McCormick (MKC): Assessing Valuation After a Year of Share Price Declines

McCormick & Company, Incorporated MKC | 50.44 | -6.11% |

McCormick (MKC) shares have been under quiet pressure recently, losing around 16% over the past year. The stock has lagged behind broader market gains. Despite steady revenue and net income growth, investors seem cautious about the company’s near-term trajectory.

Over the past year, McCormick’s share price has steadily lost ground with momentum fading in recent weeks, as a 7-day share price return of -6.9% and a year-to-date drop just under 16% hint at persistent caution from investors. In short, the stock’s total shareholder return has been negative over most short- and long-term periods. This reflects ongoing uncertainty about when sentiment and valuations might turn a corner for the company.

If you’re looking beyond the familiar names in food and beverage, now’s an ideal moment to broaden your search and discover fast growing stocks with high insider ownership

This recent slide raises a pivotal question for investors: Is McCormick now a hidden value, or has the market already baked in expectations for future growth and left little room for upside?

Most Popular Narrative: 17.5% Undervalued

At $63.83, McCormick’s shares are trading at a significant gap below the crowd-consensus fair value of $77.38. This suggests growing separation between current sentiment and analyst projections, with forward-looking expectations shaping the long-term case.

Ongoing global expansion and success in winning new customers in high-growth, health-oriented categories, particularly in Asia-Pacific and through partnerships with innovative beverage and snack brands, are broadening McCormick's addressable market while diversifying revenue streams. These factors are contributing to both top-line growth and future earnings stability.

How does McCormick get this coveted market premium? The secret is in bold profit growth assumptions and a pricing power that few food stocks can claim. Curious which financial leaps set this narrative apart? Click to discover the exact growth, margin, and valuation math driving its fair value projection.

Result: Fair Value of $77.38 (UNDERVALUED)

However, persistent pressure on input costs and unpredictable consumer demand could quickly undermine the profit and growth assumptions behind today’s bullish outlook.

Another View: Market Ratios Point to Expensive Territory

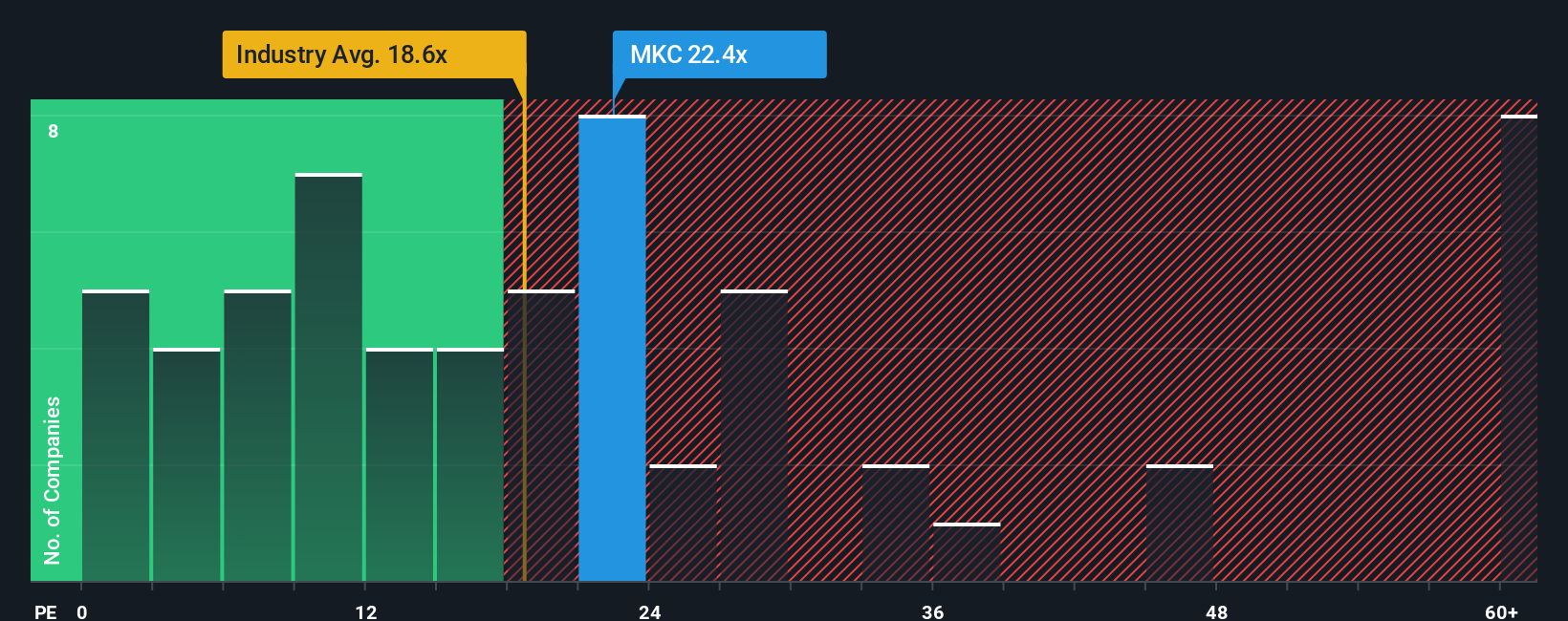

While fair value estimates suggest McCormick is undervalued, its current price is actually well above what both industry averages and the fair ratio imply. The company trades at 22 times earnings versus a fair ratio of 18.6, signaling the market may be pricing in extra optimism, which increases downside risk if growth falls short. Is the premium really worth it, or is the risk of a correction rising?

Build Your Own McCormick Narrative

If you see the story differently or want to test your own assumptions, it’s easy to dive into the data and shape your own perspective in minutes. Do it your way

A great starting point for your McCormick research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Don’t settle for the usual picks. Uncover new opportunities and get ahead of the crowd with fresh angles you won’t want to miss:

- Tap into potential growth by checking out these 854 undervalued stocks based on cash flows, giving you a head start on stocks with attractive valuations and unexplored upside.

- Capitalize on the digital future by navigating these 81 cryptocurrency and blockchain stocks, highlighting businesses redefining secure payments and blockchain-powered innovation.

- Generate reliable returns by examining these 21 dividend stocks with yields > 3%, featuring companies providing strong yields and proven financial health for income-focused investors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.