Lockheed Martin (LMT) Valuation Check After Raised 2026 Outlook And Expanded Interceptor Production Deals

Lockheed Martin Corporation LMT | 622.79 | +0.83% |

Lockheed Martin (LMT) just combined a strong fourth quarter, a higher 2026 outlook for sales and profit, and major interceptor production agreements into one dense batch of information for investors.

The 26.4% year to date share price return, including a 26.4% 1 month share price return and 32.8% 3 month share price return, suggests strong momentum. The 42.6% 1 year total shareholder return and 110.6% 5 year total shareholder return indicate that recent enthusiasm builds on longer term gains.

If this aerospace and defense story has your attention, it could be a useful moment to see what else is on the radar across aerospace and defense stocks.

Fast-rising earnings guidance, record backlog and interceptor orders, and a share price now sitting just below the latest analyst targets raise a key question: Is Lockheed Martin still mispriced, or is the market already banking on future growth?

Most Popular Narrative: 10.3% Overvalued

Compared with the narrative fair value of $569.68, Lockheed Martin's last close at $628.26 sits above that mark, which is where the tension in this story starts.

The growing focus on homeland defense initiatives such as "Golden Dome," missile warning networks, and increased munitions spending suggests future secular increases in U.S. defense budgets and multi-year, high-value contract awards that are likely to contribute meaningfully to backlog, revenue visibility, and cash flow stability.

Want to see what kind of revenue path and profit profile those contracts are expected to build in, and how that feeds into a richer earnings multiple and higher fair value over time, without relying on any single headline program? The full narrative lays out that financial blueprint in detail.

Result: Fair Value of $569.68 (OVERVALUED)

However, there is still real risk that large fixed price program charges or a US$4.6b tax dispute outcome could unsettle earnings expectations and confidence in the current setup.

Another View: Earnings Multiple Says “Good Value”

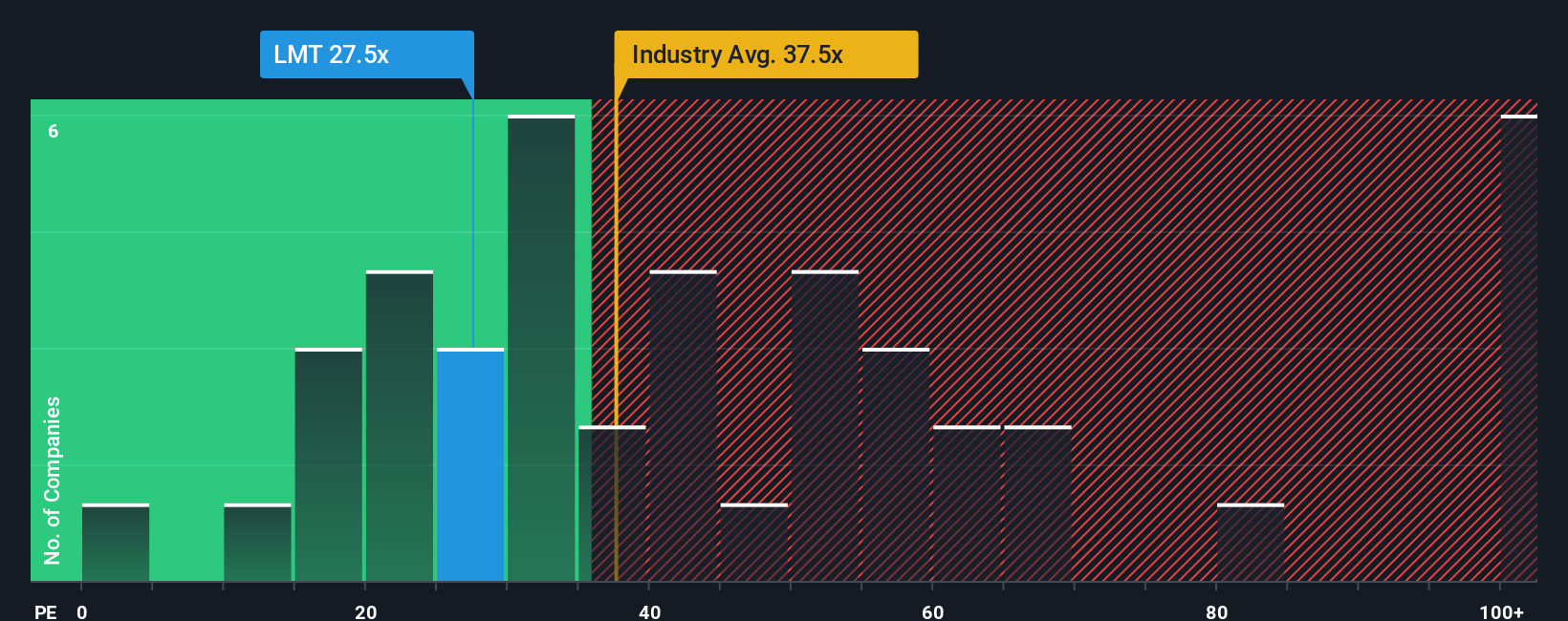

While the SWS narrative fair value marks Lockheed Martin as 10.3% overvalued, its P/E of 28.8x sits well below the US Aerospace & Defense average of 40.7x, the peer average of 36.6x, and a fair ratio of 35.9x. This points to valuation support instead of excess. With those gaps in mind, is the market underestimating the risk in the story or the potential reward if sentiment shifts?

Build Your Own Lockheed Martin Narrative

If this perspective does not fully reflect your view, or if you prefer to work from your own numbers and assumptions, you can build a personalised view in minutes with Do it your way.

A great starting point for your Lockheed Martin research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at one company story. Use the screener to spot where your next edge could come from.

- Spot potential value gaps by checking out these 867 undervalued stocks based on cash flows that might be pricing in less optimism than their cash flows suggest.

- Ride secular technology shifts by scanning these 25 AI penny stocks that are tied to real revenue and product traction, not just headlines.

- Build a cash flow focused income stream by searching through these 13 dividend stocks with yields > 3% that already offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.