Middle East's Undiscovered Gems Featuring Three Promising Small Caps

NAYIFAT 4081.SA | 10.05 | -0.20% |

As geopolitical tensions between Israel and Iran escalate, most Gulf markets have seen a downturn, with key indices such as Saudi Arabia's benchmark experiencing declines. Despite this cautious market sentiment, small-cap stocks in the Middle East can offer unique opportunities for investors willing to explore beyond the usual blue-chip options. Identifying promising small caps often involves looking for companies with strong fundamentals and growth potential that can weather regional instability.

Top 10 Undiscovered Gems With Strong Fundamentals In The Middle East

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| MOBI Industry | 6.50% | 5.60% | 24.00% | ★★★★★★ |

| Alf Meem Yaa for Medical Supplies and Equipment | NA | 17.03% | 18.37% | ★★★★★★ |

| Baazeem Trading | 8.48% | -2.02% | -2.70% | ★★★★★★ |

| Sure Global Tech | NA | 11.95% | 18.65% | ★★★★★★ |

| Saudi Azm for Communication and Information Technology | 2.07% | 16.18% | 21.11% | ★★★★★★ |

| Nofoth Food Products | NA | 15.75% | 27.63% | ★★★★★★ |

| National General Insurance (P.J.S.C.) | NA | 14.55% | 29.05% | ★★★★★☆ |

| National Corporation for Tourism and Hotels | 19.25% | 0.67% | 4.89% | ★★★★☆☆ |

| Waja | 23.81% | 98.44% | 14.54% | ★★★★☆☆ |

| Saudi Chemical Holding | 79.49% | 16.57% | 44.01% | ★★★★☆☆ |

We're going to check out a few of the best picks from our screener tool.

