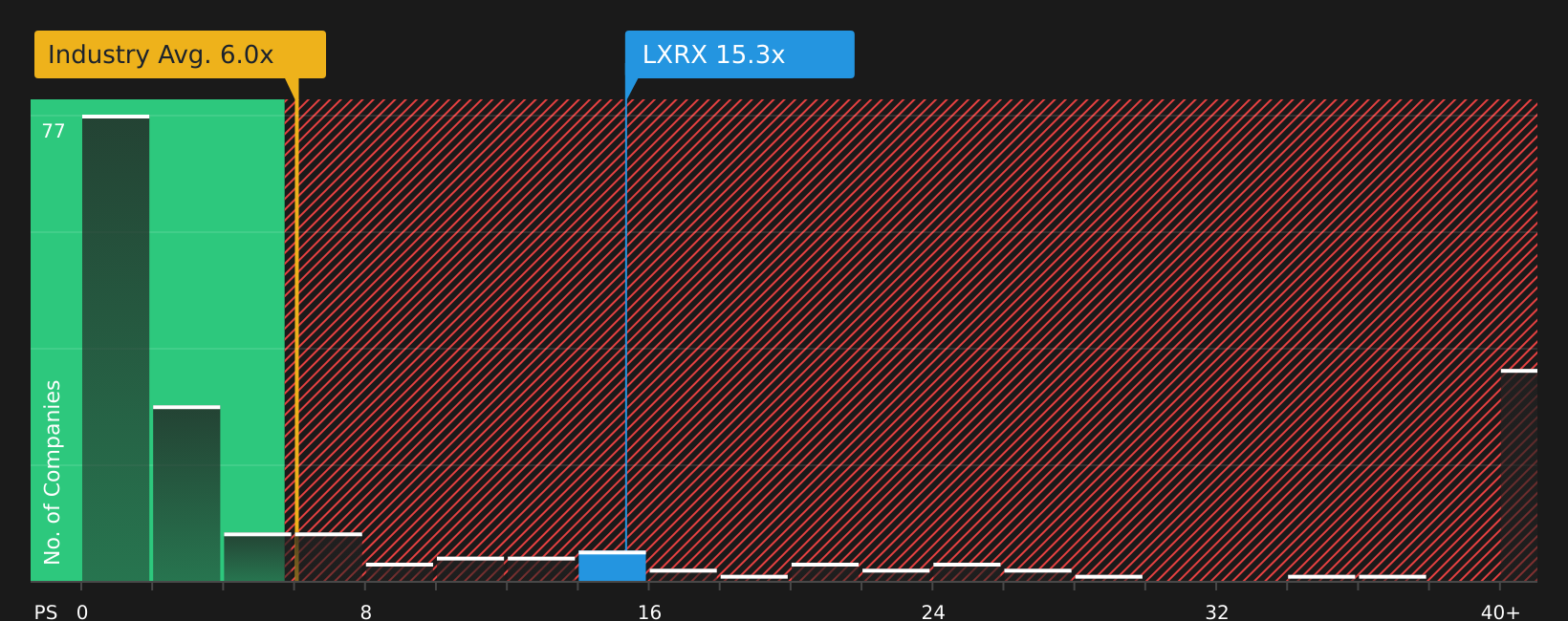

That fair value narrative presents Lexicon Pharmaceuticals as 30% undervalued at $3.77, but the current P/S ratio of 16.8x tells a different story. It is far above the US pharmaceuticals average of 5.8x and the fair ratio of 7.9x. This points to meaningful valuation risk if sentiment cools.

Before relying on that higher fair value, it is worth asking whether the stock’s elevated sales multiple leaves you with much room for error or mainly downside if expectations are not met.

Next Steps

With sentiment on Lexicon Pharmaceuticals pulled between optimism and caution, it makes sense to move quickly, explore the underlying data yourself, and weigh both sides of the story, including the 1 key reward and 2 important warning signs

Looking for more investment ideas beyond Lexicon Pharmaceuticals?

If Lexicon Pharmaceuticals has sharpened your focus, do not stop here. Broaden your watchlist now so fresh opportunities do not quietly pass you by.

- Target higher potential by scanning screener containing 19 high quality undiscovered gems that pair strong fundamentals with businesses many investors are still overlooking.

- Strengthen your downside protection by reviewing 72 resilient stocks with low risk scores that score well on resilience and risk controls.

- Focus on quality and staying power by checking the solid balance sheet and fundamentals stocks screener (48 results) for companies with financial structures built to handle setbacks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.