Medtronic Stock And 2 Dividend Value Picks For Higher Rates

Medtronic Plc MDT | 0.00 |

With the Federal Reserve keeping rates at 3.5% to 3.75% but signaling a tougher line on inflation, many investors are rethinking where steady income might come from if borrowing costs stay higher for longer. Dividend-paying value stocks with solid balance sheets and moderate payout ratios can look relatively appealing when policy is uncertain and market swings pick up. This article walks through three stocks from a Dividend-Paying Value Stocks screener that appear closely exposed to the latest Fed shift, explaining why some investors may see them as potential opportunities for income, or decide to stay cautious instead.

Medtronic (MDT)

Overview: Medtronic is a large global medical device company that supplies hospitals and clinicians with products for heart conditions, brain and spine disorders, surgery, and diabetes care, from pacemakers and heart valves to surgical tools and insulin pumps.

Operations: Medtronic generates most of its roughly US$36.4b in annual revenue from the Cardiovascular segment at about US$14.0b, followed by Neuroscience at about US$10.3b and Medical Surgical at about US$8.8b, with sales broadly split between the United States and the rest of the world.

Market Cap: US$105.0b

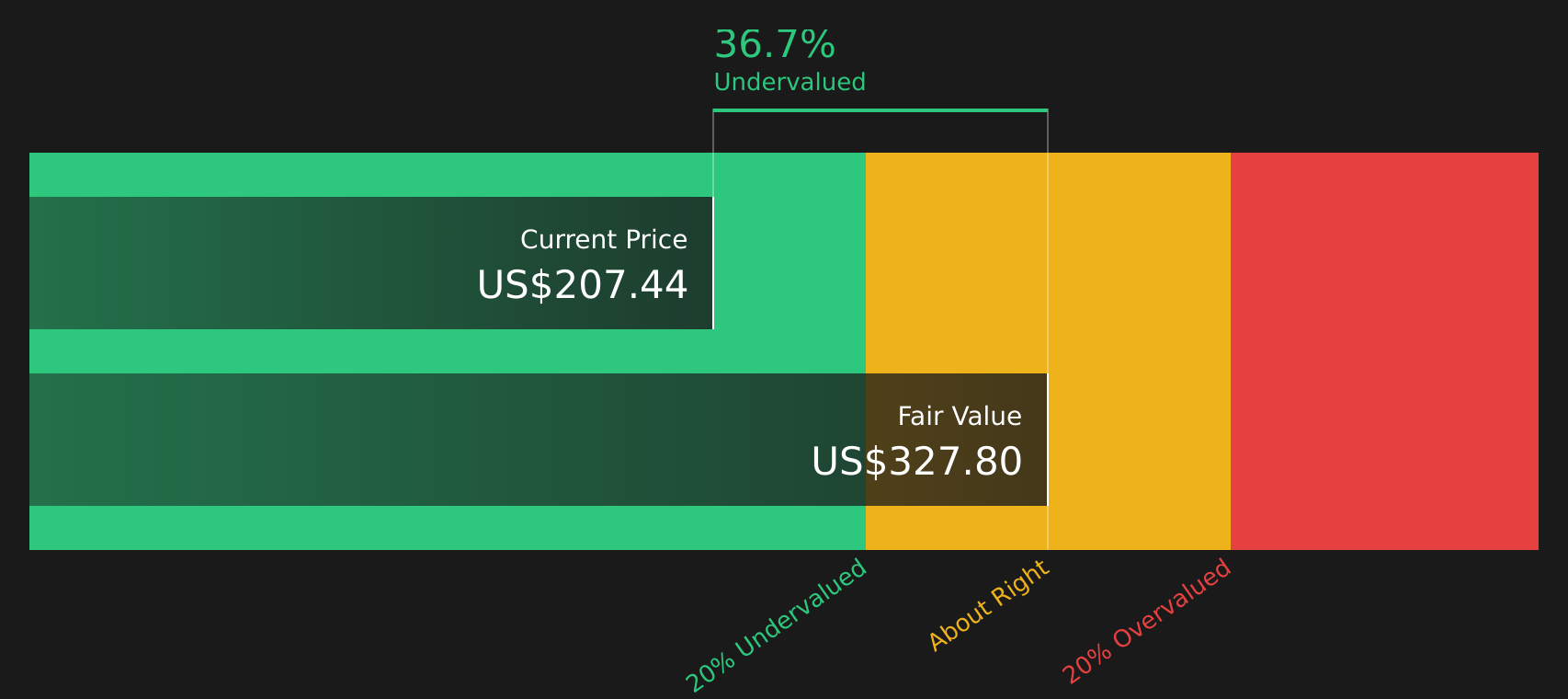

Medtronic stands out in a higher rate environment because it pairs a long dividend record and a roughly 3.45% yield with the scale and diversification to absorb policy shocks. At the same time, the stock trades on a P/E below many medical equipment peers. The company has a deep pipeline in areas such as cardiac ablation, robotics and AI enabled monitoring, and it has reported recent FDA clearances and acquisitions. These developments sit alongside margin pressure, device recalls and execution risk around major product launches and the planned Diabetes spin off, so the investment case has several moving parts. A key consideration for investors is how these factors compare with its current valuation and dividend profile.

Medtronic’s dividend track record, global scale and lower P/E could be masking what really matters now: how its next phase of growth stacks up against the risks flagged in the analysis report for Medtronic

Quest Diagnostics (DGX)

Overview: Quest Diagnostics is a large US-based medical testing company that runs a nationwide network of labs and patient service centers, providing everything from routine blood work to advanced cancer, neurology and prenatal genetic tests for doctors, hospitals, health plans, employers and consumers.

Operations: Quest Diagnostics generates about US$11.3b in annual revenue, with roughly US$11.0b coming from Diagnostic Information Services and about US$250m from DS Revenues, almost all earned in the United States.

Market Cap: US$23.0b

Quest Diagnostics attracts income focused investors because it combines a regular dividend with a business that many see as relatively resilient when rates stay higher for longer, supported by demand for essential lab testing and newer oncology tools like the Haystack MRD liquid biopsy. At the same time, the stock is flagged as trading below some cash flow based fair value estimates. Automation, AI and health data partnerships are working to lift productivity and deepen its role in preventive care and consumer wellness. The flip side is meaningful debt, reimbursement and policy risk, plus a growth profile that is solid rather than rapid. Some investors therefore treat Quest as a potential defensive income idea that still warrants close attention to funding and regulatory trends.

