MP Materials Deepens Pentagon Ties As U.S. Builds Critical Mineral Reserves

MP Materials Corp Class A MP | 49.73 | +2.73% |

- The U.S. Department of Defense commits a large, multi year investment to MP Materials (NYSE:MP) tied to rare earth processing and separation capacity.

- MP Materials enters a long term supply partnership with the Department of Defense to support domestic production of critical minerals.

- Federal initiatives to build domestic critical mineral reserves position MP Materials as a key potential supplier within the U.S. rare earth supply chain.

MP Materials operates one of the primary rare earth assets in the U.S., focused on materials used in electric vehicles, wind turbines, and defense applications. In a context of supply chain concerns and concentration of rare earth production in a few countries, U.S. policymakers are placing greater focus on domestic sourcing and processing capacity.

The new Department of Defense partnership and funding support could increase the visibility of MP Materials in government procurement and long term planning. For investors, the company now sits closer to the center of U.S. policy efforts around critical minerals, which may influence how its project pipeline and future contracting opportunities develop over time.

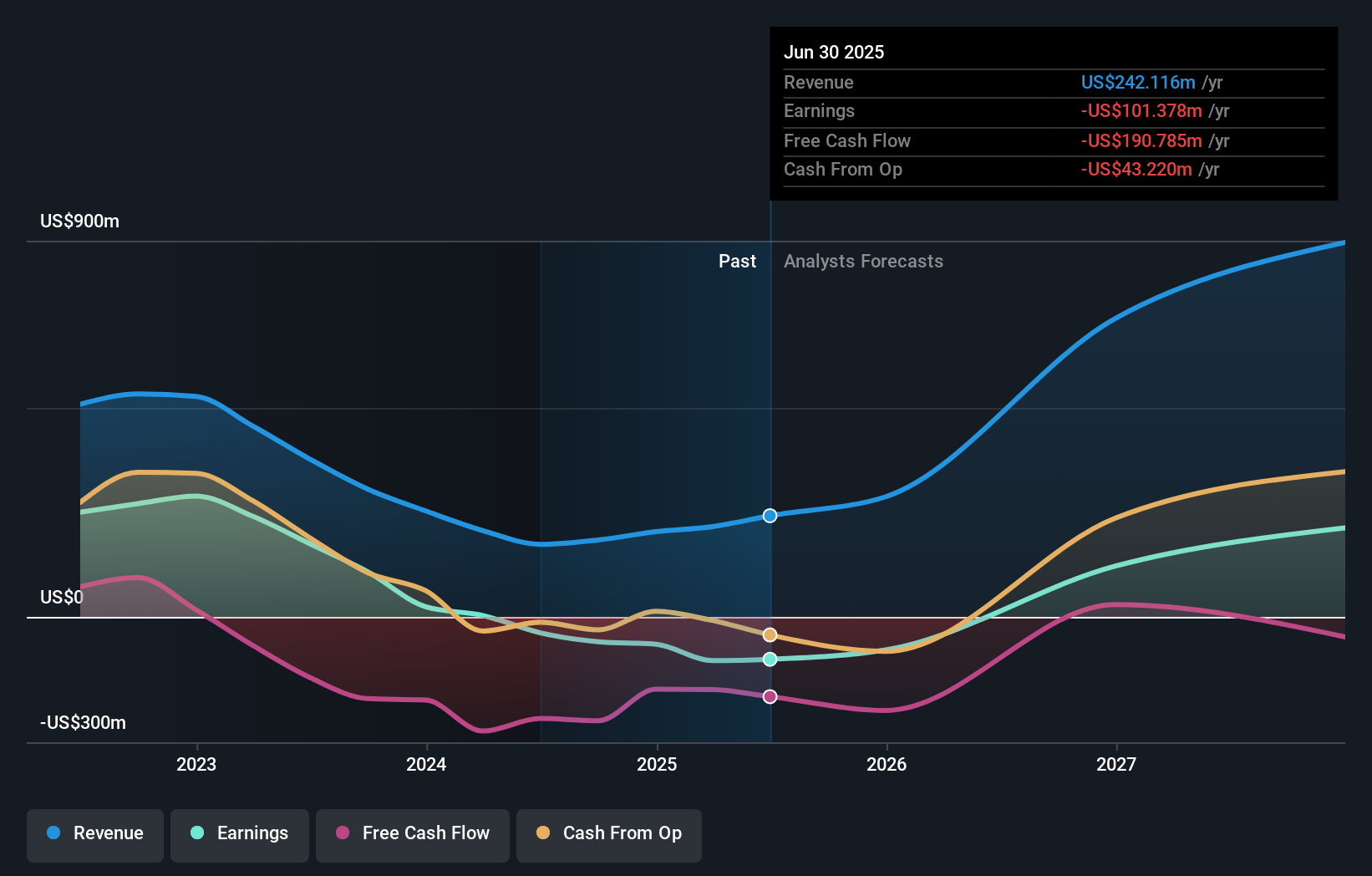

Stay updated on the most important news stories for MP Materials by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on MP Materials.

The Department of Defense’s multi year investment and long term offtake agreement effectively tie MP Materials into the heart of U.S. critical mineral policy. A 10 year commitment to buy 100% of magnets from MP’s second U.S. factory, alongside the company’s role in the planned Project Vault reserves, gives MP more visibility over future demand than many peers such as Lynas Rare Earths or Iluka Resources. For you as an investor, this news points to a business model that is moving from pure mining toward integrated processing and magnet production, with a larger share of value captured within the U.S. supply chain. At the same time, the partnership increases MP’s exposure to policy decisions, future appropriations, and execution on new facilities. How well MP hits milestones on its Mountain Pass expansions and new plants, and how it manages concentration in government and large tech customers, will be key in assessing how durable this position is compared with other rare earth and magnet producers like Neo Performance Materials.

How This Fits Into The MP Materials Narrative

