Mirion Technologies (MIR): Assessing Valuation After Strong Earnings, Guidance Reaffirmation, and Investor Momentum

Mirion Technologies, Inc. Class A MIR | 0.00 |

Mirion Technologies (NYSE:MIR) released its third quarter results along with a confirmation of its full-year revenue outlook, showing both improved revenue and a return to profitability compared to last year. The update sheds light on recent investor attention.

Mirion’s recent financial updates have struck a chord with investors, underscored by the company’s 2.65% one-day share price return and a sustained 48.9% year-to-date share price gain. Momentum is clearly building, as seen in its stellar 79% total shareholder return over the past year and an impressive 3-year total return of 228%. These results set a strong tone around its growth narrative.

Curious what other stocks might be seeing similar momentum? Now is the perfect moment to broaden your search and discover fast growing stocks with high insider ownership

With shares riding strong gains on the back of robust revenue growth and improved profitability, the key question remains: do Mirion’s fundamentals suggest a bargain, or is the market already anticipating even more growth ahead?

Most Popular Narrative: 4.2% Undervalued

Mirion Technologies' most followed narrative sees its fair value at $26.29, just ahead of the last close price of $25.19. This close gap hints investors are weighing the company’s recent growth spurt against aggressive future expectations.

Strong momentum in advanced nuclear projects, including utility-scale new builds and rapid activity in the small modular reactor (SMR) market, has materially broadened Mirion's pipeline of large, multi-year opportunities. This has created potential for significant step-changes in future order intake, backlog, and top-line revenue.

What wild card is fueling analysts’ optimism? The narrative ramps up its valuation on one outsized growth lever, daring you to dig deeper into what justifies such future profits. Ready to see the financial leaps behind this upgrade?

Result: Fair Value of $26.29 (UNDERVALUED)

However, Mirion's heavy reliance on the nuclear sector and uncertain success with new acquisitions mean its growth path could face unexpected roadblocks.

Another View: Are Its Multiples Telling a Different Story?

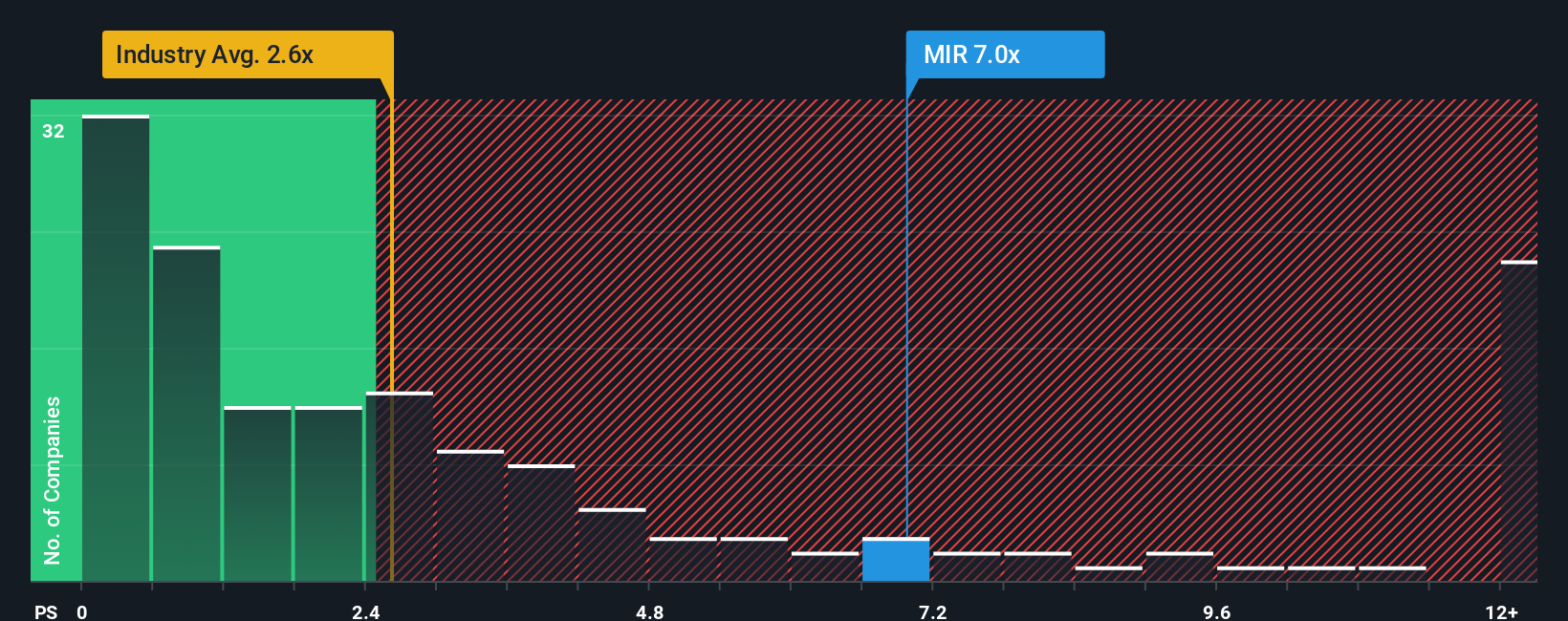

While the fair value estimate suggests Mirion is slightly undervalued, looking at standard market ratios offers a different perspective. The company trades at a price-to-sales ratio of 6.5 times, which is significantly higher than both its peer average of 3.9 times and the US electronics industry average of 3 times. For investors, this premium suggests that expectations for future growth are already reflected in the price, increasing the risk if performance falls short. Will the fundamentals support these high hopes?

Build Your Own Mirion Technologies Narrative

If our narrative does not match your conclusions, or if you want to dig into the numbers personally, you can chart your own view in just a few minutes. Do it your way

A great starting point for your Mirion Technologies research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Investment Moves?

Staying ahead in the market is about seizing unique, timely opportunities before the crowd. Don’t miss your chance to take control of your next winning idea.

- Tap into high yield potential by checking out these 21 dividend stocks with yields > 3%, which consistently deliver strong income with yields above 3%.

- Spot the next big wave in computing innovation and chart your path with these 28 quantum computing stocks for exposure to the fast-evolving quantum space.

- Cement your edge in artificial intelligence by browsing these 26 AI penny stocks, which are transforming industries with breakthroughs in automation and data-driven solutions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.