Lithia Motors (LAD) Same Store Sales Growth Supports Bullish Earnings Momentum Narratives

Lithia Motors, Inc. LAD | 251.82 | +0.40% |

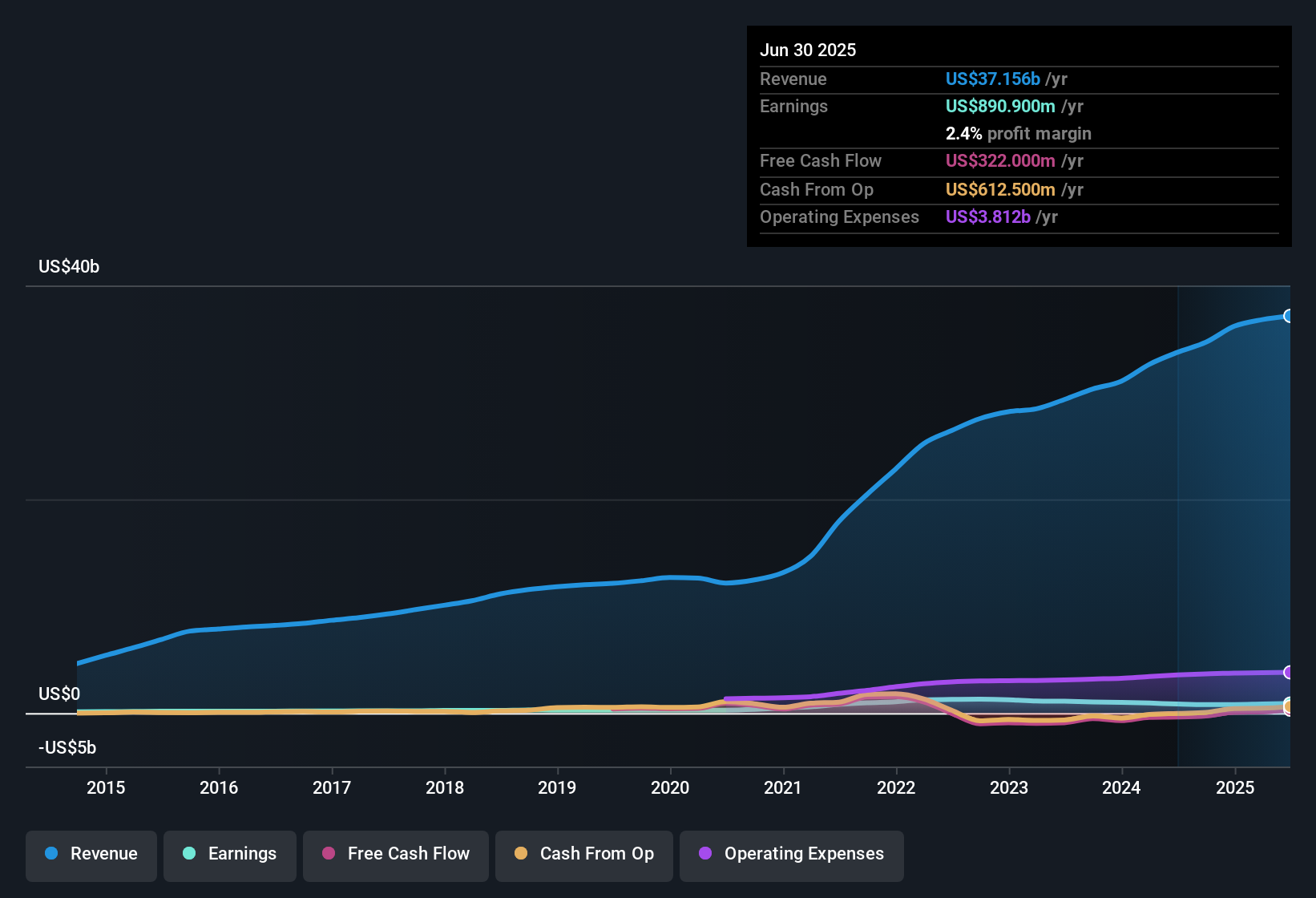

Lithia Motors (LAD) has put up another busy quarter, with Q3 FY 2025 revenue at about US$9.7b, basic EPS of US$8.62 and net income of US$217.1m, alongside same store sales growth of 7.7%. The company has seen quarterly revenue move from US$9.2b in Q3 FY 2024 to US$9.7b in Q3 FY 2025, while basic EPS shifted from US$7.76 to US$8.62 over the same span. This sets the stage for investors to weigh higher sales and earnings against how much of that is flowing through to margins.

See our full analysis for Lithia Motors.With the headline numbers on the table, the next step is to see how they line up with the widely followed stories around Lithia Motors, and where those narratives may need an update.

Margins Steady Around 2.4% Net Profit

- Over the last 12 months, Lithia earned US$900.7 million on US$37.6b of revenue, which works out to a 2.4% net profit margin compared with 2.3% the prior year.

- Consensus narrative talks up higher margin potential from aftersales, finance and technology, yet the latest trailing numbers still sit close to that 2.4% level. This suggests:

- Aftersales already contributes more than 60% of net profit in the bullish and consensus stories, but the reported margin is only slightly above last year, so investors may want to see more pronounced improvement before assuming big margin expansion is playing out.

- Analysts are looking for margins to move toward about 2.6% over the next few years, so the current 2.4% gives them a base, but it also means a fair amount of the margin uplift is still ahead rather than visible in the trailing figures.

Earnings Growth vs 0.3% Five Year Trend

- Earnings grew 12.9% over the last year, compared with a 0.3% annualized earnings growth rate over five years, so the recent pace is much stronger than the longer term record.

- Bulls argue that high margin aftersales and digital platforms can support stronger, more consistent earnings, and the recent 12.9% growth gives them some support, but it also raises questions:

- The bullish view expects earnings to keep growing at around 15.4% a year, which is not far from the 12.9% just reported, yet the much lower 0.3% five year trend shows that kind of pace has not been typical historically.

- For long term holders, that gap between recent and five year growth may be a reason to ask whether the latest year reflects a durable shift from aftersales and finance or a period that could look different from the longer run.

Cheap P/E With Debt Coverage Risk

- Lithia trades on a trailing P/E of 8.6x at a share price of US$320.41, compared with peer and US Specialty Retail industry averages of 23.5x and 20.4x, and a DCF fair value of about US$724.93 per share.

- Bears focus on balance sheet pressure and slower revenue growth, and the data gives them some clear talking points alongside the low P/E:

- Debt is described as not well covered by operating cash flow over the last 12 months, so even though valuation looks low and a DCF fair value far above the current price is shown, the cash coverage flag keeps attention on how easily the company can service and reduce its borrowings.

- Revenue is forecast to grow around 3.5% a year, below the 10.4% cited for the US market, which fits the bearish concern that organic growth could lag and helps explain why some investors might not be willing to pay peer level multiples despite the discount to both the DCF fair value and the analyst price target of about US$396.71.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Lithia Motors on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? Take a couple of minutes to test your own view against the data, shape it into a clear story and Do it your way

A great starting point for your Lithia Motors research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

Lithia Motors combines a relatively low P/E with modest net margins around 2.4%, balance sheet pressure and revenue growth expectations below the broader US market.

If that mix of thin margins and debt coverage questions leaves you cautious, it could be worth checking out solid balance sheet and fundamentals stocks screener (45 results) that aim to pair earnings power with stronger financial footing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.