Measuring Tesla’s Valuation Gap As Narratives Clash On TSLA’s Future Growth

Tesla Motors, Inc. TSLA | 360.59 | -5.42% |

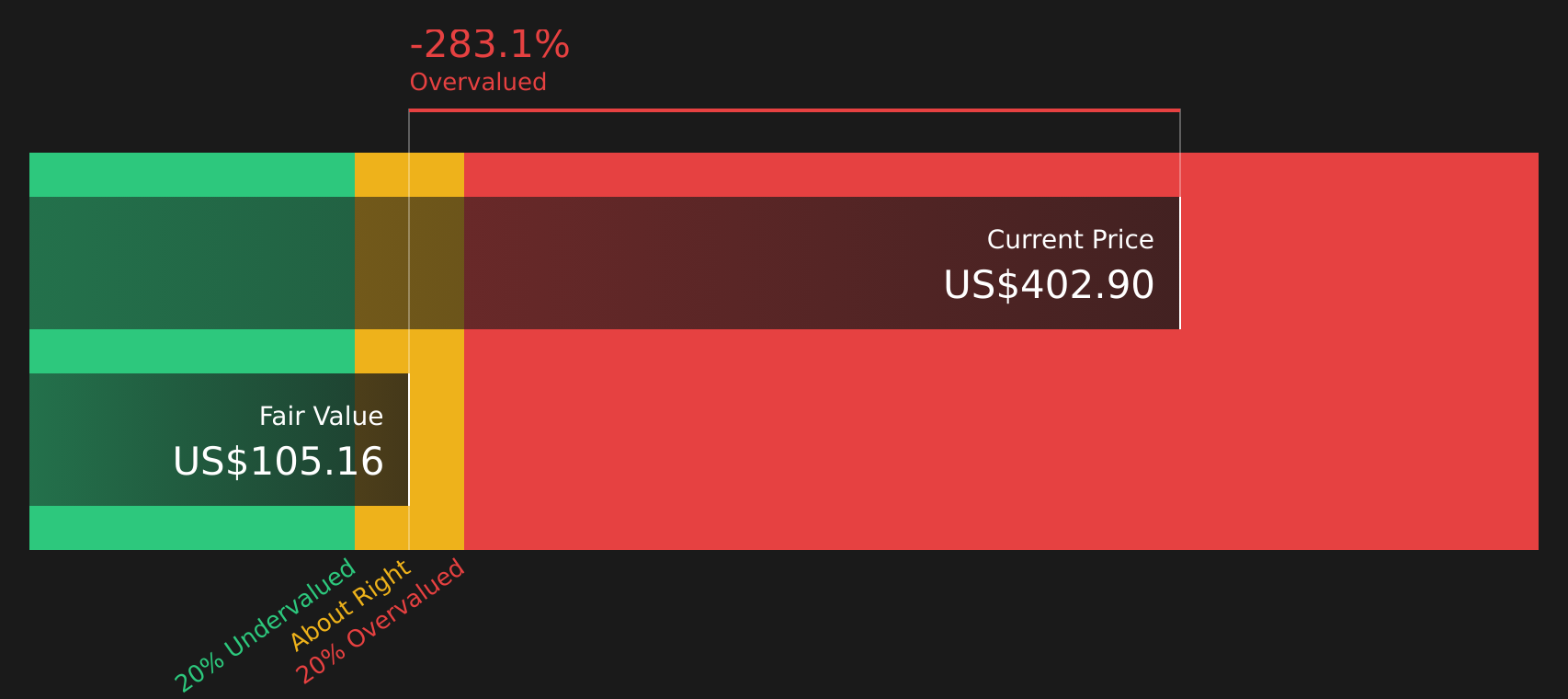

Tesla snapshot and recent returns

Tesla (TSLA) is trading around US$405.55, with a 1 day move close to flat, a small gain over the past week, and slight declines over the past month and past 3 months.

That recent softness in the share price comes after a stronger run, with a 1 year total shareholder return of 54.4% and a 3 year total shareholder return of about 1.3x, suggesting momentum has cooled even though long term holders have still seen substantial gains.

If Tesla’s moves have you thinking about the wider electric and AI ecosystem, it could be a good moment to see which 35 AI infrastructure stocks are catching attention right now.

With Tesla now roughly 4% below the average analyst price target and recent returns cooling after strong multi year gains, the key question is whether today’s price underestimates future growth. If the market already reflects these expectations, is there still a genuine buying opportunity, or is potential future growth already fully priced in?

Most Popular Narrative: 31.1% Undervalued

BlackGoat’s widely followed narrative puts Tesla’s fair value at about $588 per share, well above the last close of $405.55, which sets up a very different picture from the current market price.

For years, the debate has raged: Is Tesla a car company or a tech company? The Q4 2025 results did not just answer that with words, they answered it with structural action.

Forget the management slogans in the earnings call. The evidence that Tesla has effectively ceased to be a traditional automaker is now visible in three irreversible moves.

If you want to understand why this narrative lands on a much higher fair value, pay attention to how it treats future earnings power, margin potential, and the role of AI driven businesses alongside the existing automotive and energy operations.

Result: Fair Value of $588.18 (UNDERVALUED)

However, this bullish “physical AI” story still hinges on unproven pieces, especially large-scale robotaxi adoption and Optimus execution risk if timelines or regulation disappoint.

Another view on valuation

The $588 fair value from the narrative stands in sharp contrast to our DCF model, which indicates a future cash flow value of $128.72 per share. At around $405, Tesla appears expensive using this method. When two frameworks disagree this much, which one would you rely on?

Next Steps

With such mixed signals on Tesla’s value, do you feel the story leans more to risk or reward, and are you ready to test your own view quickly by weighing up the 1 key reward and 3 important warning signs for yourself?

Looking for more investment ideas?

If Tesla has sharpened your thinking, do not stop here. Broaden your watchlist with other focused ideas that could suit different goals and risk levels.

- Target resilient income potential by checking out 14 dividend fortresses that might help anchor your portfolio with regular cash flows.

- Hunt for quality at a sensible price by scanning 47 high quality undervalued stocks that our filters highlight for solid fundamentals and attractive pricing.

- Spot tomorrow’s potential standouts early by reviewing the screener containing 24 high quality undiscovered gems that many investors may not be watching yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.