Mirum Buyout Of Bluejay Shifts Rare Liver Story Beyond Livmarli

Mirum Pharmaceuticals MIRM | 94.17 | -0.48% |

- Mirum Pharmaceuticals agreed to acquire Bluejay Therapeutics, adding a late stage hepatitis D candidate to its rare liver disease pipeline.

- The deal expands Mirum's portfolio beyond its existing bile acid products, including those acquired from Travere Therapeutics.

- The company aims to widen its reach in rare liver diseases by reducing reliance on a single product and broadening treatment options for patients.

Mirum Pharmaceuticals (NasdaqGM:MIRM), recently trading at about $98.23 per share, has seen strong multi year share price gains, with a very large 5 year return and a 321.6% 3 year return. The stock is also up 91.7% over the past year and 25.8% year to date, although it has seen a 4.6% decline over the past week. Against that backdrop, the Bluejay Therapeutics acquisition adds another late stage asset that sits squarely within Mirum's rare liver disease focus.

For investors following rare disease companies, the addition of a hepatitis D program alongside the Travere bile acid portfolio shows Mirum building out a broader platform rather than depending on a single therapy. How successfully Mirum integrates these assets, advances the hepatitis D candidate through late stage development and executes on commercial plans is likely to be key for the company’s longer term profile in rare liver disease treatments.

Stay updated on the most important news stories for Mirum Pharmaceuticals by adding it to your watchlist or portfolio . Alternatively, explore our Community to discover new perspectives on Mirum Pharmaceuticals.

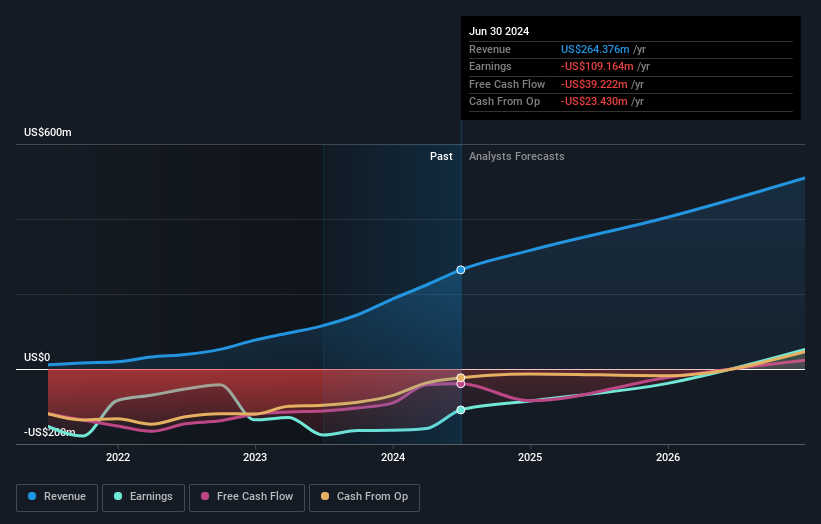

The Bluejay deal fits closely with how Mirum has been repositioning itself, from a company anchored on Livmarli to a broader rare liver disease platform. Adding brelovitug, a monoclonal antibody for chronic hepatitis delta virus already in a global Phase 3 trial, gives Mirum a late stage asset in a different part of the liver disease space to its bile acid programs from Travere. For you as an investor, that means the story is less about a single drug and more about whether Mirum can manage a multi asset portfolio, fund development and keep execution tight across several indications. The acquisition also lands alongside Mirum’s preliminary 2025 net product sales of about US$520m and a 2026 revenue outlook that points to up to 25% growth. This frames the move as an expansion from a company already operating at commercial scale rather than a pre revenue pipeline bet.

How This Fits Into The Mirum Pharmaceuticals Narrative

- The Bluejay acquisition supports the existing narrative that Mirum is trying to reduce reliance on Livmarli by adding late stage programs in rare liver diseases with meaningful patient need.

- It also raises the execution bar, since the narrative already highlights regulatory, reimbursement and competition risks, and brelovitug adds another pivotal readout and commercial launch to manage alongside PSC and other programs.

- The consensus narrative focuses heavily on bile acid based assets and near term PSC data, so the specific risk and opportunity profile for hepatitis D, including its different competitive set, may not yet be fully captured.

Narratives are an essential piece of the investing puzzle. Knowing when to buy, hold or sell is only possible through a deep understanding of the company's narrative and valuation. To know when to act for Mirum Pharmaceuticals, check out one of the company's most popular narratives in the Simply Wall St Community .

The Risks and Rewards Investors Should Connsider

- ⚠️ Analysts have flagged concentration risk around Livmarli, and adding more programs increases operational complexity that could pressure costs if launches or data are weaker than expected.

- ⚠️ Mirum remains exposed to broader rare disease sector issues such as pricing scrutiny and reimbursement uncertainty, which could affect newer assets like brelovitug as well as existing products.

- 🎁 The Bluejay acquisition supports Mirum’s aim to build a portfolio of rare disease therapies, which can diversify revenue sources if multiple indications reach approval and gain uptake.

- 🎁 The company already has commercial scale products and late stage trials in progress, so successful execution could create a more balanced rare liver disease business rather than a single product story.

What To Watch Going Forward

From here, the key items to watch are progress in the global Phase 3 trial for brelovitug in chronic hepatitis D, any integration updates on Bluejay’s team and technology, and how Mirum allocates capital across its growing set of late stage programs. You may also want to track whether Mirum’s revenue mix gradually shifts away from heavy dependence on Livmarli as newer indications and assets come through. Together with guidance updates and regulatory milestones, these signals will show whether the broader rare liver disease portfolio is translating into a more resilient business model.

To ensure you're always in the loop on how the latest news impacts the investment narrative for Mirum Pharmaceuticals, head to the community page for Mirum Pharmaceuticals to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.