MetroCity Bankshares (MCBS) Net Margin Strength Reinforces Bullish Profitability Narratives

MetroCity Bankshares MCBS | 29.36 | +0.86% |

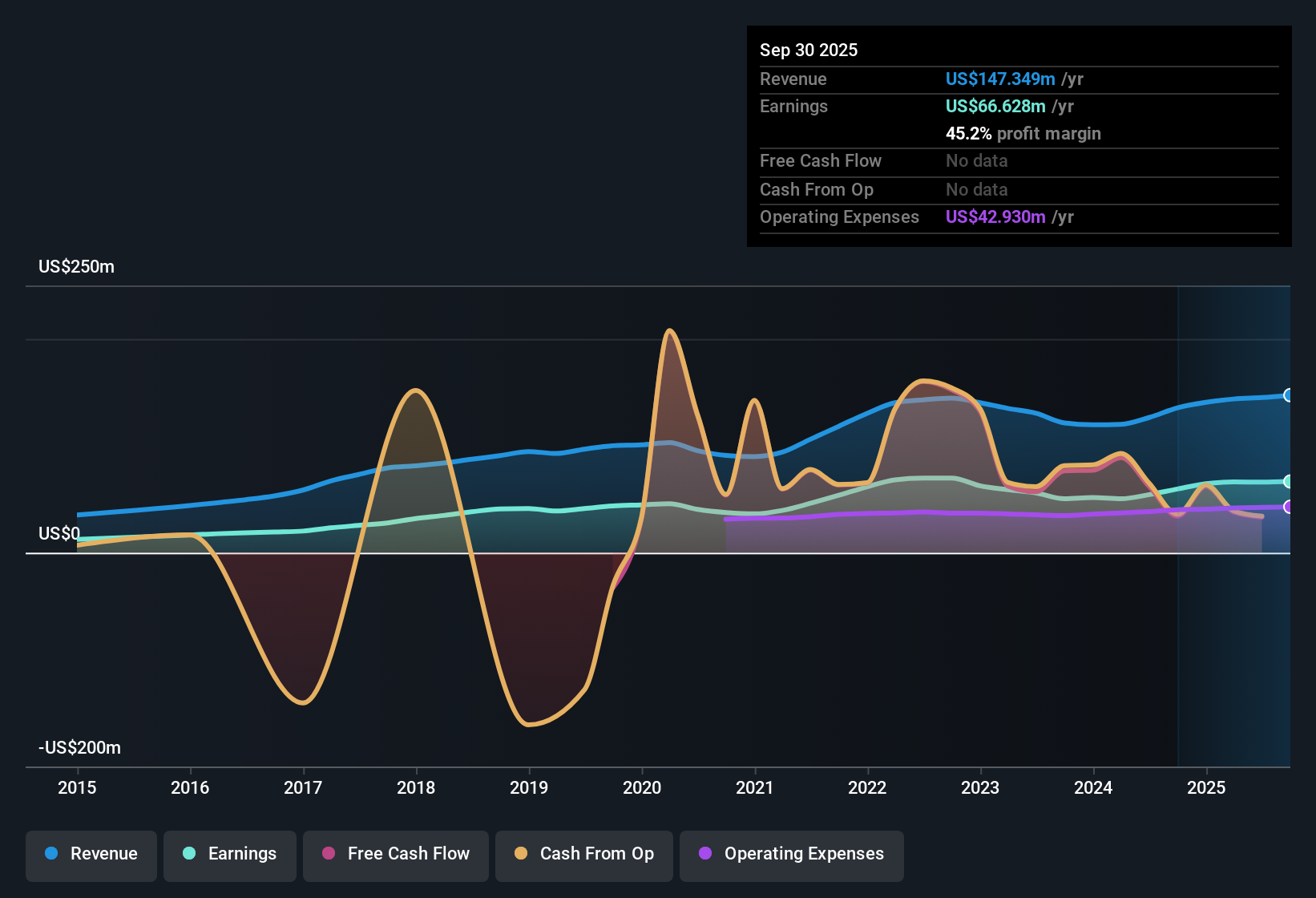

MetroCity Bankshares (MCBS) has reported Q3 FY 2025 results with total revenue of US$38.5 million and basic EPS of US$0.68, alongside net income of US$17.3 million, giving investors a fresh read on the bank’s earnings power. The company has seen trailing twelve month revenue shift from US$126.4 million in Q2 2024 to US$147.3 million in Q3 2025, with EPS over that same trailing window moving from US$2.15 to US$2.62. This sets up a results season where margins and earnings quality are front of mind.

