MercadoLibre (MELI) Is Up 5.4% After $4.6 Billion Mexico Expansion Plan And Insider Buying - What's Changed

MercadoLibre, Inc. MELI | 0.00 |

- In recent days, MercadoLibre has attracted attention as easing geopolitical tensions, lower oil prices and yields, and strong Latin American e-commerce and fintech growth coincided with fresh insider share purchases and a multi-billion-dollar investment commitment in Mexico for 2026.

- Beyond the immediate macro boost, the company’s US$4.60 billion Mexico expansion and insider buying highlight management’s conviction in its long-term ecosystem build-out despite current margin pressure.

- Now, we’ll examine how this renewed investment push in Mexico might reshape MercadoLibre’s existing investment narrative and future expectations.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

MercadoLibre Investment Narrative Recap

To own MercadoLibre, you need to believe its e-commerce and fintech ecosystem can keep compounding in Latin America even as margins stay under pressure from credit growth and aggressive investment. The immediate share move on easing macro tensions and lower oil does not change that the key near term catalyst is sustained revenue growth alongside stable credit quality, while the biggest risk remains that rising loan-loss provisions and heavy logistics spending keep profitability subdued longer than investors expect.

In that context, the announced US$4.60 billion investment in Mexico for 2026, focused on logistics, technology, and financial services, is highly relevant. It reinforces the core growth catalyst of deeper regional scale, but also amplifies existing risks around execution in logistics, margin pressure from free shipping and fulfillment, and potential overextension if competition or macro conditions in markets like Brazil, Mexico, and Argentina become more challenging.

Yet behind the growth story, investors should also be aware of rising credit and logistics costs that could pressure margins if...

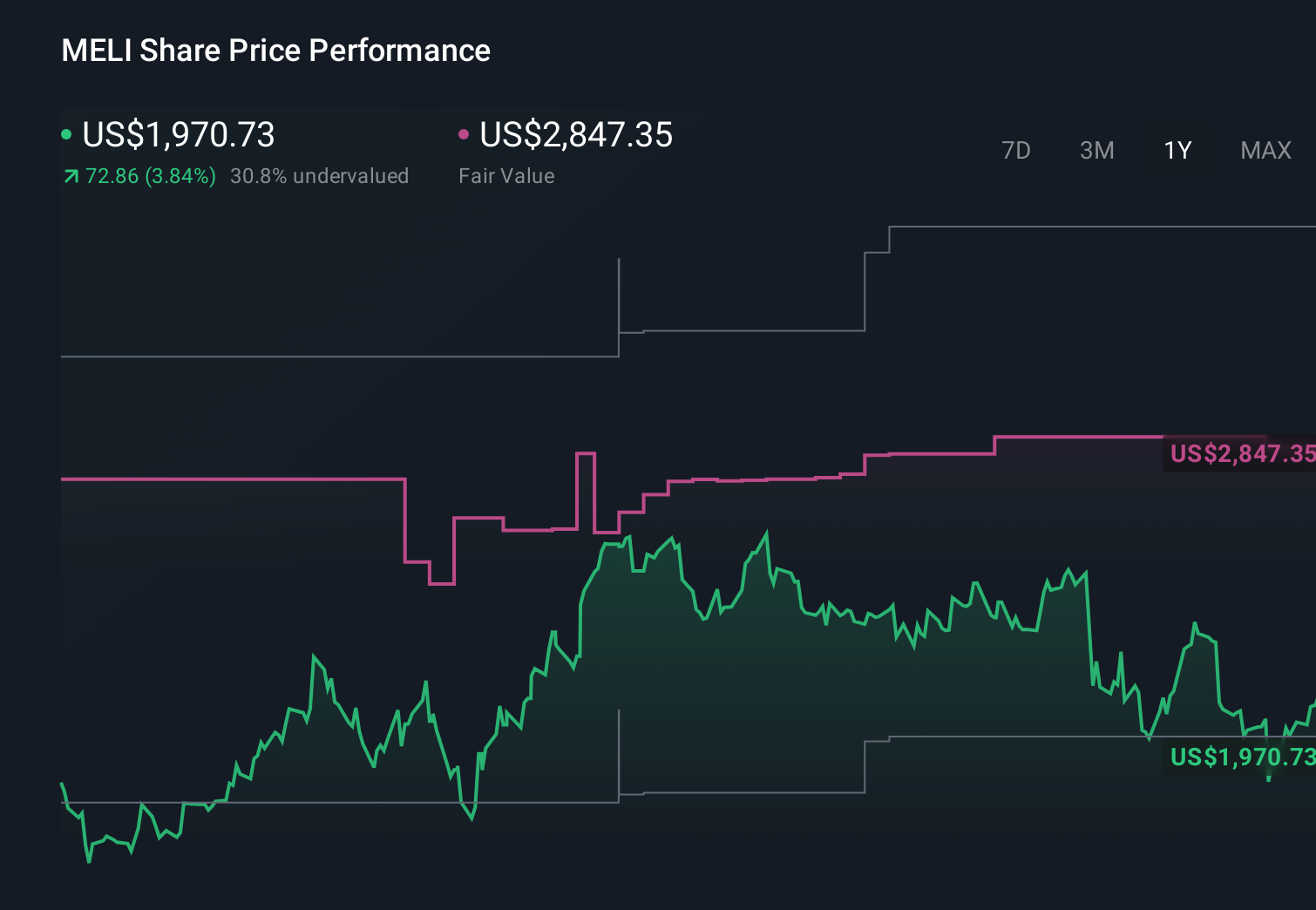

MercadoLibre's narrative projects $67.0 billion revenue and $4.7 billion earnings by 2029. This requires 28.2% yearly revenue growth and around a 2.5x earnings increase from $1.9 billion today.

Uncover how MercadoLibre's forecasts yield a $2217 fair value, a 32% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming revenue would reach about US$59.8 billion and earnings US$3.6 billion by 2029, and compared with the Mexico investment news they highlight how views on future margins and competitive pressure can differ widely, so you are encouraged to weigh several viewpoints before deciding what you believe is most likely.

Explore 23 other fair value estimates on MercadoLibre - why the stock might be worth as much as 96% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your MercadoLibre research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MercadoLibre research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MercadoLibre's overall financial health at a glance.

Seeking Other Investments?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 32 companies in the world exploring or producing it. Find the list for free.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.