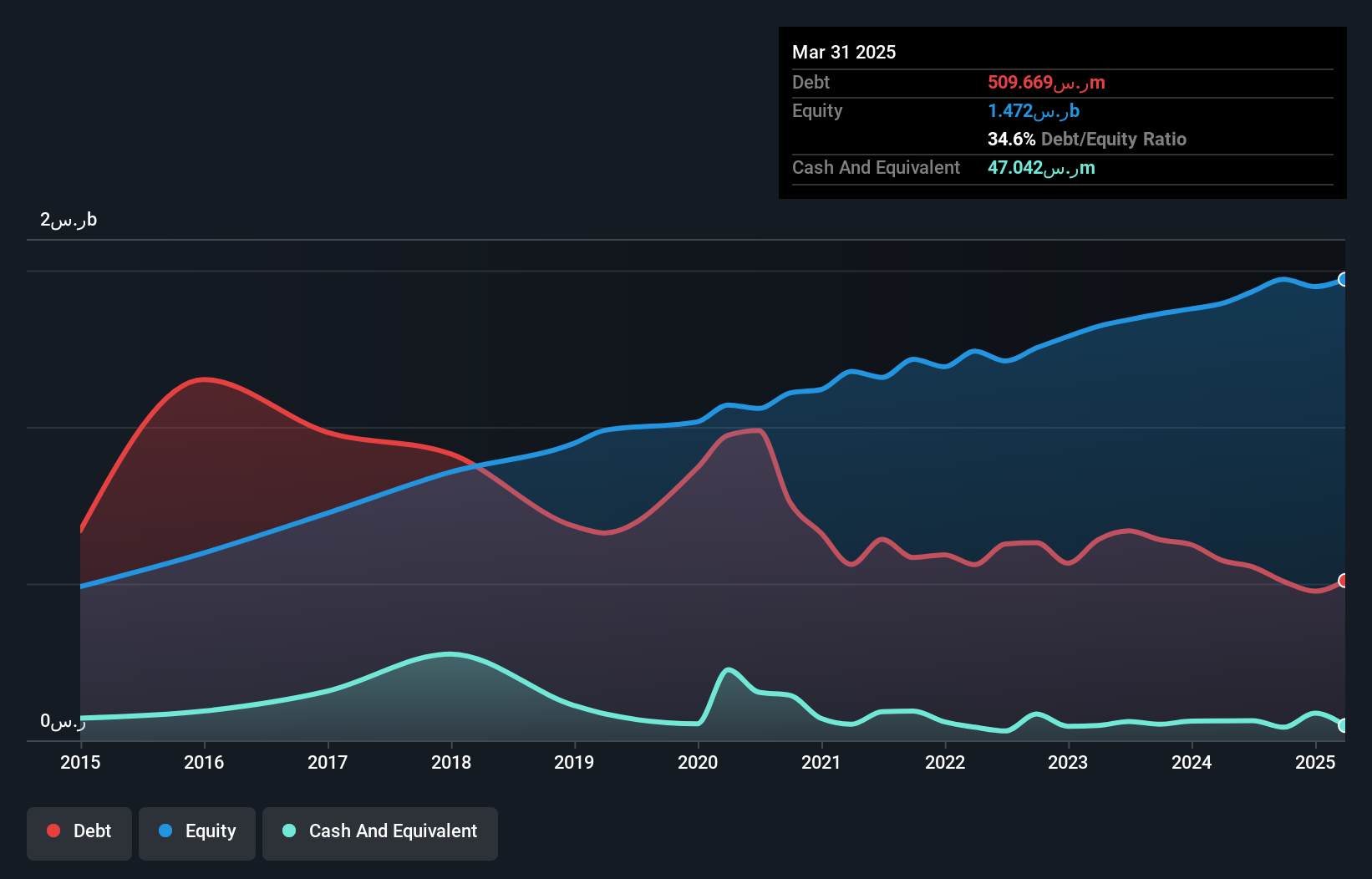

Anadolu Anonim Türk Sigorta Sirketi (IBSE:ANSGR)

Simply Wall St Value Rating: ★★★★★★

Overview: Anadolu Anonim Türk Sigorta Sirketi operates in Turkey providing a range of non-life insurance products, with a market capitalization of TRY42 billion.

Operations: Anadolu Anonim Türk Sigorta Sirketi generates revenue primarily from its non-life insurance segments, with significant contributions from Motor Vehicles (TRY14.17 billion) and Disease/Health (TRY10.38 billion) insurance products. The company also earns revenue from Motor Vehicles Liability and Fire and Natural Disasters insurance, contributing TRY9.16 billion and TRY5.25 billion respectively to its overall income streams.

Anadolu Sigorta, a prominent player in the insurance sector, has demonstrated robust growth with earnings increasing 65% annually over the past five years. Despite this impressive trajectory, recent performance indicates some challenges; net income for Q1 2025 was TRY 1.98 billion, down from TRY 2.87 billion the previous year, and basic earnings per share fell to TRY 3.95 from TRY 5.73. The company remains debt-free and trades at a valuation perceived as undervalued by about 16%. While not outpacing industry growth last year with only a 13.5% rise in earnings compared to the sector's broader gains, Anadolu Sigorta still boasts high-quality past earnings and positive free cash flow trends that suggest resilience amidst market fluctuations.

