Marathon Petroleum (MPC) Stock After 62% One-Year Surge Is There More Upside?

Marathon Petroleum Corporation MPC | 0.00 |

- If you are wondering whether Marathon Petroleum stock still offers value after a strong run, the next sections break down what the current price may be implying.

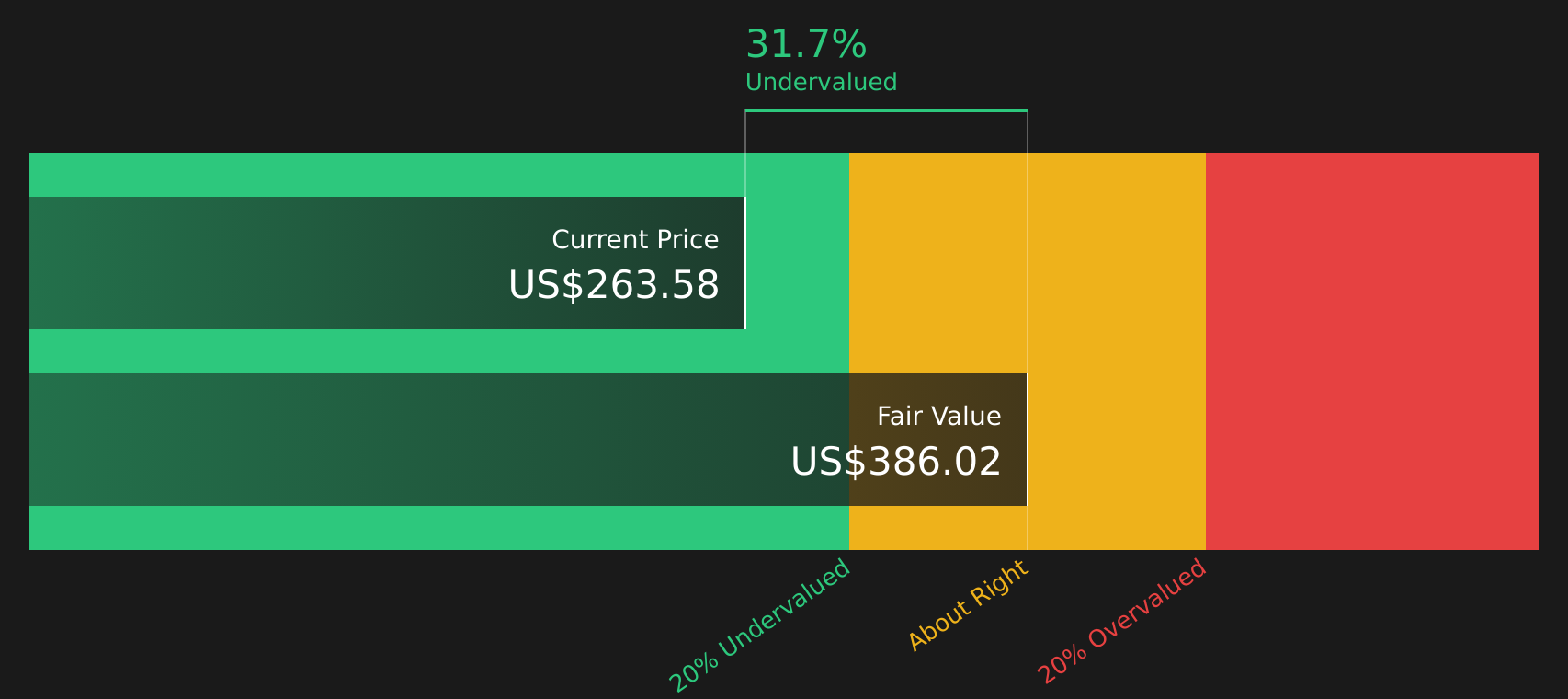

- At a last close of US$263.58, the stock has returned 0.6% over the past week, 3.4% over the past month, 59.6% year to date, and 61.7% over the past year. These figures can influence how investors think about both upside potential and risk.

- Recent coverage of Marathon Petroleum has focused on its position within the US energy sector and how investor sentiment has reacted to broader moves in oil and gas markets. This context helps frame whether the current share price reflects company specific factors, sector trends, or a mix of both.

- Marathon Petroleum currently has a valuation score of 3 out of 6. The following sections outline how different valuation approaches interpret that score, along with a final section on a broader way to think about value beyond a single metric.

