Merck (MRK) Following Keytruda Approvals And IDVYNSO Launch Looks Fully Valued

Merck & Co., Inc. MRK | 0.00 |

Merck (MRK) stock is in focus after fresh regulatory approvals for Keytruda in advanced cancers and the U.S. launch of IDVYNSO, a once daily HIV treatment, raised questions about how durable its growth engine may be.

Merck stock has been building momentum, with a 21.05% year-to-date share price return and a 63.66% total shareholder return over the past year, as fresh Keytruda approvals, IDVYNSO’s launch and new index inclusion reshape investor expectations around its pipeline strength and future risk profile.

If oncology and HIV news has you rethinking your watchlist, this is a good moment to scan a focused list of 40 healthcare AI stocks for more potential ideas in healthcare.

Given Merck’s double digit returns and fresh approvals in oncology and HIV, you need to judge whether the stock’s rerating reflects sturdier cash flow potential or investors leaning more heavily into the story. The valuation work starts there.

Most Popular Narrative: 70% Undervalued

Merck's most followed narrative pegs fair value at $129.74 per share, which sits just above the recent $128.86 close, yet still frames the stock as heavily undervalued on a discounted cash flow basis.

The analysts have a consensus price target of $129.74 for Merck based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $150.0, and the most bearish reporting a price target of just $100.0.

Read the complete narrative. Read the complete narrative.

Want to understand why this Merck view still lands on a steep discount to DCF fair value? The narrative leans on rising margins, stronger earnings power and a future profit multiple that assumes the market will keep rewarding that shift. Curious which specific growth and profitability assumptions sit under that headline fair value?

Result: Fair Value of $129.74 (UNDERVALUED)

However, this Merck narrative could be challenged if Keytruda’s loss of exclusivity hits revenues harder than expected, or if pricing pressure in key markets tightens faster.

Another View: What Merck’s P/E Is Telling You

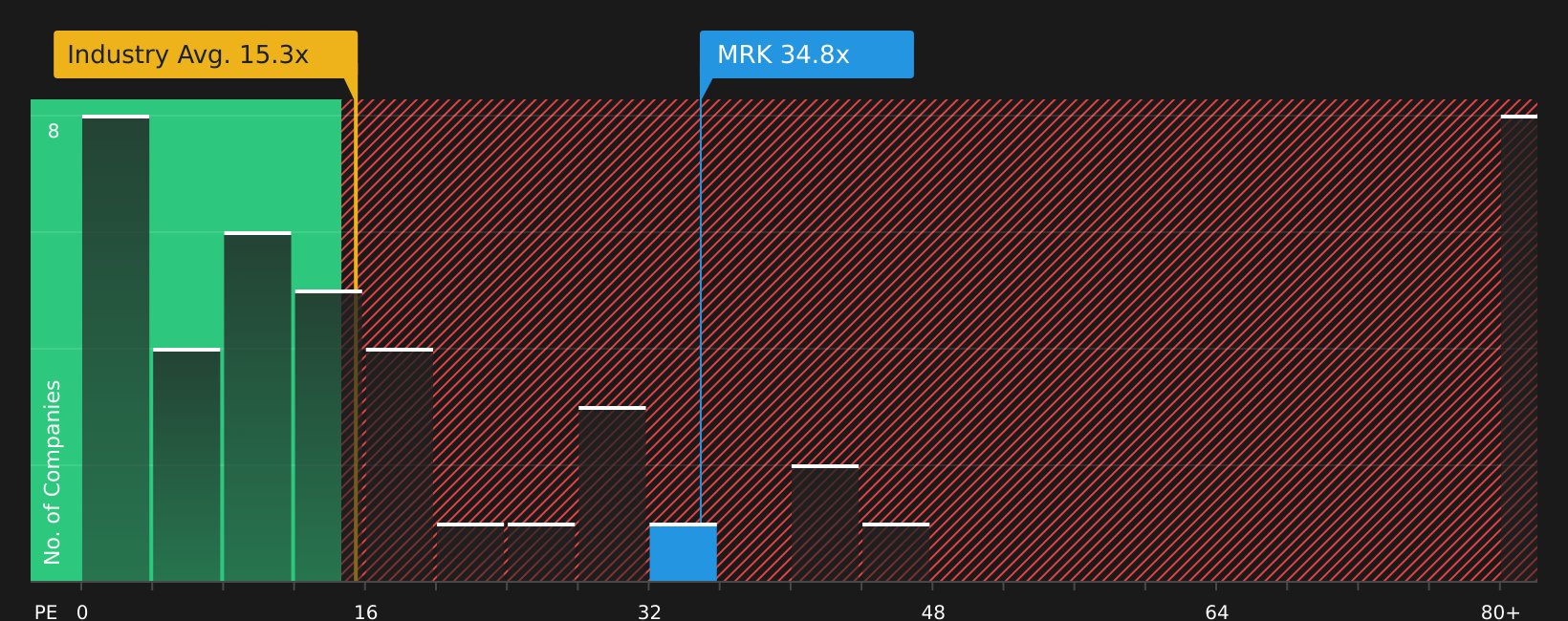

While the Merck narrative leans on discounted cash flows and a fair value of $129.74 per share, the current 35.6x P/E paints a very different picture. That is higher than the US Pharmaceuticals industry at 15.5x, the peer average at 27.2x, and even the 34.8x fair ratio the market could move toward. For investors, that gap points to valuation risk if sentiment cools or earnings slip. How comfortable are you paying a premium for this story?

Next Steps

With Merck priced for a strong story but facing clear questions on risk and reward, this is the moment to look through the numbers yourself, weigh the trade offs, and see what stands out in the 2 key rewards and 4 important warning signs.

Looking for more investment ideas beyond Merck?

If Merck has sharpened your focus on quality and risk, do not stop here. Widen your search and pressure test your next moves with curated stock shortlists.

- Target resilience first by reviewing companies highlighted in the 74 resilient stocks with low risk scores before committing fresh capital.

- Hunt for value by scanning the 45 high quality undervalued stocks when you want solid businesses that might be trading at appealing prices.

- Prioritise balance sheet strength by checking the solid balance sheet and fundamentals stocks screener (47 results) so potential weak spots do not catch you off guard.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.