McCormick (MKC) Valuation Check As Shares Struggle To Recover From Multi Year Weakness

McCormick & Company, Incorporated MKC | 48.85 | +0.97% |

Recent share performance and business profile

McCormick (MKC) has been under pressure, with the stock showing a 1 day return of 1.9%, a 7 day decline of 2.9%, roughly 3.4% lower over the past month, and 1.2% lower over the past 3 months.

Over longer periods, total returns are also weaker, with a 6.7% decline over the past year, 8.5% over 3 years, and 21.5% over 5 years. That backdrop is shaping how investors look at the business today.

The company generates US$6.79b in revenue and US$778.0m in net income from its two segments, Consumer and Flavor Solutions, focused on spices, seasonings, condiments, sauces, and other flavor products sold globally.

- The Consumer segment sells branded herbs, spices, sauces, and desserts through grocery, mass merchandise, warehouse clubs, discount and drug stores, and e commerce channels.

- The Flavor Solutions segment supplies seasoning blends, condiments, coating systems, and compound flavors directly and through distributors to multinational food manufacturers and foodservice customers.

With the share price at US$66.56 and a 1 year total shareholder return of a 6.7% decline after earlier weakness in recent months, momentum looks to be fading rather than turning higher at this stage. This can reflect a more cautious view on the company’s growth prospects or risk profile.

If you are comparing McCormick with other food names, it can also be useful to scan wider across established healthcare stocks to see how different defensively positioned sectors are currently being priced.

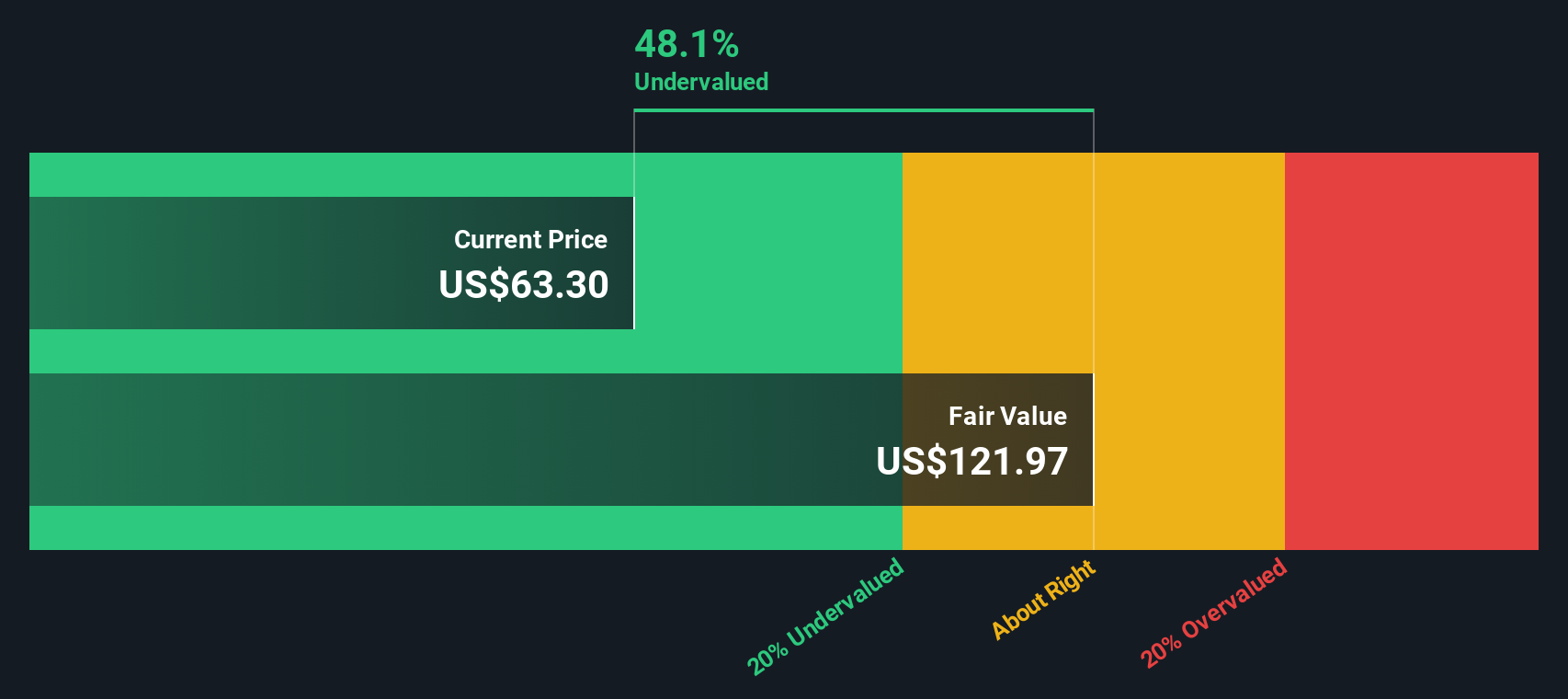

With McCormick trading at US$66.56, weaker multi year returns and some implied discount measures are catching attention. Is the stock quietly undervalued today, or is the market already pricing in future growth?

Price-to-Earnings of 23x: Is it justified?

McCormick currently trades on a P/E of 23x, which sits above both its food industry average and its closest peer group on this metric.

The P/E ratio compares the share price with earnings per share, so a higher multiple usually means investors are willing to pay more for each dollar of earnings. For a mature branded food company, that can reflect expectations around earnings stability, growth prospects, or balance sheet strength.

Here, McCormick’s 23x P/E is higher than the US Food industry average of 21.4x and above the peer average of 22.6x. This suggests the market is putting a premium on the company relative to similar names. Against an estimated fair P/E of 17.6x, that premium looks even stronger and points to a level the market could move towards if sentiment or expectations cool from here.

At the same time, Simply Wall St’s DCF framework flags McCormick as trading at a 36.5% discount to its estimated fair value, with an implied future cash flow value of US$104.84 versus the current US$66.56 share price. That contrast between an apparently expensive earnings multiple and a discounted cash flow valuation highlights how differently cash flow based models and market multiples can frame the same stock.

Result: Price-to-Earnings of 23x (OVERVALUED)

However, weaker multi year returns and a P/E premium leave little room if revenue growth slows or if rising costs pressure the US$778.0m net income base.

Another view on value: cash flows tell a different story

While the 23x P/E suggests McCormick is expensive next to the US Food industry at 21.4x, peers at 22.6x, and a fair ratio of 17.6x, our DCF model paints the opposite picture. It indicates the shares are trading at a 36.5% discount to an estimated US$104.84 per share. Which signal matters more to you: the earnings multiple, or the long term cash flow math?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out McCormick for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 881 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own McCormick Narrative

If this perspective does not quite match your view, or you would prefer to test the numbers yourself, you can build your own narrative in under three minutes by starting with Do it your way.

A great starting point for your McCormick research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you feel McCormick is only part of the story, do not stop here. Widen your watchlist now so you are not late to the next opportunity.

- Scan for potential mispricings by checking out these 881 undervalued stocks based on cash flows that may offer attractive cash flow profiles at current market prices.

- Spot emerging themes in digital assets by reviewing these 19 cryptocurrency and blockchain stocks that connect traditional markets with blockchain and cryptocurrency trends.

- Target income focused ideas by screening these 13 dividend stocks with yields > 3% that combine dividend yields above 3% with listed equity exposure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.