Lucid Group Faces Cash Squeeze As Investors Question Long Term Outlook

Lucid LCID | 8.80 | -4.76% |

- Lucid Group is under growing financial pressure as cash reserves tighten and costs remain high.

- Recent high profile share sales by major holders have added to concerns over long term viability.

- The loss of the US EV tax credit has removed a key sales incentive for Lucid vehicles.

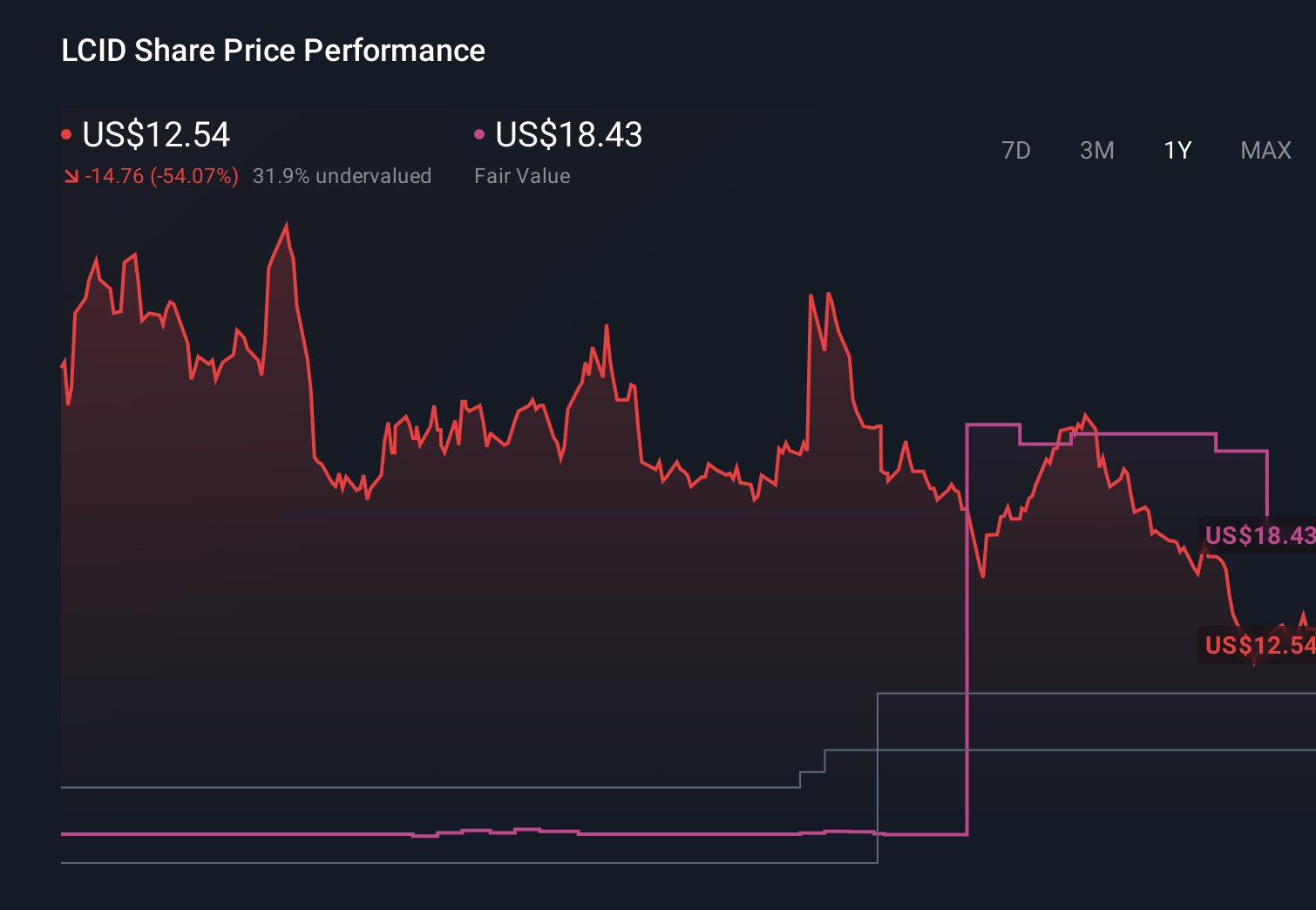

Lucid Group, trading on NasdaqGS:LCID, is in the spotlight as investors weigh rising financial strain against a share price of $10.38. The stock has fallen 64.3% over the past year and 91.0% over three years, with a 96.8% decline over five years, reflecting persistent concern about the business. Recent reports of weaker cash reserves and sustained quarterly losses are sharpening questions about how the company funds operations from here.

For you as an investor, the recent pullback of 4.9% over the past week and 11.2% over the past month sits on top of those longer term declines. These moves already point to a challenging story. With US EV tax credits no longer supporting Lucid's pricing and demand, the key issues to watch now are its funding options, cost base, and any signs that its sales trajectory is stabilizing or weakening further.

Stay updated on the most important news stories for Lucid Group by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Lucid Group.

Quick Assessment

- ✅ Price vs Analyst Target: At $10.38 versus a consensus target of $17.06, the price sits about 39% below where analysts, on average, have it.

- ⚖️ Simply Wall St Valuation: The valuation status is currently unknown, so you do not have a clear under or overvaluation signal here.

- ❌ Recent Momentum: The 30 day return of roughly 11% decline points to weak short term sentiment.

Check out Simply Wall St's in depth valuation analysis for Lucid Group.

Key Considerations

- 📊 The funding strain, weaker cash position, and insider selling all raise the bar for confidence in the long term equity story at the current price.

- 📊 Keep an eye on cash runway, any capital raises, revenue trends from the US and other markets, and how Lucid adjusts costs without choking growth.

- ⚠️ The clearest risk is the less than one year cash runway, which could mean further dilution or pressure on the balance sheet if conditions do not improve.

Dig Deeper

For the full picture including more risks and rewards, check out the complete Lucid Group analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.