Microchip Technology (MCHP) Is Down 6.1% After Earnings Beat And New Rugged Oscillator Launch - What's Changed

Microchip Technology Incorporated MCHP | 0.00 |

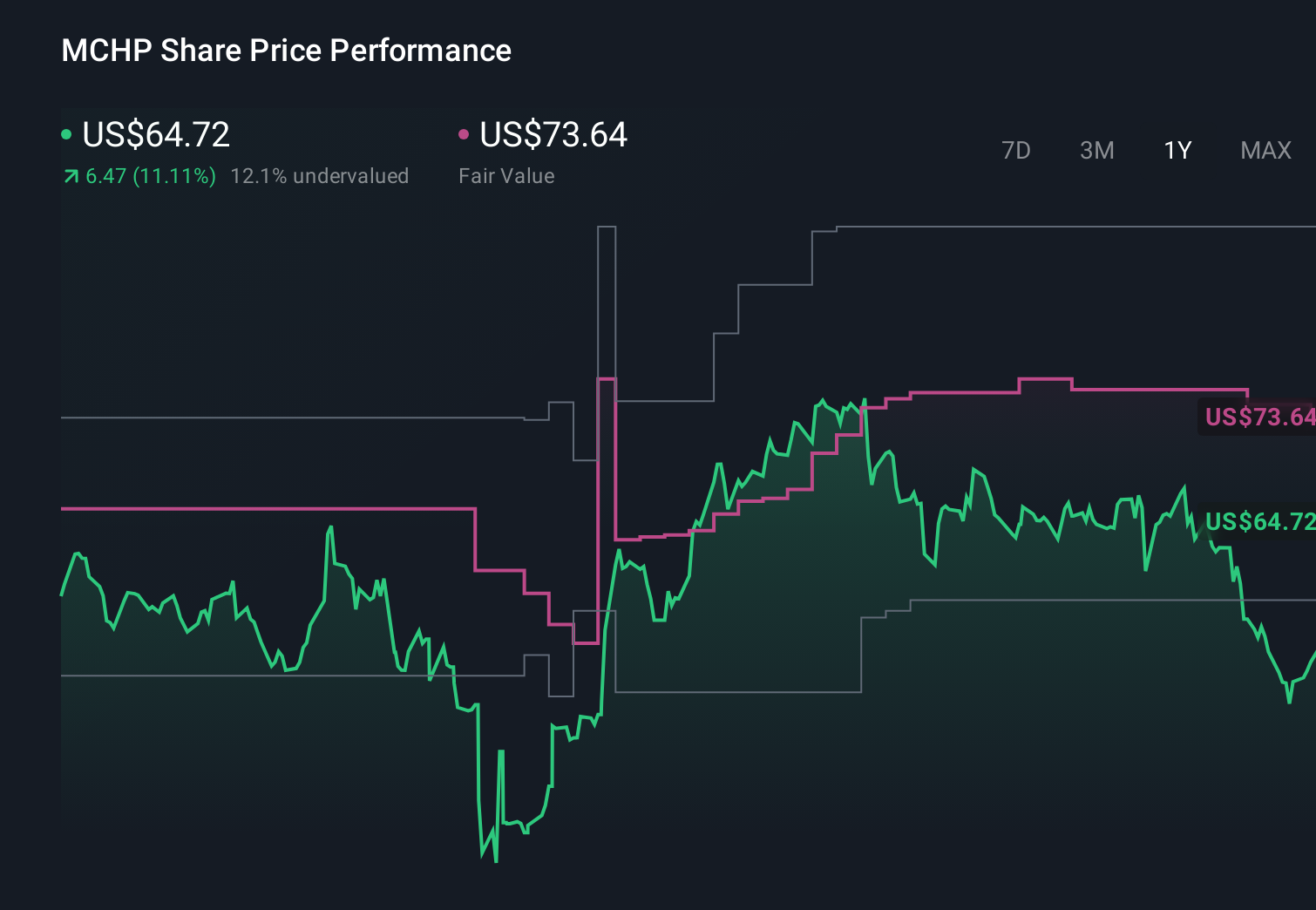

- In May 2026, Microchip Technology reported strong fiscal Q4 and full-year 2026 results, beating prior earnings guidance, tightening inventory, and returning US$984 million to shareholders via dividends while guiding to higher sales and margins for Q1 2027.

- Alongside these results, Microchip launched its EX-423 evacuated miniature crystal oscillator for high-reliability markets, underscoring how niche, ruggedized timing products may broaden its reach in defense, communications, and industrial applications.

- Next, we’ll examine how the earnings beat and margin-focused outlook could reshape Microchip Technology’s existing investment narrative and risk balance.

Find 53 companies with promising cash flow potential yet trading below their fair value.

Microchip Technology Investment Narrative Recap

To own Microchip Technology today, you largely need to believe that its recovery plan can translate improving demand, tighter inventories, and disciplined margins into healthier earnings, while the balance sheet and capital returns remain manageable. The latest upside surprise in Q4 FY2026 and higher Q1 FY2027 sales and margin guidance support that near term earnings catalyst. At the same time, high leverage and interest coverage remain a central risk that this quarter’s progress has not fully resolved.

The EX-423 evacuated miniature crystal oscillator launch matters here because it highlights Microchip pushing deeper into high reliability timing for defense, communications, and industrial gear, areas that can support mix and margin improvement rather than only volume growth. If these ruggedized products gain traction alongside improving utilization and inventory trends, they may reinforce the margin story that underpins many investors’ expectations, even as cyclical and balance sheet risks remain in focus.

Yet behind the stronger quarter, investors should still pay close attention to Microchip’s elevated debt load and how rising interest costs could...

Microchip Technology's narrative projects $7.3 billion revenue and $1.9 billion earnings by 2029. This requires 18.5% yearly revenue growth and about a $2.1 billion earnings increase from -$154.4 million today.

Uncover how Microchip Technology's forecasts yield a $86.67 fair value, a 5% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts painted a far more cautious picture, expecting revenue of about US$7.2 billion and earnings near US$2.0 billion by 2029, so if you only read the headline beat and guidance, you might miss how much opinions differ and why it helps to weigh several competing views before deciding what this latest quarter really means for you.

Explore 4 other fair value estimates on Microchip Technology - why the stock might be worth 24% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Microchip Technology research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Microchip Technology research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Microchip Technology's overall financial health at a glance.

Searching For A Fresh Perspective?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.