MannKind (MNKD) Valuation Check As Afrezza Pediatric Milestones Open Needle Free Insulin Opportunity

MannKind Corporation MNKD | 2.50 | -1.57% |

MannKind (MNKD) is back in focus after enrolling the first pediatric patient in its INHALE-1ST Afrezza study and advancing an FDA review that could make Afrezza the first needle-free insulin option for children.

The latest Afrezza pediatric milestones come as MannKind’s 30 day share price return of 8.64% and 90 day share price return of 13.20% point to building momentum, while its 1 year total shareholder return of 4.43% and 5 year total shareholder return of 7.20% reflect a more measured longer term outcome.

If you are watching MannKind’s progress and want to widen your search in healthcare, this is a good moment to check out 25 healthcare AI stocks as another potential source of ideas.

With MannKind trading at US$5.66 and screening tools flagging a sizeable gap to some intrinsic and analyst value estimates, you have to ask: is this a mispriced growth story, or is the market already accounting for those potential future gains?

Most Popular Narrative: 41.1% Undervalued

With MannKind last closing at $5.66 against a narrative fair value of $9.61, the current price sits well below what this widely followed view calls reasonable, putting extra attention on the assumptions behind that gap.

Afrezza's continued double digit prescription growth, international expansion efforts, upcoming pediatric indication launch, and a broadened salesforce footprint are set to accelerate market penetration amid a rising global diabetes burden and an aging population, directly supporting revenue and earnings growth.

Curious what kind of revenue curve and margin profile would justify that higher value, and what sort of future earnings multiple sits underneath it? The narrative leans heavily on faster earnings growth than the broader market, a richer profit margin profile than today, and a valuation multiple that assumes investors keep paying up for that growth. If you want to see how those moving parts fit together, the full story lays out the numbers behind that $9.61 figure.

Result: Fair Value of $9.61 (UNDERVALUED)

However, there are still meaningful risks here, including Afrezza adoption remaining niche and heavy dependence on a small set of products and royalty streams.

Another Angle On The Valuation

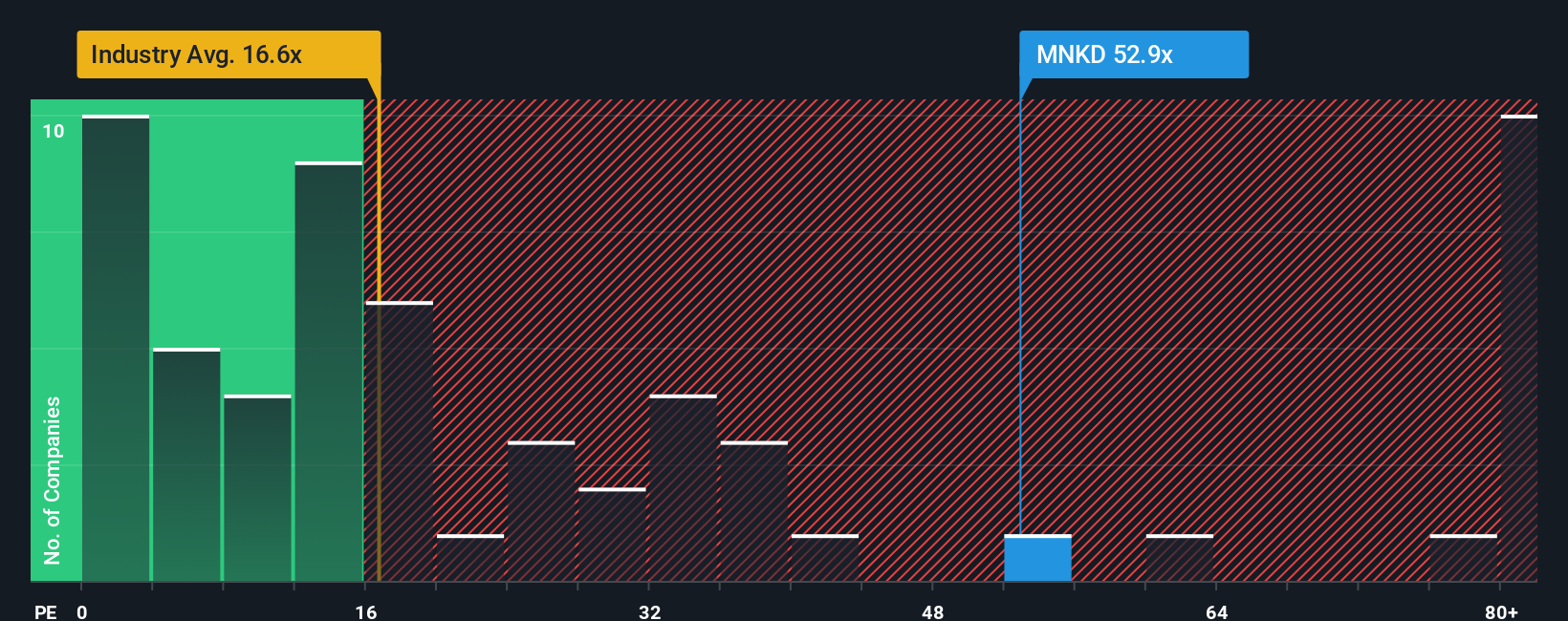

That US$9.61 fair value suggests MannKind looks undervalued, but the earnings multiple tells a different story. The current P/E of 59.5x sits well above the 22.2x industry average and the 25.1x fair ratio, which points to richer pricing and higher execution risk. Which signal do you trust more?

Next Steps

Wondering how to balance the enthusiasm in this story with the risks on the table? Take a closer look at the details, move quickly if you need to, and weigh up 4 key rewards and 3 important warning signs to shape your own view.

Looking for more investment ideas?

If MannKind has caught your attention, do not stop here. A broader set of ideas from different corners of the market could help you evaluate your next move.

- Target potential mispricings by scanning companies our screener flags as 55 high quality undervalued stocks based on fundamentals and valuation signals.

- Focus on stability first by reviewing 81 resilient stocks with low risk scores that score well on volatility and risk factors.

- Hunt for early stage opportunities by checking out our 29 elite penny stocks with strong financials that still meet quality and financial health checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.