Approach 1: Marathon Petroleum Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a stock could be worth by projecting future cash flows and then discounting them back to today using a required rate of return. It is essentially asking what the future stream of cash is worth in today's dollars.

For Marathon Petroleum, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month Free Cash Flow is about $6.7b. Analyst inputs and subsequent extrapolations by Simply Wall St project Free Cash Flow out to 2035, including estimates such as $11.1b in 2026 and $5.9b in 2030, all in $. These projected cash flows are then discounted to reflect the time value of money and risk.

On this basis, the DCF output suggests an estimated intrinsic value of about $386.02 per share. Compared with the recent share price of $263.58, the model indicates the stock trades at a discount of around 31.7%. Under these assumptions, Marathon Petroleum stock appears undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Marathon Petroleum is undervalued by 31.7%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Approach 2: Marathon Petroleum Price vs Earnings

The P/E ratio is a common way to value profitable companies because it directly links what you pay for the stock to the earnings the business generates today. In general, higher expected growth and lower perceived risk can justify a higher P/E ratio, while slower growth and higher risk usually align with a lower, more cautious multiple.

Marathon Petroleum currently trades on a P/E of 16.63x. This sits above the Oil and Gas industry average of 13.80x and also above the peer group average of 15.72x, which might initially look expensive compared to a simple sector or peer check. However, these benchmarks do not adjust for the company’s own earnings profile or risk characteristics.

Simply Wall St’s Fair Ratio for Marathon Petroleum is 20.23x. This proprietary metric is designed to estimate what a reasonable P/E might be after considering factors such as earnings growth, industry, profit margins, market cap and key risks. Because it is tailored to the company, it can offer a more targeted reference point than broad industry or peer averages. Comparing the Fair Ratio of 20.23x with the current P/E of 16.63x suggests the stock trades below this modelled level and therefore screens as undervalued on this metric.

Result: UNDERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your Marathon Petroleum Narrative

Earlier it was mentioned that there is an even better way to understand valuation. Narratives bring this to life by letting you attach a clear story about Marathon Petroleum to the numbers, including your view on future revenue, earnings, margins and what you see as a fair value.

A Narrative connects three things in one place: the company story you believe, the financial forecast that flows from that story, and the fair value you think lines up with those assumptions.

On Simply Wall St, Narratives sit on the Community page and are used by millions of investors as an easy tool to compare their own fair value with the current share price and decide whether the stock looks more attractive, less attractive or somewhere in between.

Because Narratives are refreshed when new information such as news or earnings is added, your view can stay current rather than frozen at the time you first ran the numbers.

For example, one Marathon Petroleum Narrative on the bullish end uses a fair value of about US$318.81, while a more cautious Narrative uses about US$163.00, which shows how two investors can look at the same stock, plug in different assumptions and reach very different conclusions about what the shares are worth today.

For Marathon Petroleum, here are previews of two leading Marathon Petroleum Narratives that may help frame your own view:

Fair value used in this bullish narrative: US$265.06

Implied pricing vs that fair value: about 0.6% below the narrative fair value at the last close.

Revenue trend assumption: revenue is assumed to decline 23.4% over the long term.

- Assumes refinery utilization and margins stay supportive, helped by product demand, capacity reductions and efficiency projects.

- Builds in higher profit margins by 2029 and ongoing share buybacks, which together lift earnings per share even as revenue is expected to be flat in the near term and weaker in the long term model inputs.

- Treats renewables and digital refinery upgrades as useful additions to cash flow and resilience, while still recognizing exposure to environmental policy risk and long term demand shifts.

Fair value used in this bearish narrative: US$163.00

Implied pricing vs that fair value: about 61.7% above the narrative fair value at the last close.

Revenue trend assumption: revenue is assumed to decline 2.2% a year over the next 3 years.

- Focuses on the risk that new refining and midstream projects do not run as hard as planned if product tightness eases or export demand softens, which could leave returns below management targets.

- Bakes in lower profit margins and earnings by 2029, even after share count reductions, and uses a P/E multiple that still assumes investors pay a premium for the stock.

- Flags that if sour crude differentials compress or LNG and NGL demand underwhelm, earnings and cash distributions could fall short of what is needed to support current buyback and dividend ambitions.

Taken together, these Narratives show how different assumptions on refining economics, demand for fuels and capital returns can lead to very different views of what Marathon Petroleum stock is worth today. If the numbers behind one view feel closer to how you see the world, that narrative can be a useful anchor for your own valuation work.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Marathon Petroleum on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Marathon Petroleum? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.