Moody's (MCO) Valuation Check As AI Partnerships And New Analytics CEO Sharpen Growth Focus

Moody's Corporation MCO | 0.00 |

Moody's AI push comes into focus

Moody's (MCO) has moved quickly to expand AI-driven offerings, rolling out Moody's Agentic Solutions in AWS Marketplace and Anthropic's Claude environment, while naming Christina Kosmowski as CEO of Moody's Analytics.

These AI moves come after a period where momentum has cooled, with a 90 day share price return of 16.79% decline and a year to date share price return of 10.13% decline, even as 3 year and 5 year total shareholder returns of 51.82% and 43.83% remain positive.

If Moody's AI push has your attention, it could be a good moment to see what else is emerging in this space by scanning 38 AI infrastructure stocks

With Moody's shares down 16.79% over 90 days but still showing a 51.82% three-year total return, are you looking at an underappreciated AI and risk data business, or is the market already pricing in future gains?

Most Popular Narrative: 18.7% Undervalued

According to andre_santos, the most followed valuation narrative pegs Moody's fair value at $551.41, comfortably above the recent $448.42 close, and builds a detailed case around earnings power and capital returns.

📈 Moody's has established itself as one of the global standards in credit ratings, a status reflected in its wide economic moat and consequently stellar operating margins in the 45 to 50% range. The company consistently generates returns on invested capital roughly 5x its cost of capital, a strong signal of disciplined and effective capital allocation by management. Moody's also actively returns capital to shareholders through buybacks, steadily increasing ownership concentration. Its balance sheet is equally impressive, the interest coverage ratio is so robust that Moody's own estimated debt rating would sit at Aaa, comparing it to similar companies.

Want to see what underpins that wide moat call and higher fair value? The narrative leans heavily on margin resilience, cash flow compounding, and a specific long term earnings glide path that you may want to compare with your own expectations.

Result: Fair Value of $551.41 (UNDERVALUED)

However, this narrative can be challenged if trust in rating agencies weakens in key regions or if AI-driven tools compress pricing power across Moody's core products.

Another Angle on Moody's Valuation

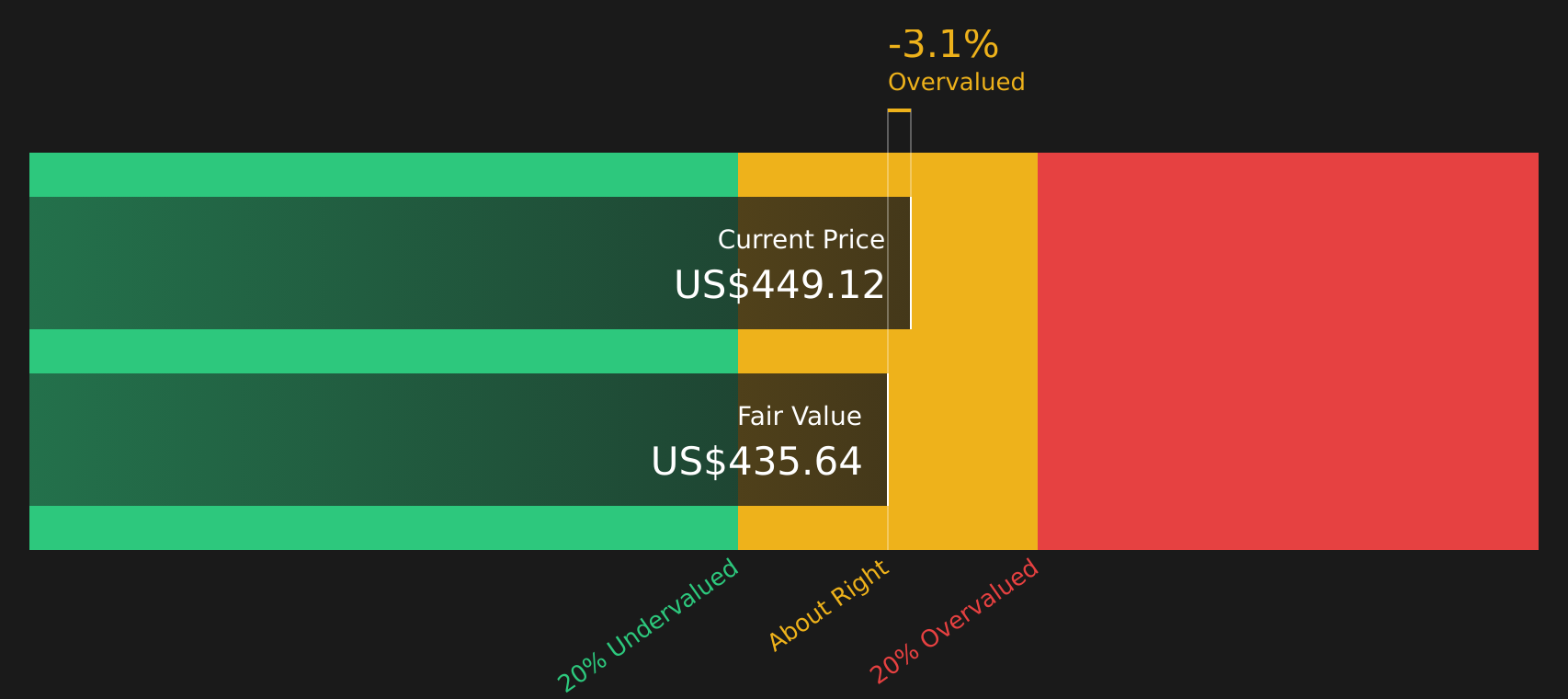

That 18.7% undervalued narrative stands in contrast to Simply Wall St's own SWS DCF model, which points to a fair value of $411.80, below the current $448.42 share price, and therefore suggests Moody's is trading on the expensive side. As an investor, which framework do you trust more for a business like this?

Next Steps

Mixed signals on value and AI potential often split opinions, so this is a good time to look through the numbers yourself and decide quickly whether the risk reward trade off lines up with your goals by weighing 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If Moody's has sharpened your focus, you can keep that momentum going by widening your watchlist with a few targeted screeners that surface fresh opportunities other investors may overlook.

- Spot potential bargains efficiently by scanning companies that currently screen as 58 high quality undervalued stocks and see which ones deserve a closer look.

- Prioritise resilience by reviewing 71 resilient stocks with low risk scores that may better match a steadier, capital preservation style.

- Stay early in the research process by checking a screener containing 23 high quality undiscovered gems that could align with your return goals before they attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.