Middle East Hidden Treasures Featuring Tab Gida Sanayi ve Ticaret And Two More Promising Stocks

ALRASHEED 9601.SA | 80.90 | +1.19% |

In recent weeks, Middle Eastern stock markets have experienced fluctuations amid geopolitical tensions and concerns over regional stability, with most Gulf equities slipping as a fragile truce has left investors on edge. Despite these challenges, opportunities remain for discerning investors who can identify promising stocks that offer resilience and growth potential in uncertain times. In this context, we explore three hidden gems from the region's market landscape, including Tab Gida Sanayi ve Ticaret, that show promise amidst the current economic backdrop.

Top 10 Undiscovered Gems With Strong Fundamentals In The Middle East

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Al Wathba National Insurance Company PJSC | 10.35% | 8.65% | -7.40% | ★★★★★★ |

| Nofoth Food Products | NA | 20.62% | 23.75% | ★★★★★★ |

| Tureks Turizm Tasimacilik Anonim Sirketi | 5.61% | 45.04% | 46.56% | ★★★★★★ |

| Terminal X Online | 10.00% | 13.43% | 45.34% | ★★★★★★ |

| Saudi Azm for Communication and Information Technology | NA | 17.85% | 23.54% | ★★★★★★ |

| MOBI Industry | 7.46% | 5.89% | 17.98% | ★★★★★★ |

| Najran Cement | 14.49% | -4.20% | -30.16% | ★★★★★★ |

| Baazeem Trading | 11.27% | -0.70% | -0.42% | ★★★★★☆ |

| Saudi Chemical Holding | 47.39% | 17.85% | 39.66% | ★★★★★☆ |

| Etihad GO Telecom | NA | 38.31% | 54.97% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

Tab Gida Sanayi ve Ticaret (IBSE:TABGD)

Simply Wall St Value Rating: ★★★★★★

Overview: Tab Gida Sanayi ve Ticaret A.S. operates and franchises fast food and restaurant chains in Turkey, with a market capitalization of TRY65.27 billion.

Operations: Tab Gida Sanayi ve Ticaret A.S. generates revenue primarily from its restaurant operations, totaling TRY47.64 billion. The company's financial performance is reflected in its market capitalization of TRY65.27 billion, indicating significant business scale within Turkey's fast food and restaurant industry.

With a Price-To-Earnings ratio of 24.8x, Tab Gida Sanayi ve Ticaret appears attractively valued compared to the Hospitality industry's average of 70.1x. Over the past year, earnings grew by 5%, outpacing the industry’s -15.6% performance, indicating resilience and potential for further growth. The company reported sales of TRY 47,636 million for 2025, up from TRY 41,897 million in the prior year, while net income reached TRY 2,628 million from TRY 2,502 million previously. With no debt on its books and high-quality earnings reported consistently over time, it seems poised for continued stability in its operations.

