Mirum Pharmaceuticals (MIRM) Is Up 15.5% After Positive FOP Phase 2 Data for Zilurgisertib

Mirum Pharmaceuticals MIRM | 0.00 |

- In June 2026, Mirum Pharmaceuticals and Incyte reported pivotal Phase 2 PROGRESS trial data showing that oral ALK2 inhibitor zilurgisertib reduced new heterotopic ossification lesions and was generally well tolerated in adolescents and adults with fibrodysplasia ossificans progressiva, following earlier FDA acceptance of its New Drug Application under Priority Review.

- The data, together with the FDA’s Priority Review and a September 26, 2026 PDUFA date, position zilurgisertib as a potentially meaningful addition to Mirum’s rare disease portfolio and a new source of diversification beyond its current bile acid-focused franchise.

- We’ll now explore how zilurgisertib’s Priority Review status and encouraging FOP efficacy profile could reshape Mirum’s rare-disease investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Mirum Pharmaceuticals Investment Narrative Recap

To own Mirum today, you need to believe its rare disease portfolio can broaden beyond Livmarli while the company manages high spend and a short cash runway. The new zilurgisertib data, together with FDA Priority Review and a September 26, 2026 PDUFA date, meaningfully elevates Mirum’s near term regulatory catalyst profile, but clinical and approval risk around this and its liver programs still looks like the core overhang.

Among recent announcements, the raised 2026 net product sales guidance to US$660 million to US$680 million stands out alongside the FOP update. Guidance still leans heavily on the existing bile acid drugs, so zilurgisertib’s progress is more about future diversification than changing this year’s revenue mix. If future approvals in PSC, HDV, or FOP underperform, Mirum’s ongoing R&D and commercialization spend could pressure margins and extend the path to sustained profitability.

Yet while the FOP data support a broader story, investors should also weigh how payer pressure and reimbursement risk could still limit Mirum’s upside...

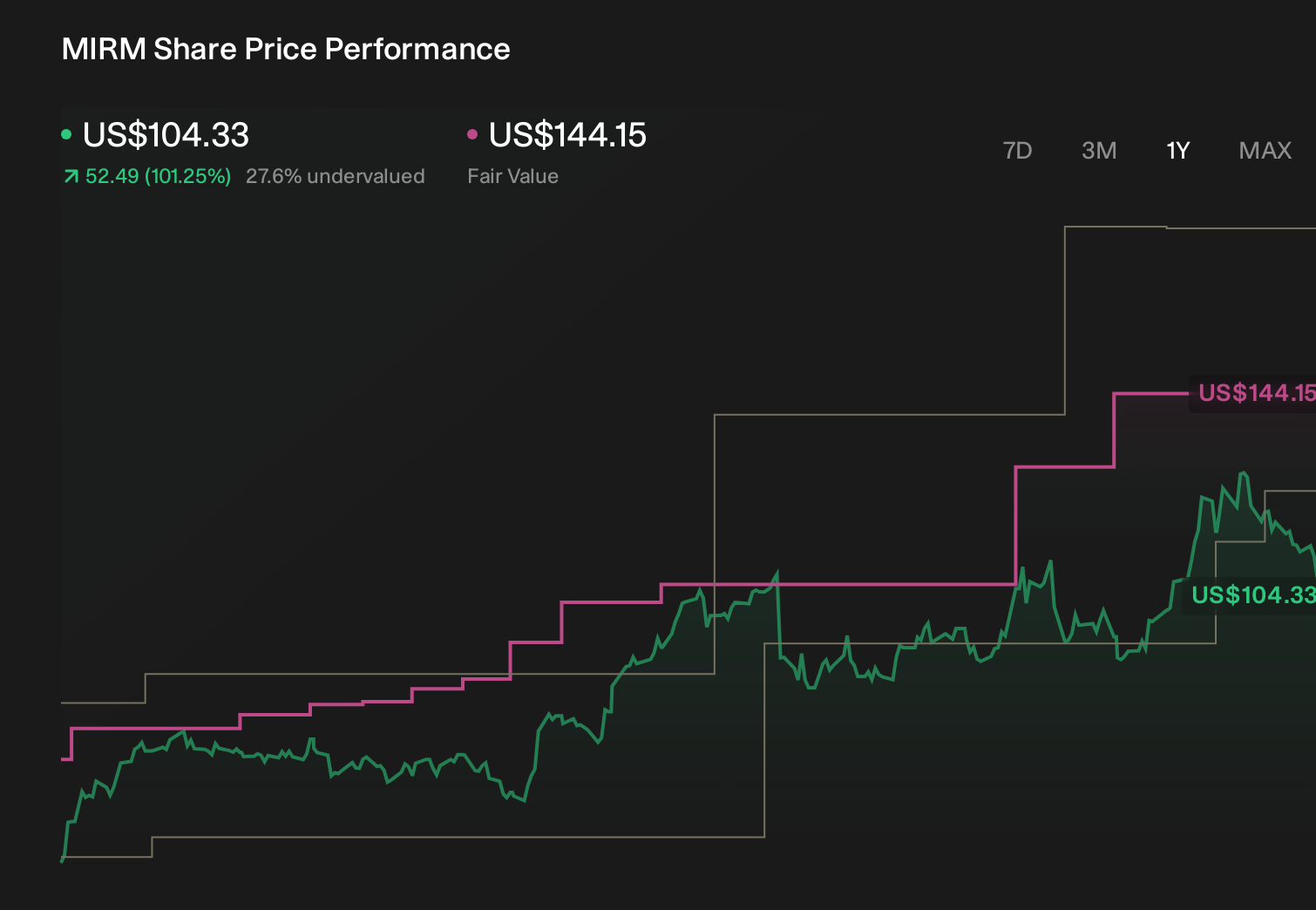

Mirum Pharmaceuticals' narrative projects $1.1 billion revenue and $234.1 million earnings by 2029. This requires 25.9% yearly revenue growth and about a $1.03 billion earnings increase from -$798.8 million today.

Uncover how Mirum Pharmaceuticals' forecasts yield a $144.15 fair value, a 16% upside to its current price.

Exploring Other Perspectives

The most bearish analysts already assumed revenue of about US$712.9 million and only US$23.3 million in earnings by 2028, so this FOP update may eventually challenge their tougher stance on regulatory and reimbursement risk.

Explore 3 other fair value estimates on Mirum Pharmaceuticals - why the stock might be worth over 3x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Mirum Pharmaceuticals research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Mirum Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Mirum Pharmaceuticals' overall financial health at a glance.

Searching For A Fresh Perspective?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 51 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.