Mastercard (MA) Stock Looks Rich On Earnings But Reasonable On Broader Checks

Mastercard MA | 0.00 |

Mastercard stock is up about 40.6% over the past 5 years, but with the shares recently closing at US$513.60 and screening as overvalued on earnings multiples, investors are weighing that track record against a mixed read from the valuation checks.

- Over 5 years, Mastercard has returned roughly 40.6%, which is a solid outcome but not necessarily a clear signal that the current price still offers an attractive entry point.

- On the upside, Mastercard’s push into areas such as AI powered payments, stablecoins and cross border services can support expectations for continued growth. However, regulatory pressure, fee litigation and competition in digital payments may limit how much investors are willing to pay for that story.

- With a value score of 3 out of 6, Mastercard screens as a mixed picture rather than a straightforward bargain or an obviously expensive stock.

The stock’s next move may depend on whether Mastercard’s current price already reflects these growth initiatives and risks, or if there is still room for a better risk reward trade off.

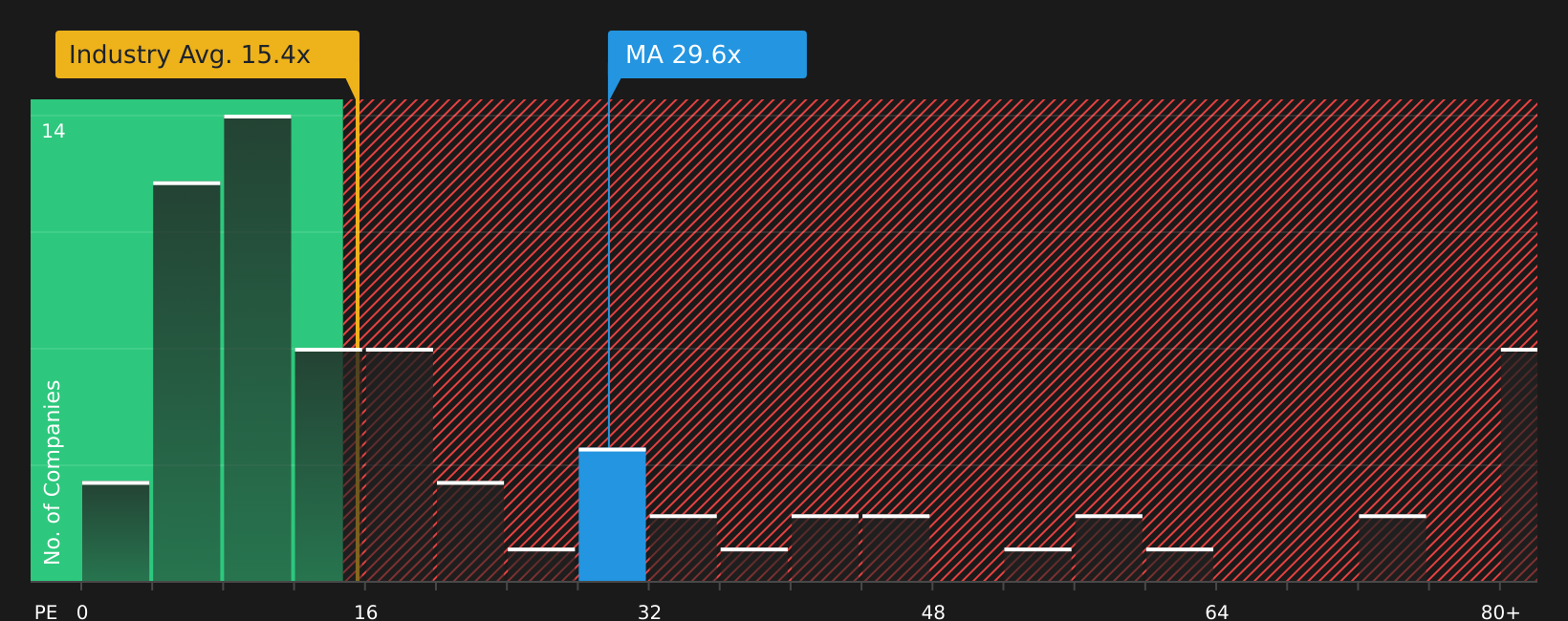

Has Mastercard Run Too Far on Earnings?

The P/E ratio is a useful lens for Mastercard because earnings are a key focus for investors in established, cash generative payment networks. At around 29.1x earnings, Mastercard trades at a premium to both its Diversified Financial industry average P/E of 15.3x and a peer group average of 25.4x, signaling that the market is willing to pay more for each dollar of Mastercard’s profit than for many peers.

The fair P/E ratio implied by the company’s profile is 20.8x, which is meaningfully lower than the current 29.1x, so Mastercard screens as overvalued on this metric. Despite recent headlines around AI powered services, stablecoins and cross border payments lifting interest in the stock, the current P/E already sits well above the level suggested by this more tailored benchmark.

On the P/E multiple alone, Mastercard stock currently looks overvalued relative to both peers and its own fair ratio estimate.

The Mastercard Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Mastercard pick up where the P/E discussion leaves off by setting out in plain terms what would need to happen to Mastercard’s revenue growth, margins and earnings for the stock to be worth materially more or less than it is today. Each narrative ties a fair value estimate to a particular view of Mastercard’s potential catalysts and key risks, so you can track over time which version of the story is closest to reality on the Community page.

One of the top community narratives on Mastercard: 32% undervalued

"It never lends money and never holds credit risk on its books, it just takes a small cut every time a transaction crosses its network..."

Do you think there's more to the story for Mastercard? Head over to our Community to see what others are saying!

The Bottom Line

For Mastercard, the valuation work points to a stock that already assumes a lot is going right, with the current P/E sitting above both peers and a tailored fair ratio. The checks do not flag an obvious bargain, but they also do not suggest wild excess, which leaves the debate centered on how much of Mastercard’s payment growth story is already in the price. The key swing factor from here is whether earnings can keep pacing the premium multiple, or whether sentiment cools and the market becomes less willing to pay up for its future.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.