Manchester United (MANU) Rebuilds Its Midfield, Is The Stock Still Expensive?

Manchester United Plc Class A MANU | 0.00 |

Midfield overhaul puts Manchester United (MANU) in the spotlight

Manchester United (MANU) is drawing fresh investor attention as the club moves to overhaul its midfield following Casemiro’s exit and injury issues, and is pursuing high-value deals for Andrey Santos, Ederson and Manu Kone.

Manchester United’s latest transfer moves come after a strong share price run, with a 90 day share price return of 24.94% and a year to date share price return of 39.67%. The 1 year total shareholder return is 25.37% and the 5 year total shareholder return is 47.87%, suggesting recent momentum has been strong compared with parts of its longer history.

If this kind of rebuilding story has your attention, it can be helpful to see what else is on the move and broaden your search with 18 top founder-led companies

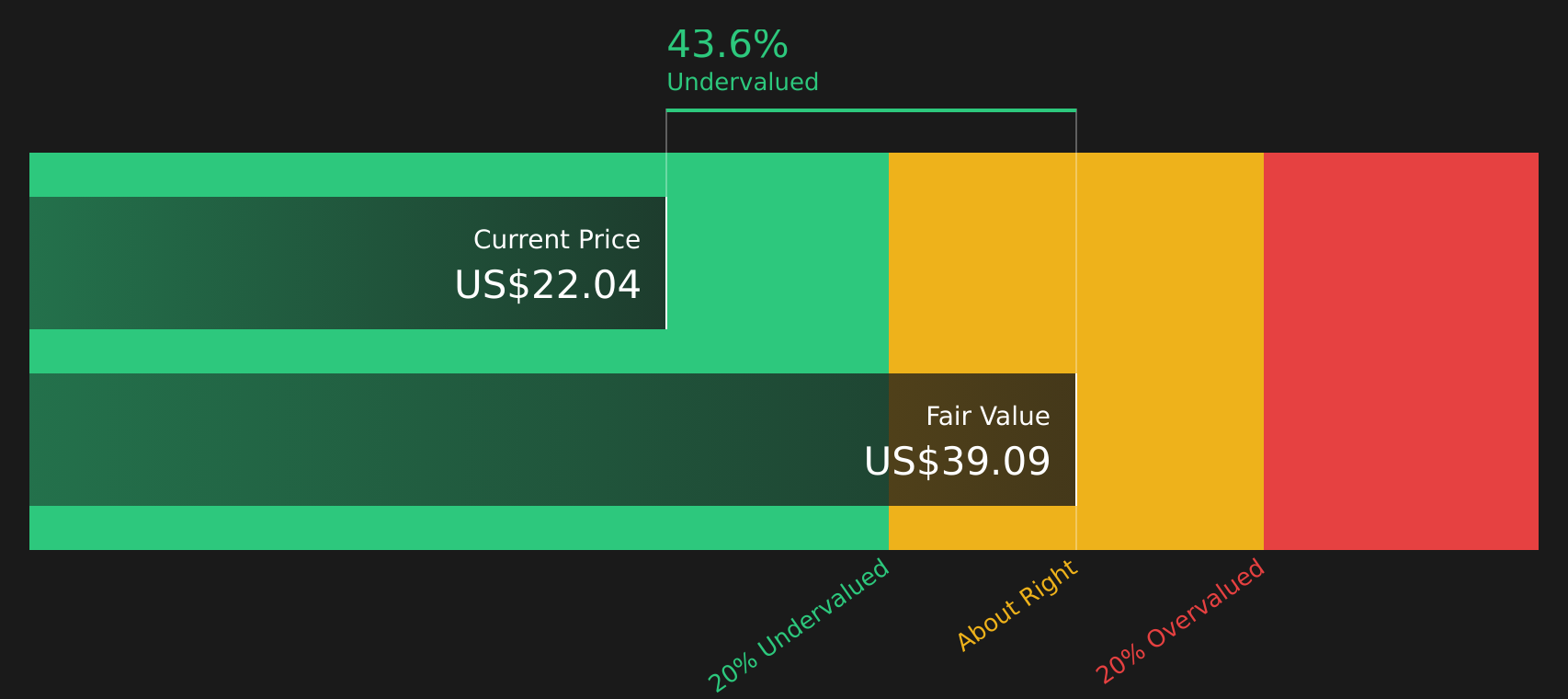

After Manchester United’s sharp share price move, the stock now trades about 17% below the average analyst target and at a wider discount to one intrinsic value estimate. So where does fair value really sit for you?

Preferred Price-to-Sales multiple of 4.1x for Manchester United: Is it justified?

On a P/S basis, Manchester United trades at 4.1x, which sits alongside a recent price of $22.04 and a sizeable discount to one intrinsic value estimate.

The P/S ratio compares the company’s market value with its annual revenue, so at 4.1x you are paying just over four times Manchester United’s reported revenue of $684.3 million. For a global sports and media brand that relies heavily on broadcast, sponsorship and merchandising income, investors often focus on revenue based metrics when earnings are still loss making.

Here, the picture is mixed. On one side, Manchester United is currently unprofitable, reports a loss of $18.1 million and has a negative return on equity. In addition, earnings are forecast to grow very quickly and the company is expected to move into profit over the next three years. On the other side, revenue is forecast to grow at around 8% a year, which is slower than both the broader US market and high growth thresholds. As a result, the current P/S looks like it builds in a relatively rich view of future revenue quality and monetisation.

Compared with peers, that premium stands out sharply. The US Entertainment industry average P/S is 1.2x and the peer group average is 2.1x, while a fair P/S ratio estimate for Manchester United sits closer to 2.2x. That is a wide gap and suggests the current 4.1x could be well above a level the market might eventually settle around if expectations cool.

Result: Price-to-Sales of 4.1x (OVERVALUED)

However, Manchester United still faces risks, including ongoing losses of $18.1 million and a relatively high P/S premium compared with the wider US Entertainment industry.

Another view of Manchester United’s value

While the 4.1x P/S ratio makes Manchester United look expensive against the US Entertainment industry at 1.2x and peers at 2.1x, the SWS DCF model shows an estimated future cash flow value of $39 per share versus the current $22.04 price. This suggests potential undervaluation and raises the question of which signal should be treated as more important.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Manchester United for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of optimism and concern around Manchester United has you thinking, take a moment to review the numbers yourself, weigh the risks and rewards, and then check the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Manchester United?

If Manchester United has sharpened your focus on opportunities, do not stop here. Broaden your watchlist with a few targeted ideas that other investors often overlook.

- Spot potential mispricings early and review 44 high quality undervalued stocks that pair quality fundamentals with more modest expectations.

- Prioritise resilience and stability by scanning 76 resilient stocks with low risk scores that score well on risk factors and balance sheet strength.

- Get ahead of the crowd and assess a screener containing 19 high quality undiscovered gems before they attract wider attention and tighter pricing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.