See our full analysis for MetroCity Bankshares.With the latest numbers on the table, the next step is to see how this earnings profile lines up with the most widely held narratives about MetroCity Bankshares and where those stories might need to be updated.

45.2% net margin underpins earnings quality

- Over the last 12 months, MetroCity Bankshares converted US$147.3 million of revenue into US$66.6 million of net income, which works out to a 45.2% net profit margin compared with 44% in the prior year.

- Supporters of a bullish view often point to this high profitability, and the recent 11.8% earnings growth rate, as evidence of a solid core franchise, yet that same bullish stance has to square with a five year earnings growth rate of 5.5%, which is slower than the most recent year and suggests history has been steadier rather than rapid.

- The latest trailing EPS of US$2.62 versus US$2.15 a year earlier aligns with the idea of stronger recent profit expansion, but the longer-run 5.5% annual growth rate anchors expectations in a more moderate trend.

- The margin moving from 44% to 45.2% over the same period fits the bullish argument that profitability is healthy, while also reminding you that the change has been incremental rather than dramatic.

Stronger margins and faster recent earnings growth are exactly what bullish investors like to see in a bank, especially when they are backed by a full year of numbers rather than just one quarter. 📊 Read the full MetroCity Bankshares Consensus Narrative.

Loan book near US$3.0b with improving credit metrics

- Total loans stood at US$2.97b at the end of Q3 FY 2025, with non performing loans at US$13.0 million, compared with US$18.0 million in Q4 FY 2024 across a slightly larger loan book of US$3.17b.

- What is interesting for a more bullish interpretation is that credit quality metrics based on these figures look firmer over the trailing year, yet the overall earnings growth profile of 11.8% sits relatively close to the recent revenue base of US$147.3 million, which suggests that profit progress is coming alongside, not purely from, a shrinking risk bucket.

- Non performing loans moving from US$18.0 million to US$13.0 million while loans sit near US$3.0b generally lines up with bulls focusing on disciplined lending, but it also means future improvement may have a smaller absolute impact as that non performing base gets lower.

- The fact that quarterly net income has been clustered in a tight range, from US$16.2 million in Q4 FY 2024 to US$17.3 million in Q3 FY 2025, shows the bank is earning steadily on this loan book, which some bullish investors like, even if it does not point to a rapid shift in the earnings mix.

P/E of 10.8x with DCF fair value at US$45.35

- The shares trade on a trailing P/E of 10.8x at a price of US$28.17, slightly above the peer average of 10.7x and below the broader US Banks industry at 11.8x, while a DCF fair value of US$45.35 and a 3.55% dividend yield sit alongside trailing EPS of US$2.62.

- Critics who question how much valuation support is really on offer highlight that the P/E is almost identical to peers, even with the stock trading about 37.9% below the DCF fair value, which creates a tension between the DCF signal and the peer based comparison that investors need to be comfortable with.

- The close match between the 10.8x P/E and the 10.7x peer average suggests the market is pricing MetroCity Bankshares in line with similar banks, while the gap between US$28.17 and the US$45.35 DCF fair value is much wider than that peer based signal alone might imply.

- The 3.55% dividend yield, backed by trailing net income of US$66.6 million, adds a cash return on top of that valuation picture, which some investors see as helpful when weighing up whether the DCF fair value or the peer level P/E carries more weight.

When you line up a peer like P/E, a higher DCF fair value and Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on MetroCity Bankshares's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

MetroCity Bankshares shows steady earnings and healthy margins, but the modest five year earnings growth rate and tight recent profit range point to more measured progress.

If you want exposure to companies that already show more consistent and stronger expansion, check out our stable growth stocks screener (2167 results) and quickly line up alternatives with a clearer growth rhythm.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.