Lyft (LYFT) Valuation Check As Israel Ride Hailing Bill Opens A Potential New Market

Lyft LYFT | 13.34 | +0.38% |

The recent approval by an Israeli ministerial committee of a bill that would allow ride hailing platforms into the country has put fresh attention on Lyft (LYFT) as a potential new entrant.

At a share price of $17.90, Lyft has had a softer recent run, with a 30 day share price return of 8.72% and a 90 day share price return of 12.55% decline, even though the 1 year total shareholder return of 29.71% points to stronger performance over a longer stretch. Alongside the potential Israel entry, investors have also been reacting to headlines around new unionization efforts in Illinois, pay floor proposals in Maine, options activity that skews bearish, and fresh competitive pressure from Tesla’s Robotaxi announcement.

If the Israel news has you looking at how ride hailing and mobility are evolving, it could be worth scanning auto manufacturers as another way to spot transport names exposed to shifting demand and technology trends.

With Lyft valued at US$17.90 per share, trading at a discount to some analyst targets and with an estimated intrinsic value gap still flagged, you have to ask: is this a mispriced rideshare player, or is the market already baking in future growth?

Most Popular Narrative: 25.6% Undervalued

Lyft’s most followed narrative pegs fair value at $24.07 versus the recent $17.90 close, which suggests the market and the narrative are telling different stories.

The ongoing rollout and consumer adoption of autonomous vehicles backed by new partnerships with tech leaders like Baidu and operational capabilities in both the U.S. and Europe are expected to significantly expand Lyft's total addressable market (TAM), lower labor costs, and increase long-term gross margins and earnings.

Want to see what this narrative is really baking in, across revenue, margins, and earnings? The entire fair value rests on a tight set of financial assumptions. The key tension is how quickly profitability scales versus growth investment. Curious which numbers have to line up for $24.07 to make sense?

Result: Fair Value of $24.07 (UNDERVALUED)

However, this depends on Lyft fending off intense competition from larger rivals and avoiding cost spikes if regulators push insurance or autonomous vehicle rules in a tougher direction.

Another View: Valuation Ratios Paint A Tougher Picture

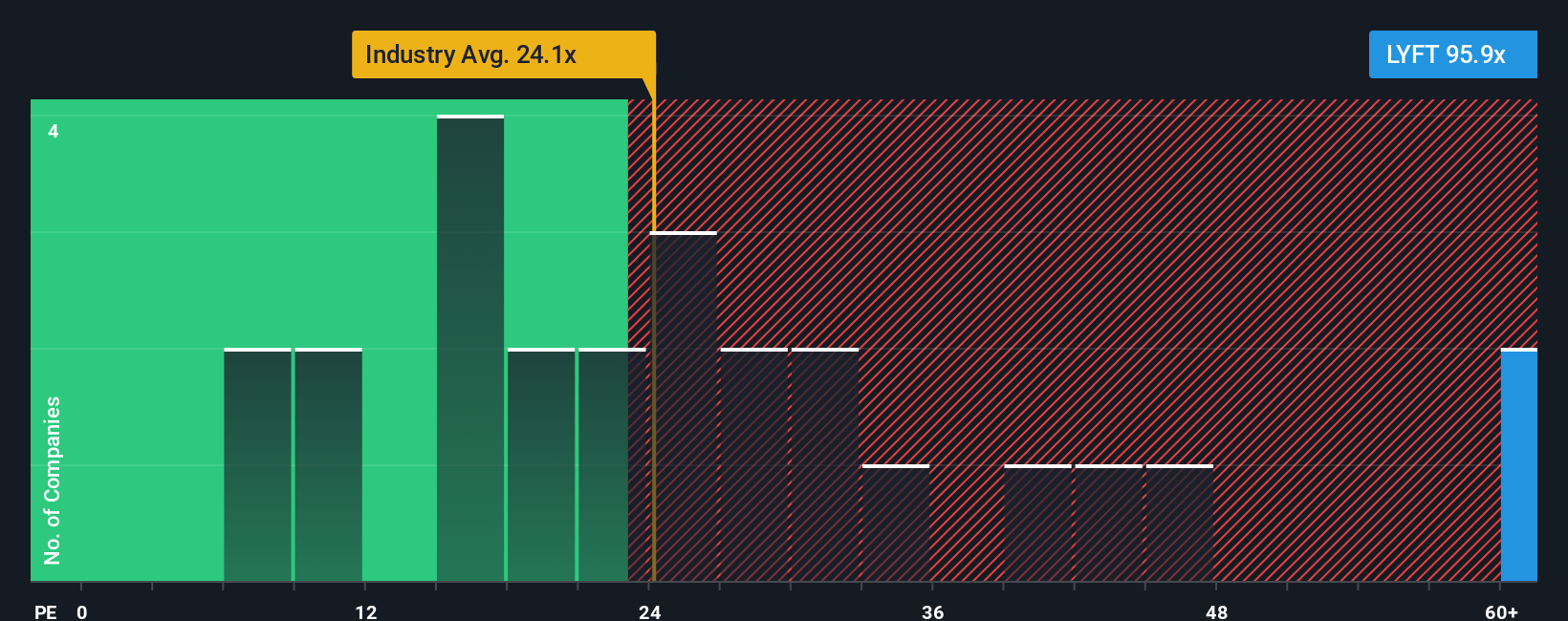

While our fair value model suggests Lyft is 63.5% below intrinsic value, the current P/E of 47.4x raises different questions. It sits above the US Transportation average of 32.7x and the fair ratio of 18.4x, even though it is below peers at 53x. That gap points to real valuation risk if sentiment cools. The key question is which signal you give more weight to.

Build Your Own Lyft Narrative

If you are not fully on board with this view or you prefer to stress test the numbers yourself, you can build a custom thesis in under three minutes, starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Lyft.

Looking for more investment ideas?

If Lyft has you thinking about where to put your next dollar to work, do not stop at a single ticker. Consider a broader range of options and compare what else fits your goals.

- Explore potential high risk high reward opportunities by scanning these 3523 penny stocks with strong financials that show stronger financial foundations than many smaller peers.

- Access the growth of artificial intelligence by filtering for these 24 AI penny stocks where market themes and business models align with your view on the future of tech.

- Focus on price versus fundamentals by examining these 864 undervalued stocks based on cash flows that might offer more appealing entry points than widely followed headline names.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.