MercadoLibre (MELI) Is Down 13.1% After Margin-Squeezing Growth Push In Credit And Logistics

MercadoLibre, Inc. MELI | 0.00 |

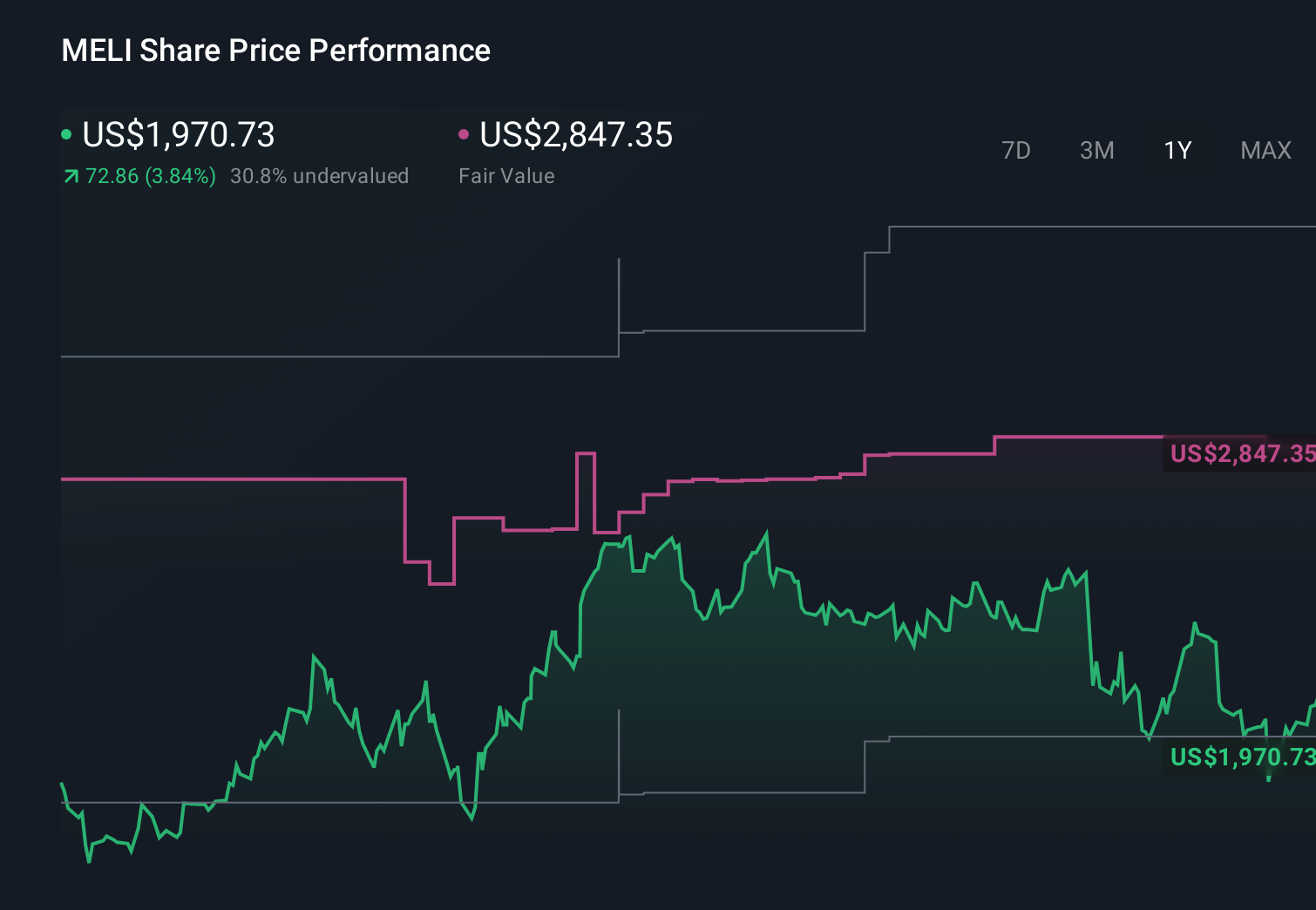

- In early May 2026, MercadoLibre reported first-quarter revenue of US$8.85 billion, up from US$5.94 billion a year earlier, while net income fell to US$417 million and earnings per share declined as heavier spending and higher loan-loss provisions weighed on profitability.

- The results highlighted how MercadoLibre’s push into credit cards, expanded free shipping in Brazil, and logistics upgrades is driving very large top-line growth but compressing margins as the company prioritizes long-term expansion over near-term profit improvement.

- We’ll now examine how this mix of stronger revenue but weaker margins, especially from Brazil shipping and credit costs, reshapes MercadoLibre’s investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

MercadoLibre Investment Narrative Recap

To own MercadoLibre today, you have to believe its integrated commerce and fintech platform across Latin America can justify heavy investment in shipping, logistics and credit. The latest quarter reinforced that trade off: revenue jumped to US$8.85 billion but net income and EPS fell as Brazil shipping costs and higher credit provisions hurt margins. That meaningfully increases the near term risk that credit losses and fulfillment spending keep profitability under pressure, even if revenue keeps growing.

Against that backdrop, the March 2026 plan to invest US$3.4 billion in Argentina this year looks especially important. It underlines how committed MercadoLibre is to building out logistics, new distribution centers and Mercado Pago across a key market right as margins are tightening. For catalysts, these investments can deepen the ecosystem and support user growth, but they also raise the stakes if credit quality or shipping economics do not improve as expected.

Yet behind the strong revenue story, rising credit provisions and Brazil shipping spend highlight a different risk profile that investors should be aware of...

MercadoLibre's narrative projects $57.9 billion revenue and $4.8 billion earnings by 2029. This requires 26.1% yearly revenue growth and a $2.8 billion earnings increase from $2.0 billion today.

Uncover how MercadoLibre's forecasts yield a $2440 fair value, a 55% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming revenue of about US$55.6 billion and earnings of US$4.4 billion by 2029, and Q1’s margin pressure could easily push their already pessimistic view of credit and competition risks even further, so it is worth weighing these more cautious scenarios against the more optimistic narratives before deciding how you see MercadoLibre’s future.

Explore 27 other fair value estimates on MercadoLibre - why the stock might be worth just $1827!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your MercadoLibre research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MercadoLibre research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MercadoLibre's overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.