Lululemon’s Tariff Lawsuit Fight Could Be A Game Changer For lululemon athletica (LULU)

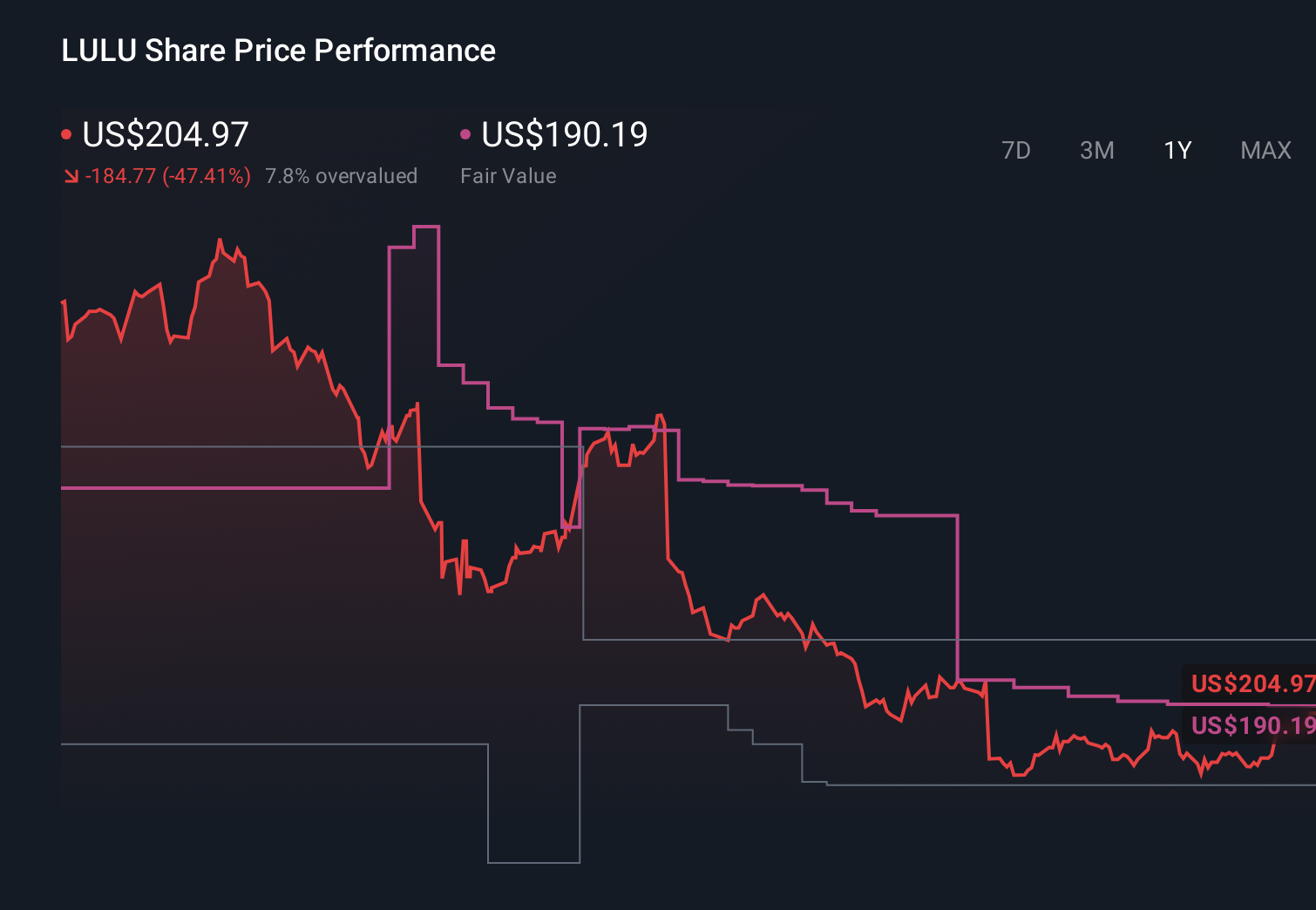

lululemon athletica inc. LULU | 0.00 |

- In late June 2026, Hagens Berman and The Miller Law Firm filed a consumer-protection lawsuit alleging Lululemon unlawfully kept tariff-linked price increases after the U.S. Supreme Court invalidated IEEPA tariffs, even as the company pursued refunds as importer of record.

- The case not only challenges Lululemon’s handling of hundreds of millions of dollars in contested tariff-related costs but also raises broader questions about how the brand balances legal rights, pricing decisions, and customer trust.

- We’ll now explore how resolving the proxy battle and reshaping the board could influence Lululemon’s longer-term investment narrative and risk profile.

Find 43 companies with promising cash flow potential yet trading below their fair value.

lululemon athletica Investment Narrative Recap

To own Lululemon today, you have to believe the brand can refresh its product engine and reignite demand, particularly in a softening U.S. business, while using international and digital channels to offset domestic pressure. The new class-action lawsuit around tariff-linked pricing directly underscores brand-trust risk, but its financial impact is uncertain, and the more immediate catalyst still appears to be whether the ongoing product reset can stabilize sales in the next few quarters.

The recent board reshuffle following the proxy battle, which added new directors backed by founder Chip Wilson, is especially relevant here because it could influence how Lululemon approaches both pricing decisions and customer redress in light of the lawsuit. It also matters for how aggressively the company backs its innovation, international expansion, and margin protection efforts that many investors are watching as key drivers of sentiment.

Yet even if the product reset works, investors should be aware that legal and tariff related disputes could still reshape how Lululemon manages pricing, refunds, and long term margins...

lululemon athletica's narrative projects $12.3 billion revenue and $1.6 billion earnings by 2029. This requires 3.2% yearly revenue growth and an earnings increase of about $0.1 billion from $1.5 billion today.

Uncover how lululemon athletica's forecasts yield a $132.16 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Some of the most pessimistic analysts were already assuming roughly flat revenue near US$10.9 billion and lower margins by 2029, so when you factor in fresh legal and tariff related uncertainty, you can see how opinions might spread even further apart and why it is worth comparing several viewpoints before you decide what feels realistic for you.

Explore 41 other fair value estimates on lululemon athletica - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your lululemon athletica research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free lululemon athletica research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate lululemon athletica's overall financial health at a glance.

Interested In Other Possibilities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.