Maase (MAAS) Stock Looks Rich After A Very Large Rally

Maase Inc MAAS | 0.00 |

Maase (MAAS) has drawn renewed attention after recent share price moves, prompting investors to reassess how the company’s AI centric digital systems business, focused on flexible energy and commercial networks, aligns with its current valuation.

Recent trading has been strong, with Maase’s share price return of 5.35% over one day, 25.08% over seven days and 59.49% over thirty days building on a very large 90 day share price return and 224.46% year to date share price return. This performance points to accelerating momentum as investors reassess the stock’s risk and growth profile against its current valuation.

If Maase’s recent surge has you thinking about other AI focused opportunities, this could be a good moment to check out 49 AI infrastructure stocks

With Maase now valued at about US$8.36b despite modest reported revenue and a recent net loss, the key question for you is clear: is there still upside on the table, or is the market already pricing in future growth?

Preferred Price to Book Multiple of 29.2x: Is it justified?

Based on the preferred metric of price to book, Maase currently trades on a P/B of 29.2x, which is high compared with both the US Insurance industry and its peer group.

The P/B ratio compares the company’s market value to its book value of equity. A higher multiple often reflects investor expectations for future returns on that equity or for valuable intangible assets not yet fully reflected on the balance sheet. For Maase, this elevated P/B sits alongside very limited reported revenue of about $3.48m and a recent net loss of $1.78m, so the current valuation is not anchored by profitability.

Against that backdrop, Maase’s 29.2x P/B stands far above the US Insurance industry average of 1.5x and also well above the 4.2x peer average. This indicates that the market is valuing each dollar of Maase’s equity at a multiple far greater than comparable companies. Without a fair ratio estimate to suggest a level the P/B could gravitate toward, the stock’s current pricing appears heavily influenced by expectations around its AI centric digital systems story rather than established financial performance.

Result: Price-to-book of 29.2x (OVERVALUED)

However, Maase’s modest US$3.48m revenue and recent net loss of US$1.78m mean any disappointment in its AI deployment or asset scaling could quickly pressure sentiment.

Another View: SWS DCF Model Signals a Very Different Picture

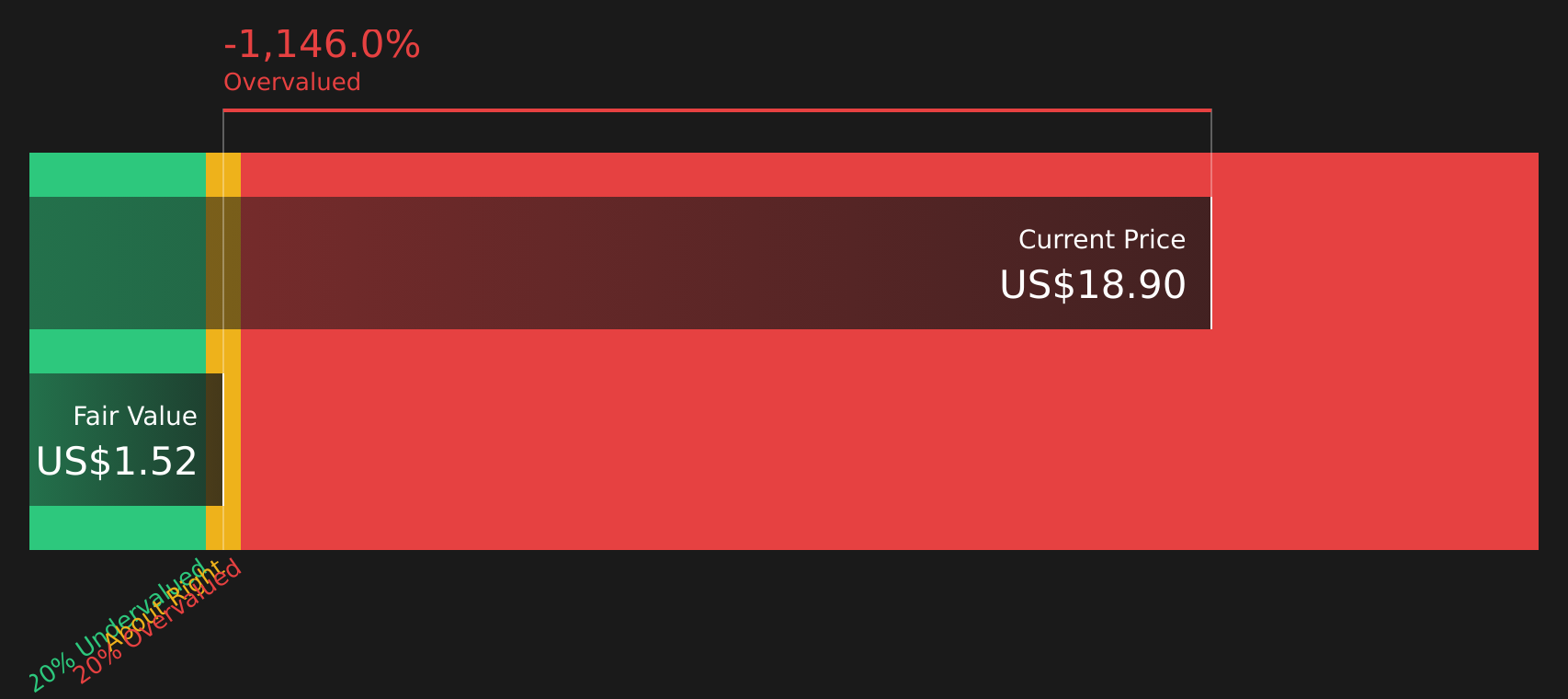

While the P/B ratio suggests Maase is priced richly against insurance peers, the SWS DCF model points in the same direction, with an estimated future cash flow value of $1.52 per share versus the current $18.90. That gap suggests expectations are already very high, so where is your comfort level?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Maase for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With Maase attracting strong opinion on both its risks and its potential rewards, this is a good moment to act quickly and test the data for yourself, starting with the 1 key reward and 3 important warning signs.

Looking for more investment ideas beyond Maase?

If Maase has sharpened your focus on where capital works hardest, do not stop here. Broaden your watchlist with ideas filtered for quality, resilience and income.

- Target potential mispricing by scanning for companies that combine quality fundamentals with attractive valuations through the 44 high quality undervalued stocks.

- Strengthen your defence by focusing on businesses with healthier finances using the solid balance sheet and fundamentals stocks screener (48 results).

- Build a cash flow stream by reviewing companies offering higher yields and resilient payouts in the 7 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.