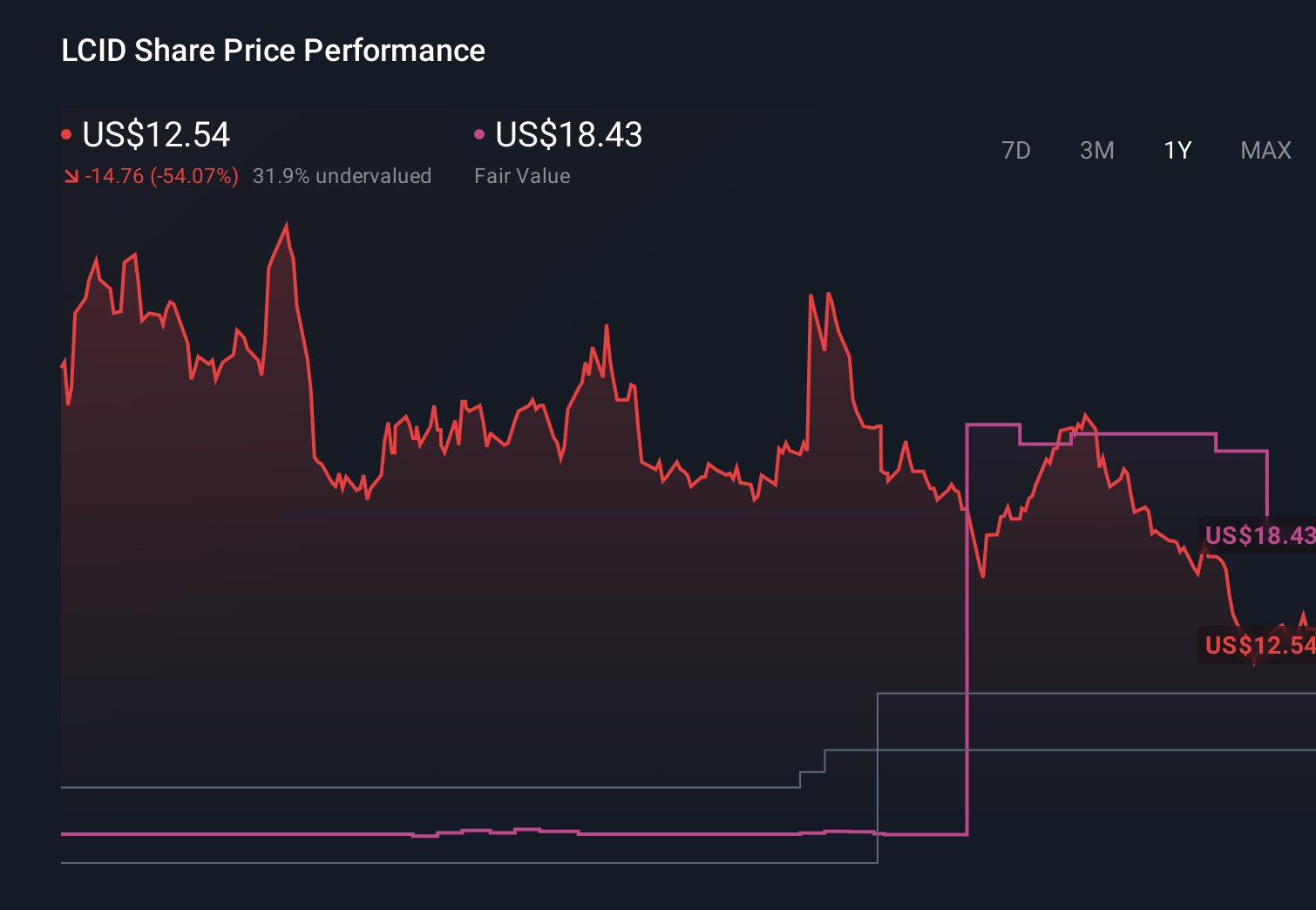

Lucid Group (LCID) Is Down 15.8% After New CEO, Expanded Uber Robotaxi Deal And Fresh Funding - What's Changed

Lucid LCID | 0.00 |

- In April 2026, Lucid Group announced Silvio Napoli as its next CEO, expanded its Uber partnership to at least 35,000 dedicated robotaxi vehicles, and bolstered liquidity with about US$1.05 billion in new equity and preferred financing from Uber and existing backer Ayar Third Investment Company.

- This combination of fresh leadership, deeper exposure to Uber’s planned global robotaxi network, and strengthened funding support could reshape how investors view Lucid’s ability to pursue its software-defined EV and fleet platform ambitions.

- We’ll now examine how the expanded Uber robotaxi commitment and fresh capital impact Lucid’s existing investment narrative and risk profile.

Outshine the giants: these 19 early-stage AI stocks could fund your retirement.

Lucid Group Investment Narrative Recap

To own Lucid today, you have to believe its software-focused EV and fleet platform can eventually turn heavy losses and dilution into a sustainable business, with the Uber robotaxi ramp as the key nearer term proof point. The expanded Uber commitment and fresh US$1.05 billion funding help the liquidity and demand story, but they also highlight the biggest current risk: Lucid’s dependence on ongoing external capital while gross margins remain deeply negative.

Among the recent announcements, the expanded Uber agreement for at least 35,000 dedicated Lucid robotaxi vehicles looks most relevant. It reinforces the earlier 20,000 vehicle plan and ties directly into Lucid’s ambition to monetize software-defined vehicles and high volume fleet sales. For investors focused on catalysts, this Uber pipeline sits on the other side of the same coin as the main risk: whether Lucid can fund and execute that ramp without eroding existing shareholders through further dilution.

Yet beneath the headline new funds and Uber volume, investors should be aware of Lucid’s continued reliance on fresh capital and...

Lucid Group's narrative projects $5.6 billion revenue and $285.8 million earnings by 2028.

Uncover how Lucid Group's forecasts yield a $16.67 fair value, a 141% upside to its current price.

Exploring Other Perspectives

Before this news, the most bearish analysts assumed revenue could still grow about 47% a year while warning that ongoing cash burn and dilution might block any path to profitability, so it is worth asking how the Uber deal and new financing could either ease or reinforce that much more cautious view.

Explore 6 other fair value estimates on Lucid Group - why the stock might be worth just $7.50!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Lucid Group research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Lucid Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lucid Group's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 61 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.