LG Patent Deal And 2026 Outlook Might Change The Case For Investing In InterDigital (IDCC)

InterDigital, Inc. IDCC | 0.00 |

- In February 2026, InterDigital reported past fourth-quarter 2025 results showing sales of US$158.23 million and net income of US$42.97 million, alongside full-year 2025 sales of US$834.02 million and net income of US$406.64 million, and issued first-quarter 2026 guidance for revenue of US$194–US$200 million and diluted EPS of US$1.61–US$1.86.

- A recent patent license agreement with LG Electronics, covering digital TVs, display monitors and advanced technologies, broadens InterDigital’s licensing reach beyond smartphones and could diversify its royalty income sources.

- With the company pairing a new LG patent deal and detailed first-quarter 2026 guidance, we'll examine how this reshapes InterDigital's investment narrative.

We've uncovered the 15 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

What Is InterDigital's Investment Narrative?

To own InterDigital, you really have to believe in the durability of its patent licensing model and the company’s ability to keep signing and renewing deals with big-name electronics makers. The new LG agreement fits neatly into that story, reinforcing the idea that InterDigital’s portfolio matters not just for smartphones but for TVs, monitors and other connected devices. Coupled with detailed first quarter 2026 guidance, the latest update gives a clearer near term line of sight on revenue and earnings after a softer fourth quarter, which may ease some concerns around lumpiness in licensing income. At the same time, full year 2026 guidance points to lower profit than 2025, so concentration in a handful of large licensees and the inherent volatility of deal timing remain key risks to watch.

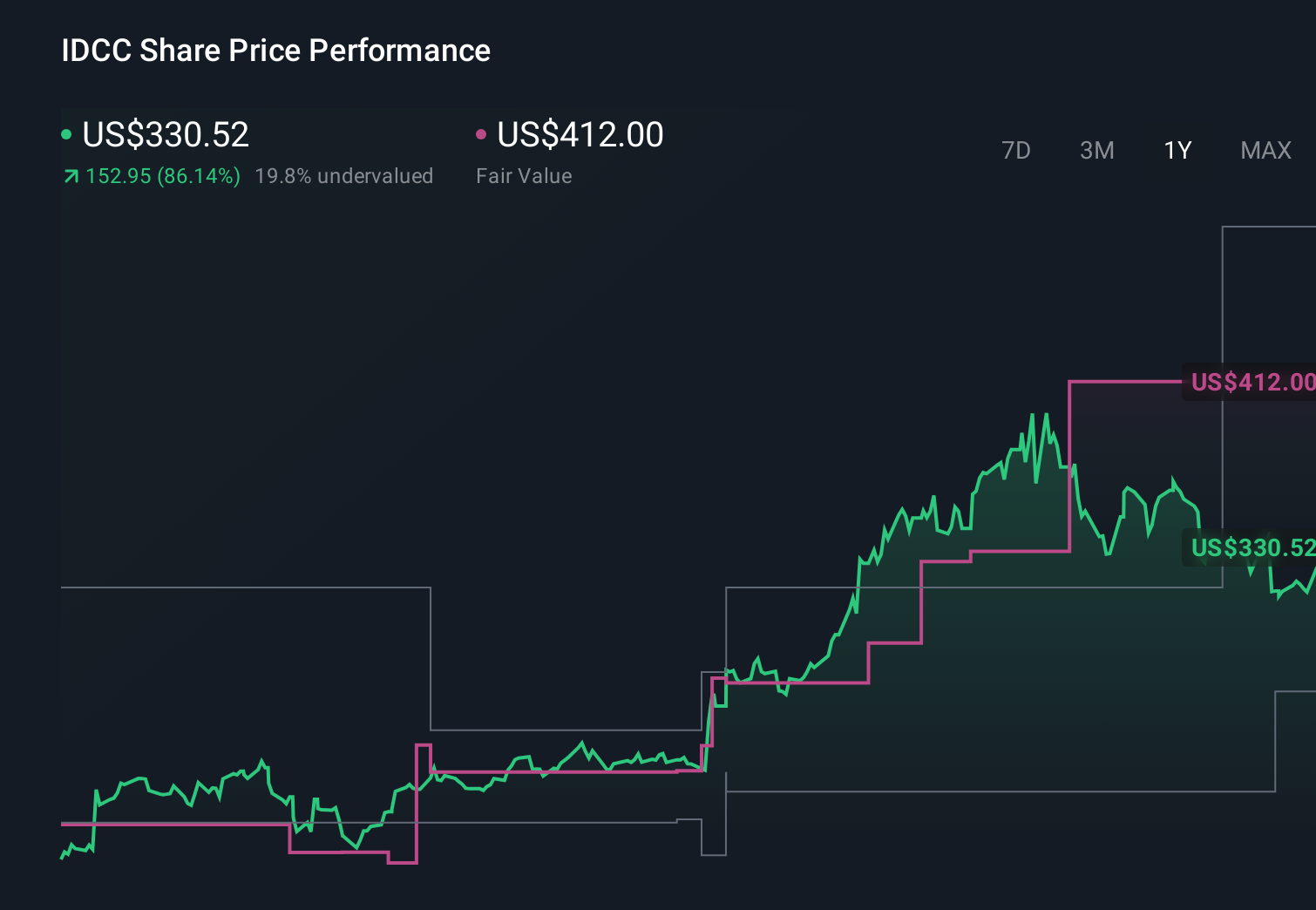

However, one risk in particular could catch new shareholders off-guard. InterDigital's shares are on the way up, but could they be overextended? Uncover how much higher they are than fair value.Exploring Other Perspectives

Explore 5 other fair value estimates on InterDigital - why the stock might be worth less than half the current price!

Build Your Own InterDigital Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your InterDigital research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free InterDigital research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate InterDigital's overall financial health at a glance.

Interested In Other Possibilities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 55 companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.