- The DoD becoming a major shareholder and committing to long term magnet purchases lines up with the narrative’s focus on government backed contracts that can support more visible revenue from value added manufacturing.

- The heavy reliance on a single anchor customer heightens the concentration and policy risk already highlighted in the narrative, especially since the partnership includes contract restrictions and depends on continued congressional support.

- The emerging role in Project Vault and potential supply into national reserves is not fully reflected in the narrative, and may represent an additional source of long duration demand that sits alongside existing Apple and DoD agreements.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for MP Materials to help decide what it's worth to you.

The Risks and Rewards Investors Should Consider

- ⚠️ MP’s expansion into new U.S. processing and magnet facilities, including a second magnet plant targeting production by 2028, brings execution risk around timing, costs, and operational performance.

- ⚠️ The public private partnership makes MP more dependent on ongoing federal funding and policy support, and any shift in priorities or appropriations could affect the value of these long term agreements.

- 🎁 Long duration offtake contracts with the DoD and large customers can provide greater earnings visibility than many peers that rely on spot rare earth prices.

- 🎁 Potential participation in a US$12b critical minerals reserve through Project Vault could create an additional demand source for MP’s products beyond commercial EV and electronics markets.

What To Watch Going Forward

From here, it is worth watching three things. First, the detailed terms and milestones on the DoD partnership, including how price floors and volumes are structured over the 10 year period. Second, progress updates on MP’s integrated production plans, especially the ramp of its second U.S. magnet plant and any new heavy rare earth capacity at Mountain Pass. Third, how the company is referenced in future Project Vault announcements and federal procurement plans, which will help you gauge how central MP is to the broader U.S. rare earth supply chain compared with other suppliers. Upcoming Q4 2025 results and the strategic update on February 26 should give more color on these points.

To ensure you're always in the loop on how the latest news impacts the investment narrative for MP Materials, head to the community page for MP Materials to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.