Main Street Capital (MAIN) Stock May Be 28% Undervalued Despite Credit Facility Expansion

Main Street Capital Corporation MAIN | 0.00 |

Main Street Capital stock has delivered a 5 year return of 87.7%, yet its current checks show a mixed valuation picture, with the intrinsic value estimate pointing to meaningful upside while market multiples suggest the price is closer to fair.

- Over the past 5 years, Main Street Capital has returned 87.7%, which sets a high bar for any further upside case.

- Recent news around an expanded revolving credit facility and portfolio exits can support future income generation, while questions around the sustainability of supplemental dividends remain a key risk for how investors value the stock.

- On Simply Wall St's broader checks, Main Street Capital is assessed as undervalued in 4 of 6 areas, a mixed picture rather than a clear bargain or clear overvaluation. See the full breakdown at 4 out of 6.

The issue now is whether Main Street Capital's current price already reflects its income profile and recent developments, or if the intrinsic value estimate still leaves room for upside.

Is Main Street Capital a Bargain on Excess Returns?

The Excess Returns model looks at how efficiently Main Street Capital turns its equity base into profits above its cost of capital. For Main Street Capital, the model is built around a Book Value of $33.46 per share and a Stable EPS estimate of $5.18 per share, derived from the median return on equity over the past 5 years. With a Cost of Equity of $2.83 per share, the model suggests an Excess Return of $2.35 per share, supported by an average Return on Equity of 16.94% and a Stable Book Value assumption of $30.57 per share.

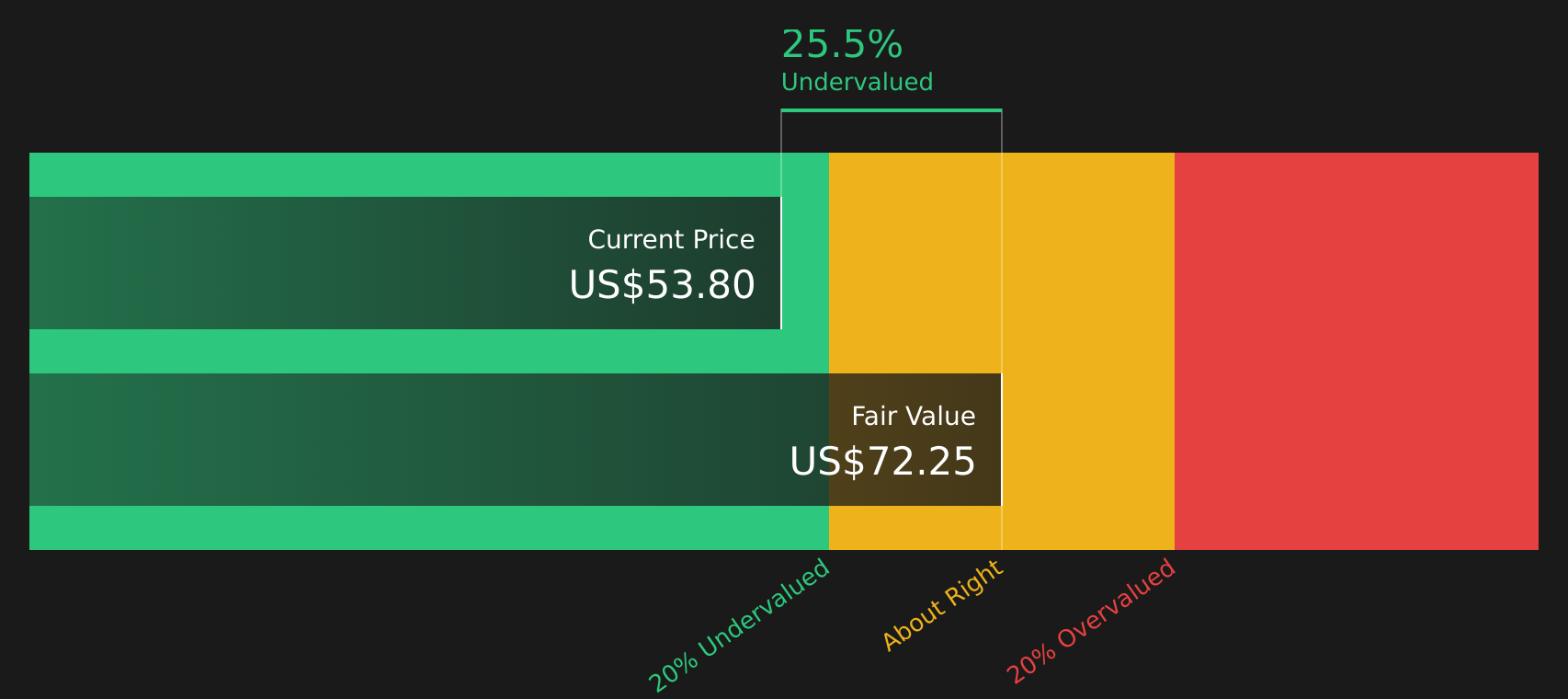

Translating these inputs into a per share estimate, the Excess Returns valuation points to an intrinsic value of $71.73. At this level, Main Street Capital would be trading at a 27.6% discount to the model’s estimate of intrinsic value. The recent increase in the revolving credit facility to $1.24b, together with the extended maturity profile, helps explain why the model still supports an excess return stream even as investors evaluate how dependable supplemental dividends will be.

On this Excess Returns view, the stock currently appears undervalued relative to the earnings power implied by its equity base.

Our Excess Returns analysis suggests Main Street Capital is undervalued by 27.6%. Track this in your watchlist or portfolio, or discover 43 more high quality undervalued stocks.

Where Does Main Street Capital Sit on Earnings?

P/E is a useful lens for Main Street Capital because earnings and dividends are central to how you judge this stock. Right now, Main Street Capital trades on a P/E of about 11.3x, which is below both the Capital Markets industry average of roughly 40.0x and the peer group average of around 17.3x.

The Fair Ratio for the stock, which estimates the P/E you might expect given its profile, sits at about 11.2x, almost identical to where Main Street Capital is currently priced. That tight fit suggests the market is broadly aligned with this tailored benchmark, even if the industry as a whole trades on much higher earnings multiples.

On the P/E measure, Main Street Capital stock currently looks priced at about fair value rather than clearly cheap or expensive.

The Main Street Capital Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Main Street Capital pick up where the valuation checks leave off by spelling out which paths for Main Street Capital's future earnings, margins and growth would need to play out for the stock to be worth meaningfully more or less than it is today on the market. Instead of a single output from a ratio or model, Narratives lay out the future those numbers rely on, so you can see what needs to materialise and monitor whether it is on track over time on the Community page.

If you have a numbers based view on whether Main Street Capital's larger US$1.24b revolving credit facility and recent portfolio exits support the current valuation, share a Narrative to put your thesis on record. Add your voice to the Simply Wall St community and track how your case on Main Street Capital holds up as new results and developments come through.

Do you think there's more to the story for Main Street Capital? Head over to our Community to see what others are saying!

The Bottom Line

For Main Street Capital, the intrinsic value estimate from the Excess Returns model points to meaningful upside, while the P/E view suggests the stock is priced about right against its tailored benchmark. That split comes down to whether the company can keep converting its equity base into earnings at recent levels, despite questions around the longevity of supplemental dividends. With a mixed broader valuation picture, the real debate now is whether the current discount to intrinsic value reflects an opportunity in a resilient income stream or a fair adjustment for the risk that those extra distributions prove less dependable over time.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.