Moody's (MCO) Expands AI Tools, Is The Stock Fairly Valued?

Moody's Corporation MCO | 0.00 |

AI skills rollout puts Moody's (MCO) data at the center of client workflows

Moody's (MCO) has launched its first set of AI skills and expanded its Model Context Protocol integrations, with the goal of embedding its ratings, research, and risk data directly into how financial professionals run their day to day analysis.

Despite the AI skills rollout and fresh integrations with Microsoft 365 Copilot and Amazon Quick, Moody's share price is around $450, with mixed momentum. It has a 4.16% 90 day share price return but a year to date share price decline of 9.81%, and a 3 year total shareholder return of 32.63% that contrasts with a 7.02% decline over the past year.

If Moody's AI push has your attention, it could be a good moment to look across the sector and see which other companies are benefiting from similar themes through the 61 profitable AI stocks that aren't just burning cash

With Moody’s leaning into AI workflows and the stock around $450 after a year of share price weakness, the key question is simple: is this a genuine mispricing, or is the market already factoring in future growth?

Most Popular Narrative: 4.9% Undervalued

According to a widely followed Moody's narrative by user prajeesh, a fair value of $473.36 sits modestly above the last close around $450, which frames the stock as slightly undervalued rather than deeply mispriced.

Moody’s is not just a credit rating agency; it is one of the foundational infrastructure providers of the global financial system. Every year, governments, corporations, banks, and structured finance issuers collectively raise trillions of dollars in debt, and most of that debt requires a Moody’s rating to access institutional capital markets. This creates one of the strongest regulatory moats in modern capitalism. Alongside S&P Global, Moody’s effectively operates inside a global duopoly protected by decades of regulatory integration, reputation, and investor trust.

Curious what underpins that $473.36 fair value for Moody's? The narrative focuses on steady top line expansion, resilient margins, and a richer future earnings multiple than the market is currently implying.

Result: Fair Value of $473.36 (UNDERVALUED)

However, Moody's narrative could be challenged if bond issuance weakens again or if AI tools reduce the value that clients place on traditional credit ratings and analytics.

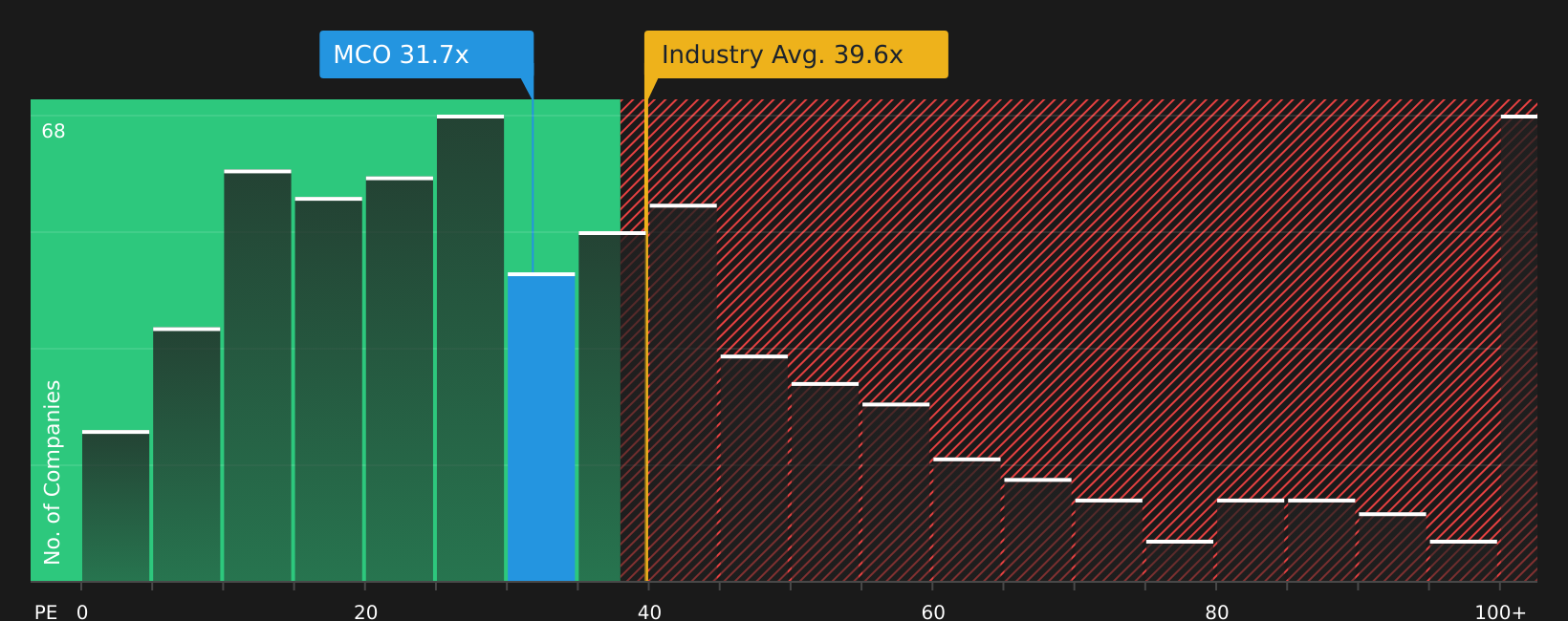

Another View: Moody's Looks Pricey On Earnings

That 4.9% “undervalued” fair value for Moody's sits awkwardly next to the current P/E of 31.5x, which is above the peer average of 21.3x and even above an estimated fair ratio of 17.7x. If the market leans back toward that lower fair ratio, how comfortable do you feel paying up today?

For a closer look at how this earnings based view compares to other valuation checks, including peers and the fair ratio, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If the mix of AI momentum and valuation debate around Moody's feels finely balanced, do not wait for consensus to form. Instead, weigh the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Moody's?

If Moody's has you thinking more broadly about opportunities, do not stop here. Widen your search with a few focused stock lists that match different investing goals.

- Target resilient cash flows and quality balance sheets by scanning companies in the solid balance sheet and fundamentals stocks screener (48 results).

- Hunt for potential mispricings using the 44 high quality undervalued stocks to spot stocks that combine fundamentals with room for re rating.

- Focus on resilience first and stress test your portfolio ideas against the 71 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.