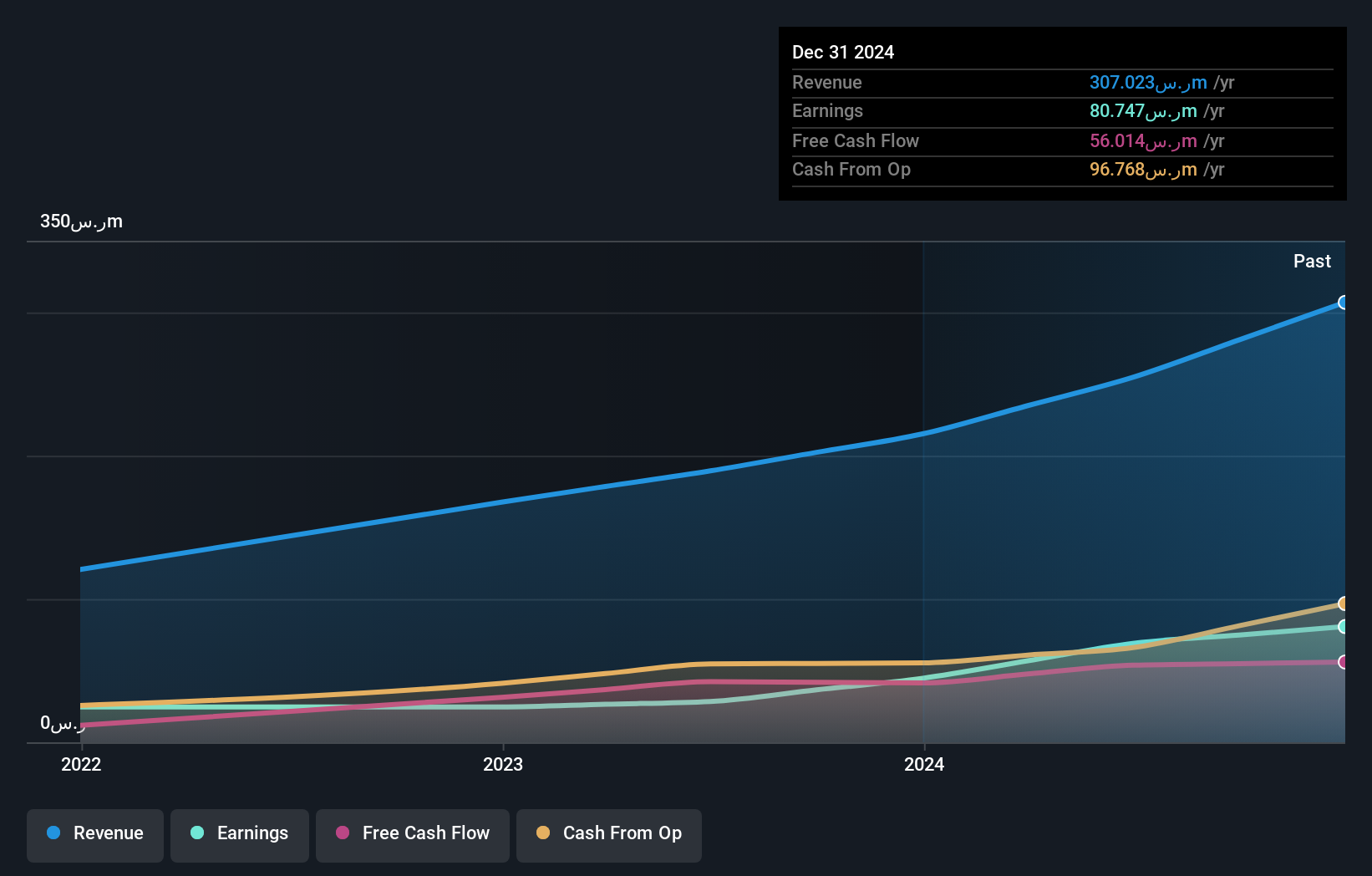

Mohammed Hadi Al-Rasheed (SASE:9601)

Simply Wall St Value Rating: ★★★★★☆

Overview: Mohammed Hadi Al-Rasheed Company specializes in the production of silica sand for diverse industrial uses and has a market capitalization of SAR1.40 billion.

Operations: The company generates revenue primarily from the production of silica sand for industrial applications. With a market capitalization of SAR1.40 billion, it focuses on leveraging its resources to cater to various industrial needs.

Mohammed Hadi Al-Rasheed's recent performance highlights its potential as a small cap player in the Middle East. Its earnings growth of 5.3% over the past year outpaced the Basic Materials industry's -6.8%. The company reported sales of SAR 347.7 million, up from SAR 307.02 million, with net income rising to SAR 85.01 million from SAR 80.75 million previously, although basic earnings per share dipped to SAR 4.72 from SAR 6.73 due to increased shares outstanding or other factors not detailed here. A price-to-earnings ratio of 16x suggests it trades below market average, while interest payments are well covered by EBIT at a robust multiple of nearly 190x, indicating strong financial health and management efficiency in handling debt obligations without straining resources significantly.

