Molina Healthcare (MOH) Q4 Loss And Margin Compression Challenge Bullish Earnings Narratives

Molina Healthcare, Inc. MOH | 139.38 | +2.62% |

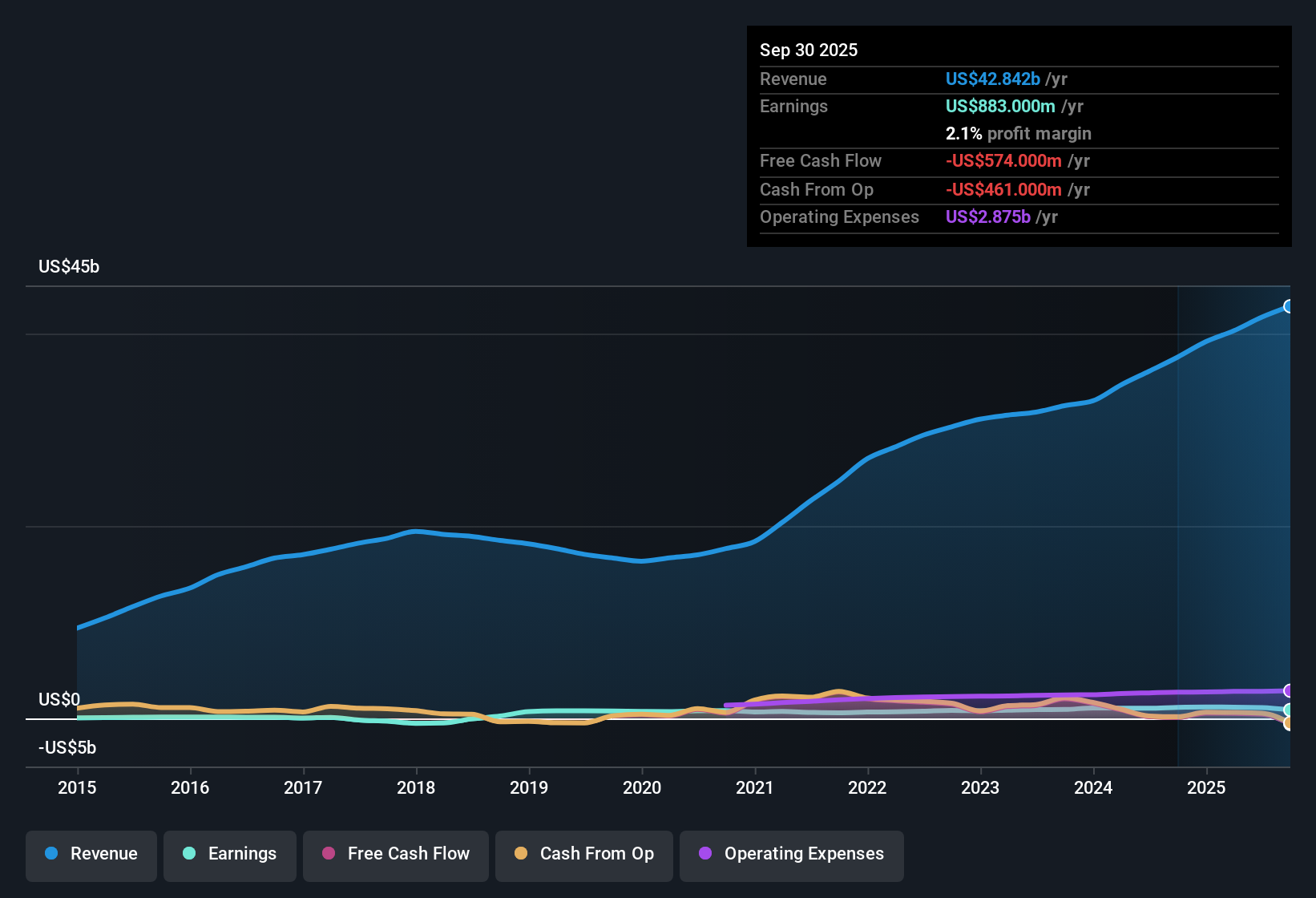

Molina Healthcare (MOH) has just wrapped up FY 2025 with Q4 revenue of US$10.8b and a basic EPS loss of US$3.15, following earlier quarterly EPS of US$5.46, US$4.76 and US$1.50, while trailing 12 month EPS sits at US$8.92 on revenue of US$43.6b. Over the past six reported quarters, revenue has moved from US$9.8b in Q3 2024 to above US$10b per quarter in 2025, as quarterly EPS ranged from US$4.44 and US$5.66 in late 2024 to a loss in Q4 2025. This sets up a mixed picture on profitability. With trailing net income of US$472m and a 1.1% net margin versus 3% a year earlier, investors are likely to focus closely on how sustainable the current margin profile looks from here.

See our full analysis for Molina Healthcare.With the latest results on the table, the next step is to see how these numbers line up with the widely followed narratives around Molina Healthcare’s growth, risks and long term earnings story, and where they may push investors to rethink their assumptions.

Margins Squeezed, With Q4 Loss Standing Out

- On a trailing 12 month view, Molina earned US$472 million on US$43.6b of revenue for a 1.1% net margin, compared with 3% a year earlier. Q4 2025 itself swung to a net loss of US$160 million after three earlier quarters of positive net income.

- Bears argue that rising medical costs and tighter government budgets could keep pressure on margins, and the shift from a 3% to 1.1% trailing margin aligns with that concern, although:

- Net income over the last year still totals US$472 million, which sits between the earlier US$1.18b trailing figure in late 2024 and the weaker latest run rate that Q4 implies.

- Consensus narrative points to rate adjustments and cost management efforts aimed at stabilising margins, which is not yet evident in the latest 1.1% net margin.

Revenue Near US$44b, But Profit Growth Lags

- Trailing revenue has moved from US$39.2b in Q4 2024 to US$43.6b in Q4 2025, while trailing net income over the same snapshots fell from about US$1.18b to US$472 million, so revenue growth has not translated into similar profit growth over this period.