Quest Diagnostics’ income story, automation push and lab footprint may be only half the picture, with valuation signals hinting at something more. See how the full thesis stacks up in the analysis report for Quest Diagnostics.

Genesis Energy (NZSE:GNE)

Overview: Genesis Energy is a New Zealand utility that generates, trades, and sells electricity and gas to residential and business customers, using a mix of thermal, hydro, wind, and solar assets backed by its Kupe gas and LPG operations.

Operations: Genesis Energy earns most of its revenue in New Zealand from Wholesale activities of about NZ$2.4b and Retail at about NZ$2.3b, with Kupe contributing around NZ$112.2m and intersegment and adjustment items reducing the consolidated total.

Market Cap: NZ$3.4b

Genesis Energy catches the eye because it mixes a traditional utility profile with clear moves into batteries, renewables and EV charging, at a time when the Federal Reserve has signaled tighter policy and investors are looking more closely at cash flow resilience. Reported earnings growth over 5 years of 11.9% a year and a 5.6% net margin sit alongside high debt, an unstable dividend record and dilution in the past year, so income may require active monitoring. The new 200 MW / 400 MWh battery build at Huntly, funded after a NZ$400m equity raise, could reshape how Genesis earns money from flexibility and grid services, but there are still 5 warning signs to weigh before deciding how it fits in a dividend-paying value portfolio.

Genesis Energy’s shift toward batteries and renewables could be masking what really matters for long term holders, so it is worth seeing how the 2 key rewards and 5 important warning signs line up in the 2 key rewards and 5 important warning signs (1 is major!)

The three dividend stocks covered here are just a starting point, with the full Dividend-Paying Value Stocks screener surfacing 21 more large, established companies that pair income potential with equally compelling stories around balance sheet strength and valuation. Use Simply Wall St to identify, filter and analyze the specific catalysts and narratives that matter to you so you can focus on the dividend opportunities that best fit your portfolio.

Take Control of Your Investment Journey

If Medtronic or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd?

Fresh opportunities do not stay quiet for long. Spot stocks building breakout momentum or quietly dropping into value territory while it matters, before the crowd catches up, and get in early.

- Scan for under the radar quality by checking companies in the 19 high quality undiscovered gems that pair strong fundamentals with stories the wider market has not fully caught yet.

- Target resilient balance sheets by reviewing the curated list of solid balance sheet and fundamentals (47 results) so you can focus on businesses that look built to handle tougher conditions.

- Ride powerful income trends by tracking high yield candidates in the 9 dividend fortresses before the strongest payers are crowded and yields start dropping.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.