lululemon athletica (LULU) Is Down 11.0% After Outlook Cut And Founder Deal - Has The Bull Case Changed?

lululemon athletica inc. LULU | 0.00 |

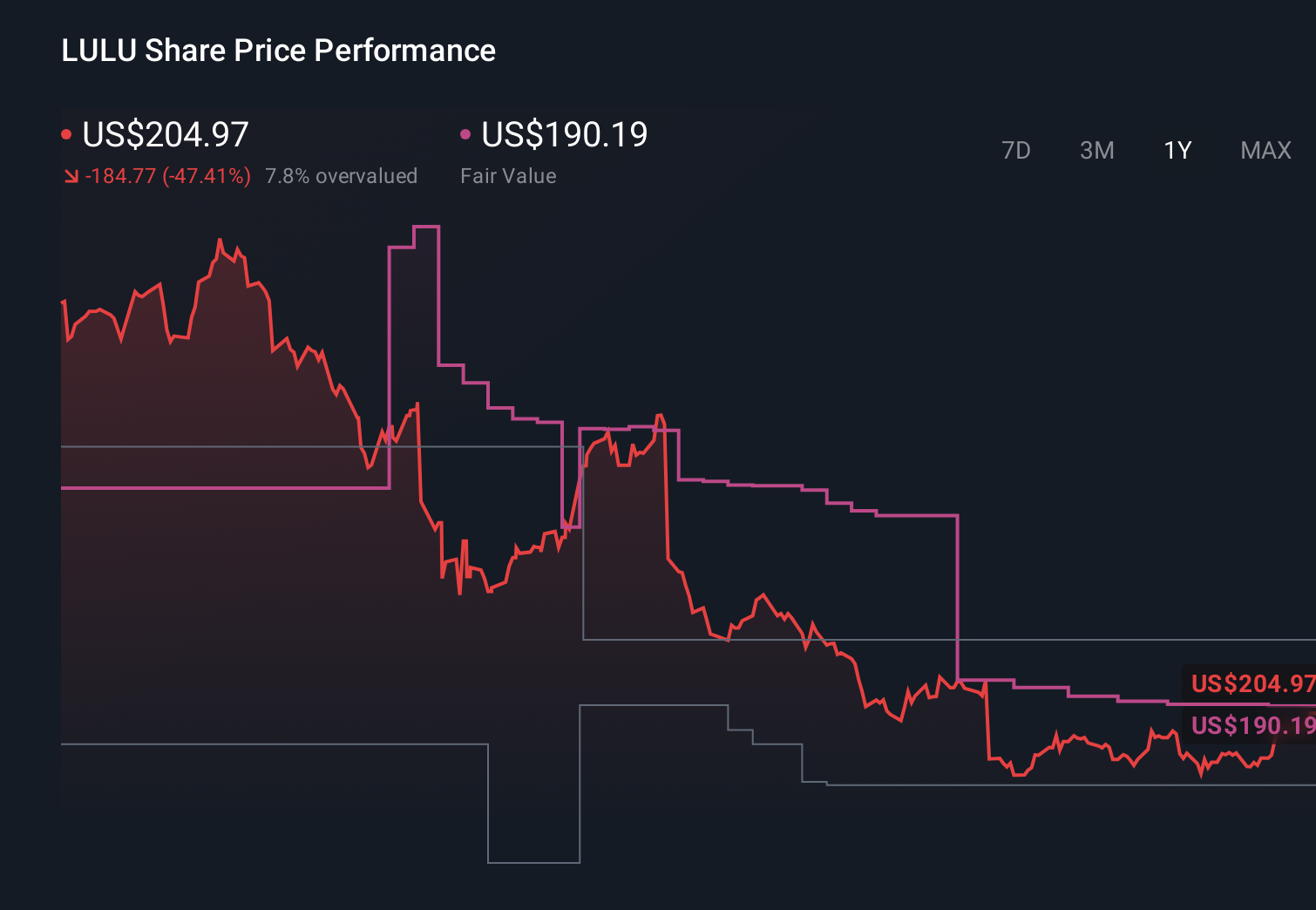

- In early June 2026, lululemon athletica reported first‑quarter sales of US$2,471.6 million with significantly lower net income and earnings per share than a year earlier, cut its full‑year outlook, and issued guidance for a 2%–3% revenue decline in the second quarter alongside ongoing U.S. demand and margin pressures.

- At the same time, the company moved to resolve tensions with founder Chip Wilson through a cooperation agreement that reshapes its board and governance, while management highlighted sharp regional divergence with weakness in North America and continued strength in China as it embarks on a broad product and brand reset.

- We’ll now examine how this guidance cut and U.S. weakness, set against China strength and leadership changes, affect lululemon’s investment narrative.

AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

lululemon athletica Investment Narrative Recap

To own lululemon today, you need to believe that its product reset, China growth and brand power can offset a weakening U.S. business, tariff headwinds and margin pressure. The latest quarter and guidance cut keep the core near term catalyst squarely on a U.S. sales and brand rebound, while the biggest current risk is that demand softness and higher costs linger longer than expected. This news reinforces, rather than changes, that risk balance.

The cooperation agreement with founder Chip Wilson, which adds three independent directors and starts declassifying the board, is particularly important here. It tightens governance just as lululemon works through U.S. underperformance, a brand reset and a CEO transition, creating a clearer link between execution on these catalysts and board accountability without directly changing the near term financial outlook.

Yet beneath the appeal of a premium global brand, investors should be aware that...

lululemon athletica's narrative projects $12.6 billion revenue and $1.6 billion earnings by 2029. This requires 4.3% yearly revenue growth with earnings remaining flat from $1.6 billion today.

Uncover how lululemon athletica's forecasts yield a $179.36 fair value, a 53% upside to its current price.

Exploring Other Perspectives

The most bullish analysts were assuming lululemon could reach about US$13.8 billion in revenue and US$2.2 billion in earnings by 2028, which now looks far more optimistic when set against U.S. weakness and product fatigue risk, reminding you that opinion ranges are wide and worth comparing before deciding what you believe.

Explore 43 other fair value estimates on lululemon athletica - why the stock might be worth 32% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your lululemon athletica research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free lululemon athletica research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate lululemon athletica's overall financial health at a glance.

Searching For A Fresh Perspective?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.