Maplebear (CART) Is Up 11.7% After Strong Earnings and Expanded Grocery Partnerships Has the Bull Case Changed?

Maplebear Inc. CART | 38.64 38.64 | +3.15% 0.00% Post |

- In November 2025, Instacart (Maplebear Inc.) reported higher quarterly sales and net income compared to the prior year and announced new enterprise partnerships, including an expanded collaboration with Associated Food Stores to deploy white-label e-commerce solutions across multiple grocery banners.

- These developments, coupled with ongoing share repurchases and the rollout of advanced AI-powered retail technologies, reflect Instacart’s growing momentum in strengthening its omnichannel presence and operational efficiency.

- We'll explore how Instacart's strong quarterly earnings and expanded retail partnerships could shape its future investment outlook.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Maplebear Investment Narrative Recap

To be a Maplebear (Instacart) shareholder, you need to believe that grocery e-commerce adoption will keep expanding and that the company's investments in AI and omnichannel partnerships will build a more profitable, resilient business. While the new enterprise deals and strong earnings support Instacart’s technology-driven margin story, they do not materially change the most important near-term catalyst: further traction in high-margin advertising and retail media. The biggest current risk for investors remains potential changes in labor costs and regulations, which could challenge net margins if gig work economics come under pressure.

Among the recent developments, Instacart’s expanded partnership with Associated Food Stores stands out as particularly relevant. By bringing Instacart’s white-label e-commerce, retail media, and in-store AI technology to over 40 banners, Instacart is deepening its integration with established retailers, creating more recurring non-transaction revenue opportunities, an ongoing catalyst for profitability and stability. These enterprise wins reinforce the trend toward stickier, tech-enabled partnerships that could help offset volatile demand from end consumers.

On the other hand, investors should also be mindful of how quickly changes in labor regulations or costs could disrupt…

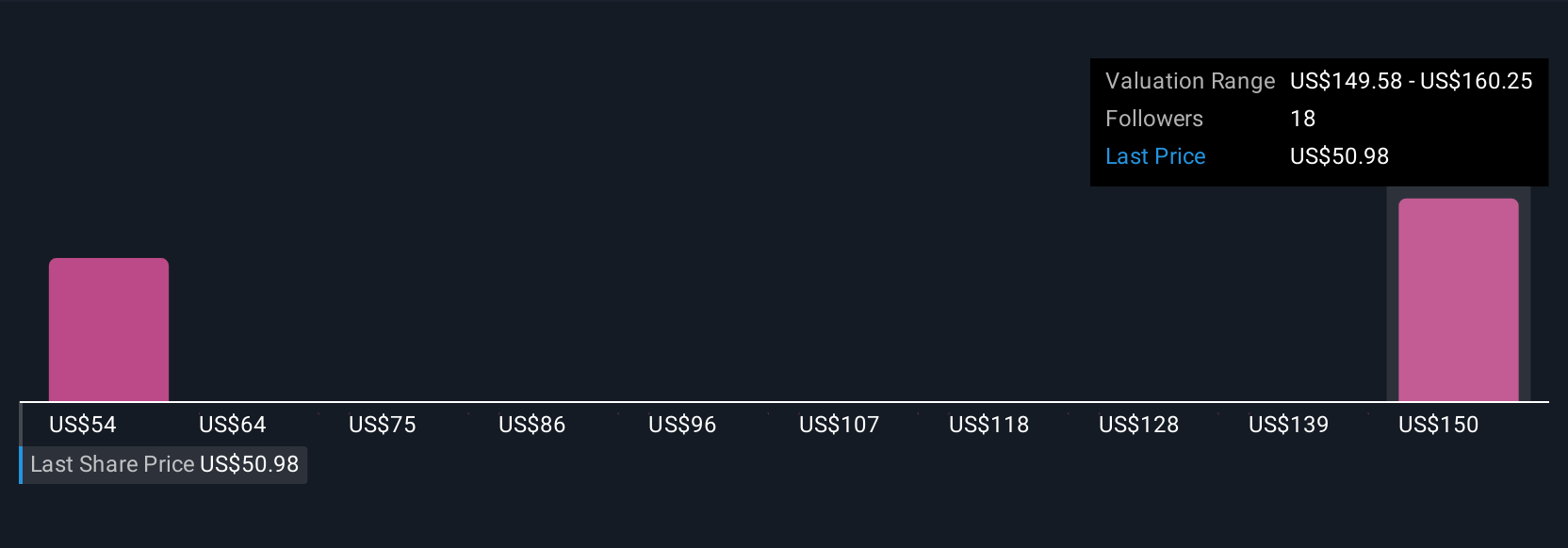

Maplebear's narrative projects $4.6 billion in revenue and $779.9 million in earnings by 2028. This requires 9.3% yearly revenue growth and a $300.9 million earnings increase from the current $479.0 million level.

Uncover how Maplebear's forecasts yield a $50.67 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Three fair value estimates from the Simply Wall St Community ranged widely from US$46.47 to US$94.83. While opinions vary, the company’s push for retailer-integrated tech and new recurring revenues may help support future earnings, though cost structure risks are top of mind for many.

Explore 3 other fair value estimates on Maplebear - why the stock might be worth just $46.47!

Build Your Own Maplebear Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Maplebear research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Maplebear research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Maplebear's overall financial health at a glance.

No Opportunity In Maplebear?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 37 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.