MercadoLibre (MELI) Is Up 8.9% After Brazil Shipping Efficiency Surges And Demand Accelerates

MercadoLibre, Inc. MELI | 0.00 |

- In recent months, MercadoLibre reported accelerating growth in Brazil, with FX-neutral gross merchandise volume rising 38% in the first quarter, items sold climbing 56%, and unit shipping costs falling 17% despite higher volumes.

- This combination of faster demand growth and improving logistics efficiency in Brazil has reinforced the country’s role as a central engine of MercadoLibre’s broader ecosystem expansion across Latin America.

- We’ll now explore how Brazil’s improved shipping efficiency and growth momentum influence MercadoLibre’s existing investment narrative and longer-term outlook.

We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

MercadoLibre Investment Narrative Recap

To own MercadoLibre, you have to believe its e-commerce and fintech ecosystem can keep scaling across Latin America while balancing growth, credit risk, and profitability. Brazil’s faster FX-neutral GMV and item growth, alongside lower unit shipping costs, strengthens the short term catalyst of logistics-driven engagement, but does not remove the key risk that rising credit exposure and ongoing spending to win share could weigh on margins if conditions turn less favorable.

The Q1 2026 earnings release is especially relevant here: revenue reached US$8,845 million while net income slipped to US$417 million, reflecting the tension between investing for growth and preserving profitability. Combined with the Brazil shipping efficiency gains, these results highlight how heavily MercadoLibre’s thesis now leans on its ability to convert operational improvements into sustained earnings strength, despite more intense competition and a growing credit portfolio.

Yet behind the strong Brazil numbers, investors should still watch how MercadoLibre manages rising credit risk and competitive pressure across...

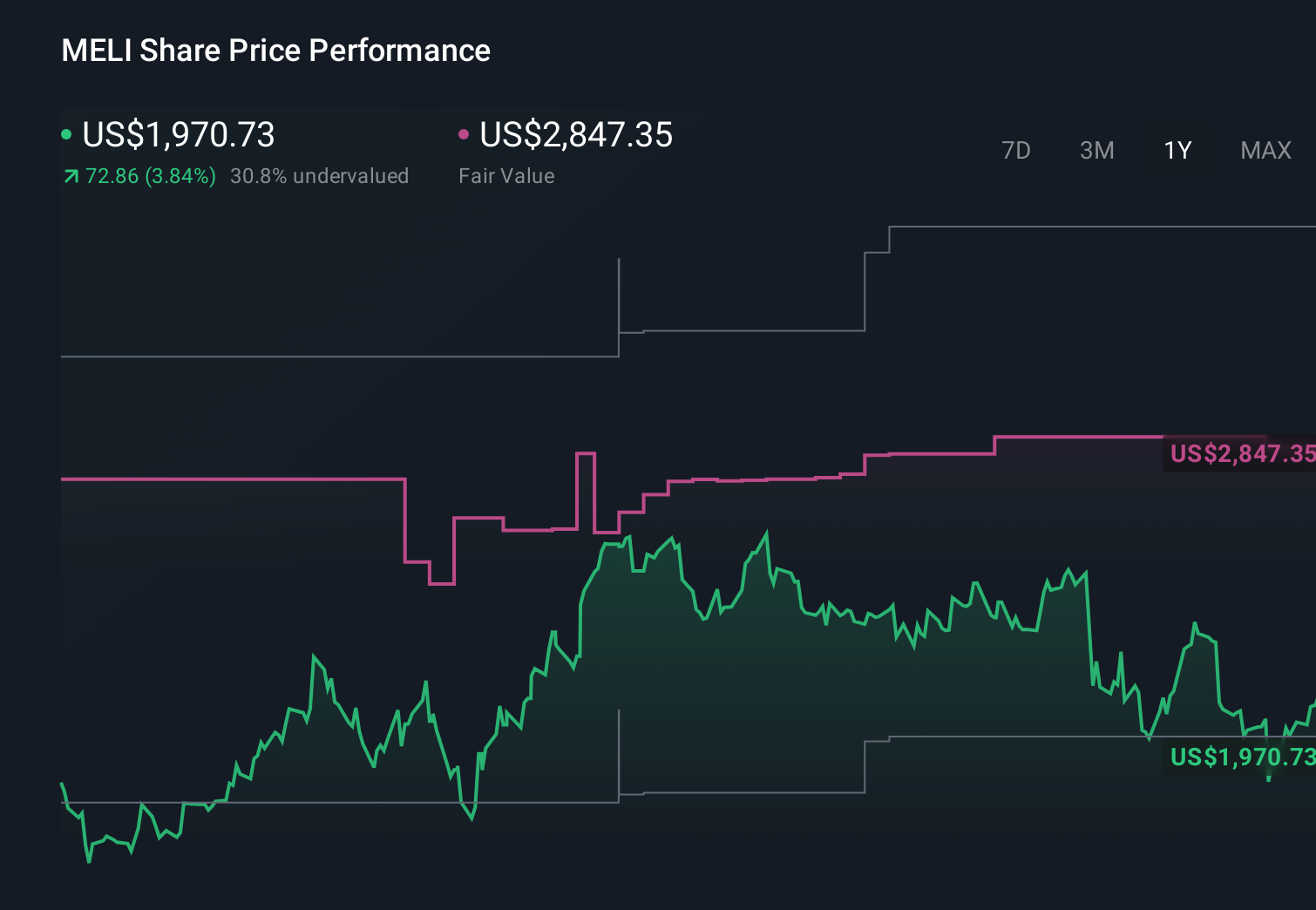

MercadoLibre's narrative projects $67.0 billion revenue and $4.7 billion earnings by 2029. This requires 28.2% yearly revenue growth and roughly a $2.8 billion earnings increase from $1.9 billion today.

Uncover how MercadoLibre's forecasts yield a $2217 fair value, a 26% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming revenue of about US$59.8 billion and flat 6 percent margins by 2029, so Brazil’s stronger logistics and growth could either soften or reinforce that pessimism depending on how you view the trade off between higher scale and rising competitive and credit risks.

Explore 22 other fair value estimates on MercadoLibre - why the stock might be worth just $1750!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your MercadoLibre research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MercadoLibre research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MercadoLibre's overall financial health at a glance.

Searching For A Fresh Perspective?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.