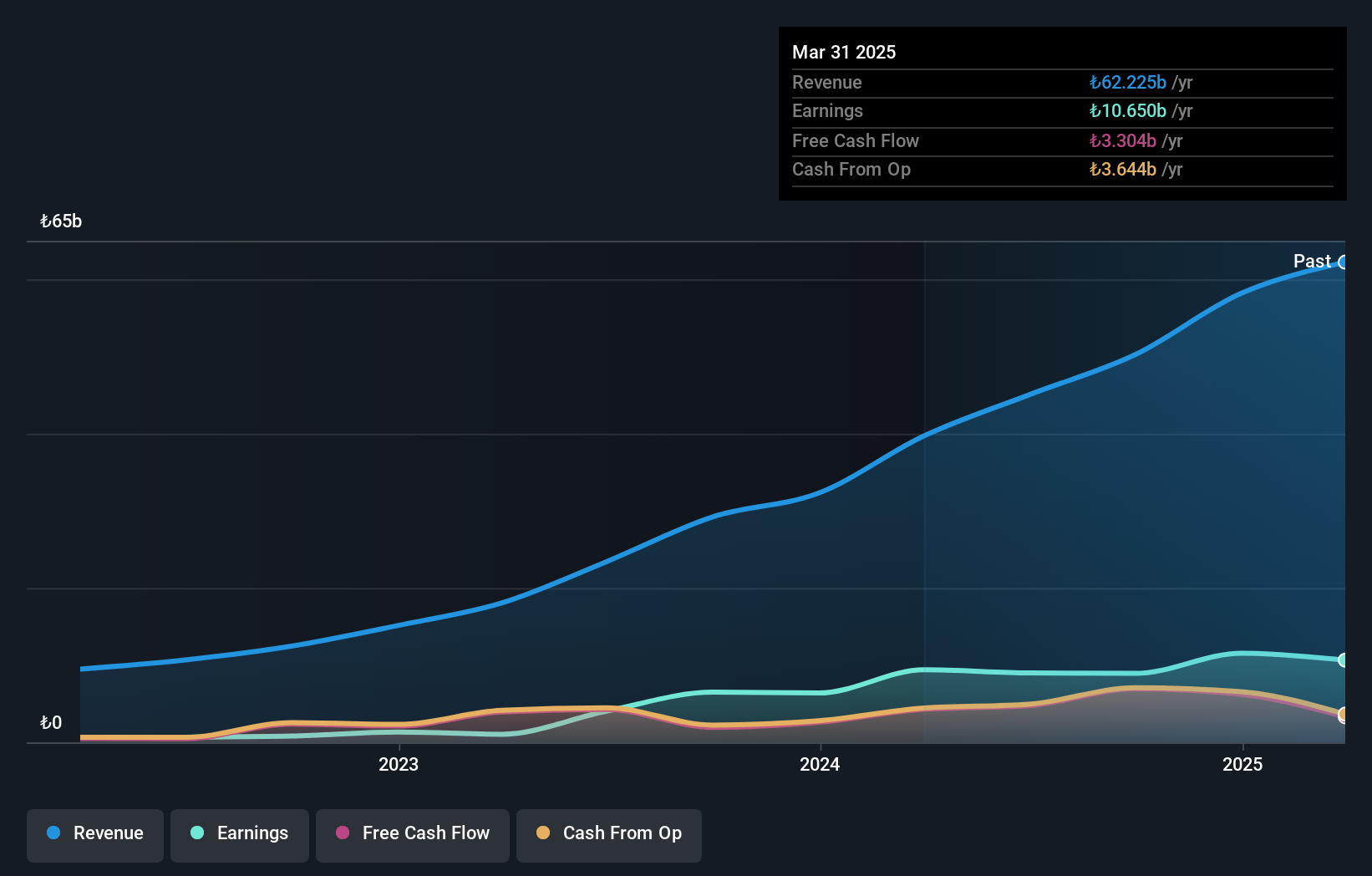

Nayifat Finance (SASE:4081)

Simply Wall St Value Rating: ★★★★★☆

Overview: Nayifat Finance Company specializes in offering personal financing solutions within the Kingdom of Saudi Arabia and has a market capitalization of SAR1.45 billion.

Operations: The company generates revenue primarily from personal financing, contributing SAR258.30 million, followed by SME financing at SAR43.05 million, and Islamic credit cards at SAR1.73 million.

Nayifat Finance, a notable player in the Middle East's financial sector, has demonstrated resilience with earnings growth of 87% over the past year, significantly outpacing the Consumer Finance industry's 8%. The company reported net income of SAR 23.55 million for Q1 2025, up from SAR 17.18 million a year earlier. Its debt management appears robust as the debt-to-equity ratio improved from 91% to a more manageable 35% over five years. Recently appointed Acting CEO Khalid Abdulaziz AlJenaidel brings extensive experience, potentially steering Nayifat towards strategic advancements amidst its promising valuation at a P/E ratio of just 10x against the market's average of about double that figure.