- The bullish view expects Molina to benefit from contract wins and acquisitions, yet the current data show a different mix, because:

- Five year earnings growth of about 9.3% per year sits alongside the latest 12 month margin of 1.1%, which is lower than the prior year’s 3%, so recent profitability is weaker than that multi year growth rate suggests.

- Forecasts in the dataset call for earnings to grow about 21.4% per year while revenue is forecast at roughly 4.8% per year, which contrasts with the recent pattern where revenue expanded but trailing net income declined versus late 2024.

P/E At 13.4x With Large Gap To DCF Fair Value

- Molina trades on a P/E of 13.4x based on trailing earnings, compared with about 23.5x for the US Healthcare industry and 24.1x for peers. The dataset also shows a DCF fair value of US$810.45 against a current share price of US$122.65.

- Sceptics worry that weaker margins justify this lower multiple, yet parts of the bearish story are not fully echoed in the current numbers, because:

- While bears focus on the risk of long term margin compression, the company still reports trailing 12 month earnings of US$472 million and a history of around 9.3% annual earnings growth over five years, which is not consistent with a collapse in profitability.

- The roughly 13.4x P/E and the large gap between the share price and the US$810.45 DCF fair value in the dataset suggest the market is already pricing in some of the margin and policy risks described by the bearish narrative.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Molina Healthcare on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers another way? Take a couple of minutes to turn that view into your own Molina Healthcare narrative and share it with other investors: Do it your way.

A great starting point for your Molina Healthcare research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

Molina’s recent shift from a 3% to 1.1% net margin, capped by a Q4 loss, highlights that earnings quality is under pressure despite higher revenue.

If margin swings and earnings pressure have you second guessing concentration in one name, check out our 85 resilient stocks with low risk scores to find companies with steadier profiles that could help balance your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.