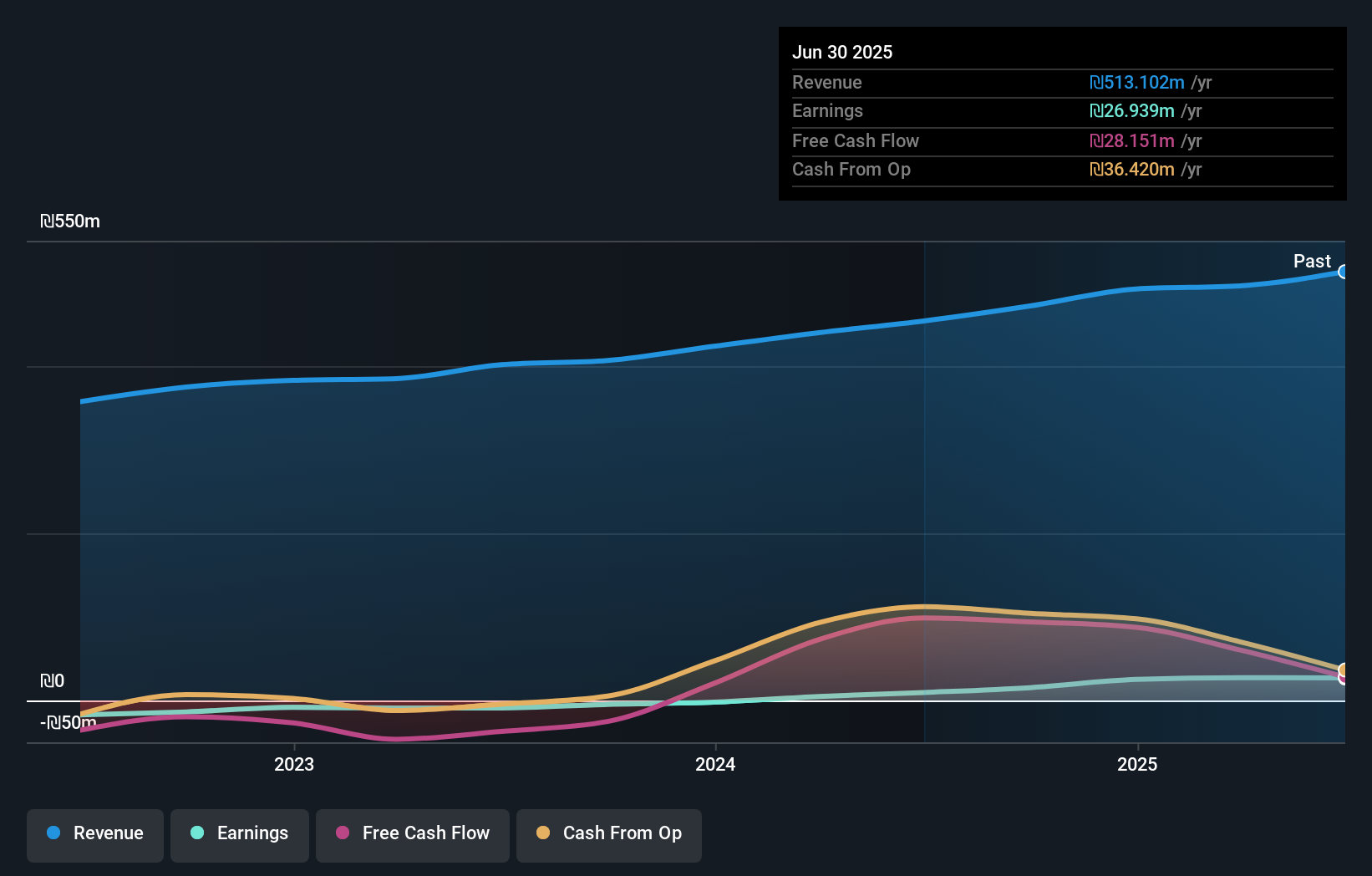

Terminal X Online (TASE:TRX)

Simply Wall St Value Rating: ★★★★★★

Overview: Terminal X Online Ltd. is involved in the marketing and sale of fashion and lifestyle products in Israel, with a market capitalization of approximately ₪964.41 million.

Operations: Terminal X Online Ltd. generates revenue primarily from its Terminal X segment, contributing ₪454.61 million, and its Independent Websites segment, adding ₪108.54 million. Adjustments account for a deduction of ₪2.91 million in the overall revenue calculation.

Terminal X Online has shown impressive financial resilience, with earnings growth of 12.5% over the past year, outpacing its industry peers. The company reported sales of ILS 560.24 million in 2025, up from ILS 492.34 million the previous year, and net income rose to ILS 28.36 million from ILS 25.21 million, indicating robust operational performance. With a debt-to-equity ratio reduced significantly from 527.5% to just 10% over five years and interest payments well-covered by EBIT at a multiple of 15.4x, Terminal X appears financially sound despite recent share price volatility in the market context.

Where To Now?

- Unlock more gems! Our Middle Eastern Undiscovered Gems With Strong Fundamentals screener has unearthed 219 more companies for you to explore.Click here to unveil our expertly curated list of 222 Middle Eastern Undiscovered Gems With Strong Fundamentals.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.