Li Auto (LI) Is Down 6.7% After Recall and Supply Pact News Is Management’s Strategy on Track?

LI Auto LI | 18.41 | +3.28% |

- Earlier in November 2025, Li Auto recalled its Mega MPV after a coolant leakage issue led to a vehicle fire and implemented employee terminations and penalties for those accountable, while also addressing other mass quality incidents across newer models.

- An exclusive new supply agreement with Hesai Technology for LiDAR in future vehicles signals Li Auto’s continued commitment to advanced driver assistance and vehicle technology innovation even while managing operational setbacks.

- Let’s examine how Li Auto’s strong response to safety and quality issues affects its broader investment narrative and future growth outlook.

These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Li Auto Investment Narrative Recap

To own Li Auto stock, an investor must believe in the company’s ability to drive electric vehicle innovation and regain consumer trust as it shifts from EREV to BEV models. The recent Mega MPV recall highlights execution risk, but does not materially affect the most important short-term catalyst: successful launches and deliveries of new BEV models such as the Li i6 and Li i8. However, it does bring renewed focus to process discipline and cost management, especially as the company contends with margin pressures and intensifying competition.

Of recent announcements, the exclusive agreement with Hesai Technology for LiDAR supply stands out in connection with the recall. This partnership could reinforce Li Auto’s commitment to technological advancement, a critical factor as the company attempts to differentiate its lineup and support recurring software revenue despite short-term quality setbacks. The combination of advanced driver assistance features and high-quality manufacturing remains central to Li Auto’s growth narrative.

But while some rivals have pushed forward, investors should be aware of intensifying price wars and thinner margins...

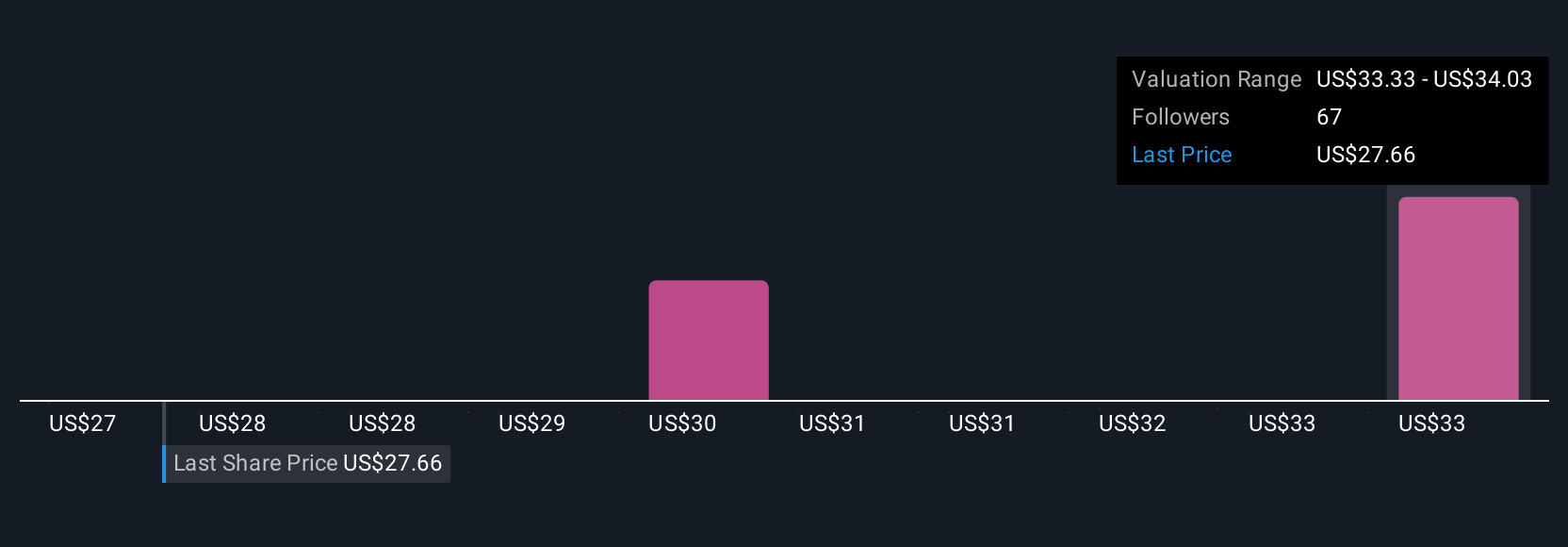

Li Auto's narrative projects CN¥232.1 billion revenue and CN¥15.2 billion earnings by 2028. This requires 17.4% yearly revenue growth and an earnings increase of CN¥7.1 billion from CN¥8.1 billion currently.

Uncover how Li Auto's forecasts yield a $28.70 fair value, a 52% upside to its current price.

Exploring Other Perspectives

Five fair value estimates from the Simply Wall St Community cluster between CN¥27.33 and CN¥35.15 per share, all above current trading levels. Yet, with recent product recalls and accountability measures raising execution risk, investor opinions on Li Auto’s future performance remain divided, explore multiple viewpoints here.

Explore 5 other fair value estimates on Li Auto - why the stock might be worth just $27.33!

Build Your Own Li Auto Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Li Auto research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Li Auto research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Li Auto's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 27 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 38 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.