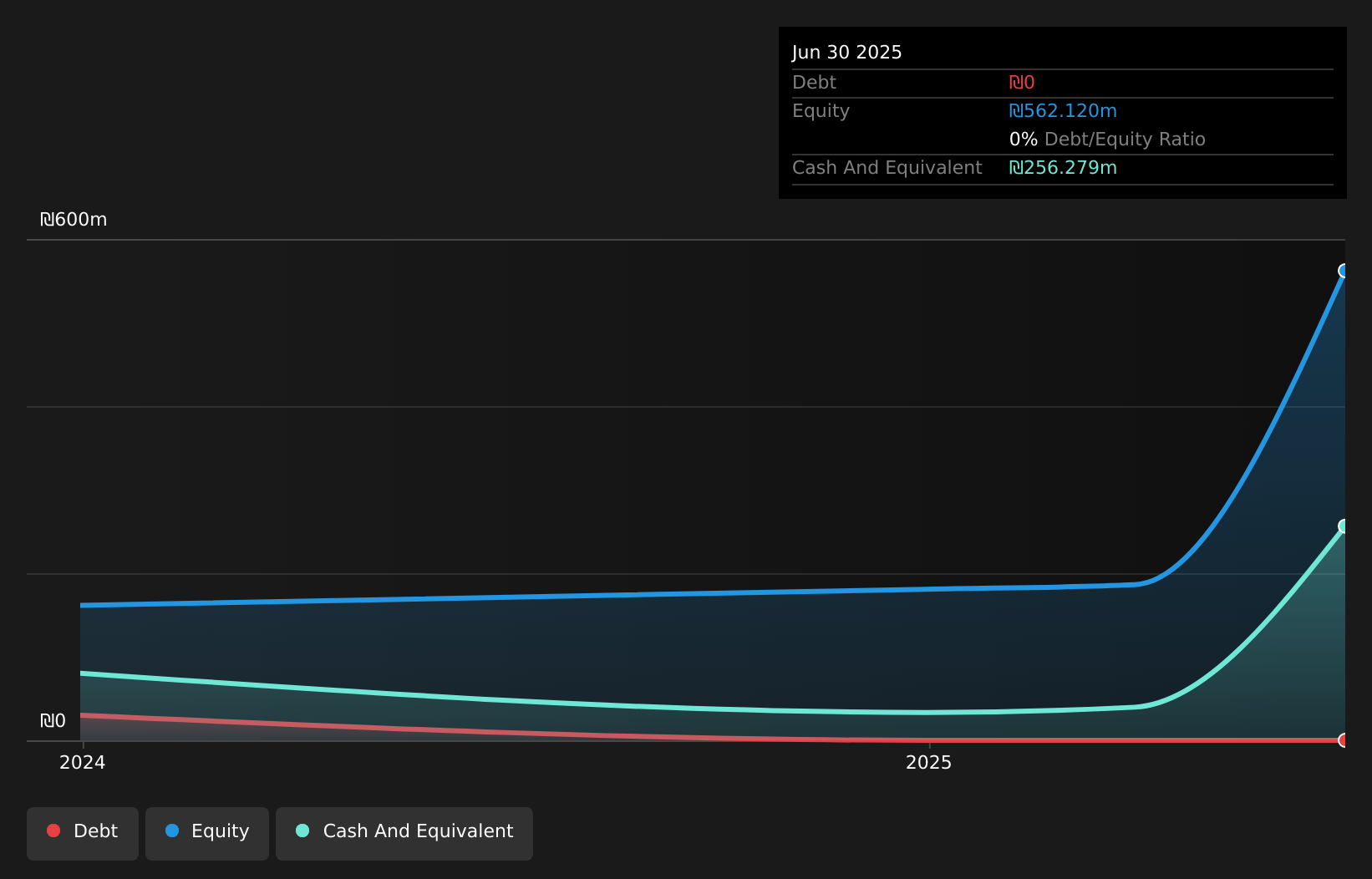

Urbanica (Palo) Retail (TASE:URBC)

Simply Wall St Value Rating: ★★★★★☆

Overview: Urbanica (Palo) Retail Ltd is involved in the design, purchase, marketing, and retail sale of clothing for women, men, and children in Israel with a market cap of ₪1.41 billion.

Operations: Urbanica generates revenue primarily from fashion clothing, contributing ₪487.01 million, and fashion accessories, adding ₪132.95 million.

Urbanica Retail, a small player in the Middle East retail sector, has shown impressive earnings growth of 69% over the past year, outpacing its industry peers. Despite generating less than US$1 million in revenue, this debt-free company boasts high-quality earnings and positive free cash flow. Recently completing an IPO worth ILS 410 million at ILS 10 per share, Urbanica seems poised for expansion. While it remains profitable with no debt concerns, its future trajectory will likely depend on how effectively it leverages the recent capital influx to boost revenue and market presence.

Where To Now?

- Discover the full array of 217 Middle Eastern Undiscovered Gems With Strong Fundamentals right here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.