MP Materials (MP) Stock Could Be 18.6% Overvalued as Magnet Narrative Meets DCF Upside

MP Materials MP | 0.00 |

MP Materials (MP) has drawn fresh attention after recent share price swings, leaving investors weighing its rare earth exposure against mixed momentum, including a decline of about 6% over the past month.

At a share price of $60.29, MP Materials has seen short term share price momentum cool slightly, with a 1 month share price return down 6.47%. However, a 90 day share price return of 13.14% and a 1 year total shareholder return of 64.91% point to stronger performance over a longer period.

If the recent rare earth moves have caught your attention, it could be worth scanning a wider set of peers using the 30 best rare earth metal stocks

MP Materials combines rare earth production, magnet manufacturing and strong recent shareholder returns, but also reports a net loss and trades below some valuation estimates. Is this a genuine opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 18.6% Overvalued

The most followed narrative on MP Materials puts fair value at $50.85, below the last close of $60.29, and frames the company as a future magnet manufacturer rather than just a miner.

MP Materials represents the highest conviction idea in the sector for 2026. The market is currently pricing MP as a mining company, ignoring its imminent transformation into a high-margin industrial manufacturer. The "10X Facility" partnership with the Department of Defense (DoD) 48 fundamentally de-risks the downside while providing explosive upside.

Interested in how this narrative gets to its valuation call on MP Materials? It leans heavily on rapid revenue expansion, margin lift from vertical integration, and a richer future earnings multiple tied to magnet manufacturing.

Result: Fair Value of $50.85 (OVERVALUED)

However, MP Materials still faces execution risk on its magnet ramp and HREE plans, and any weaker pricing or contract changes could quickly challenge this bullish narrative.

Another View: SWS DCF Points To Upside

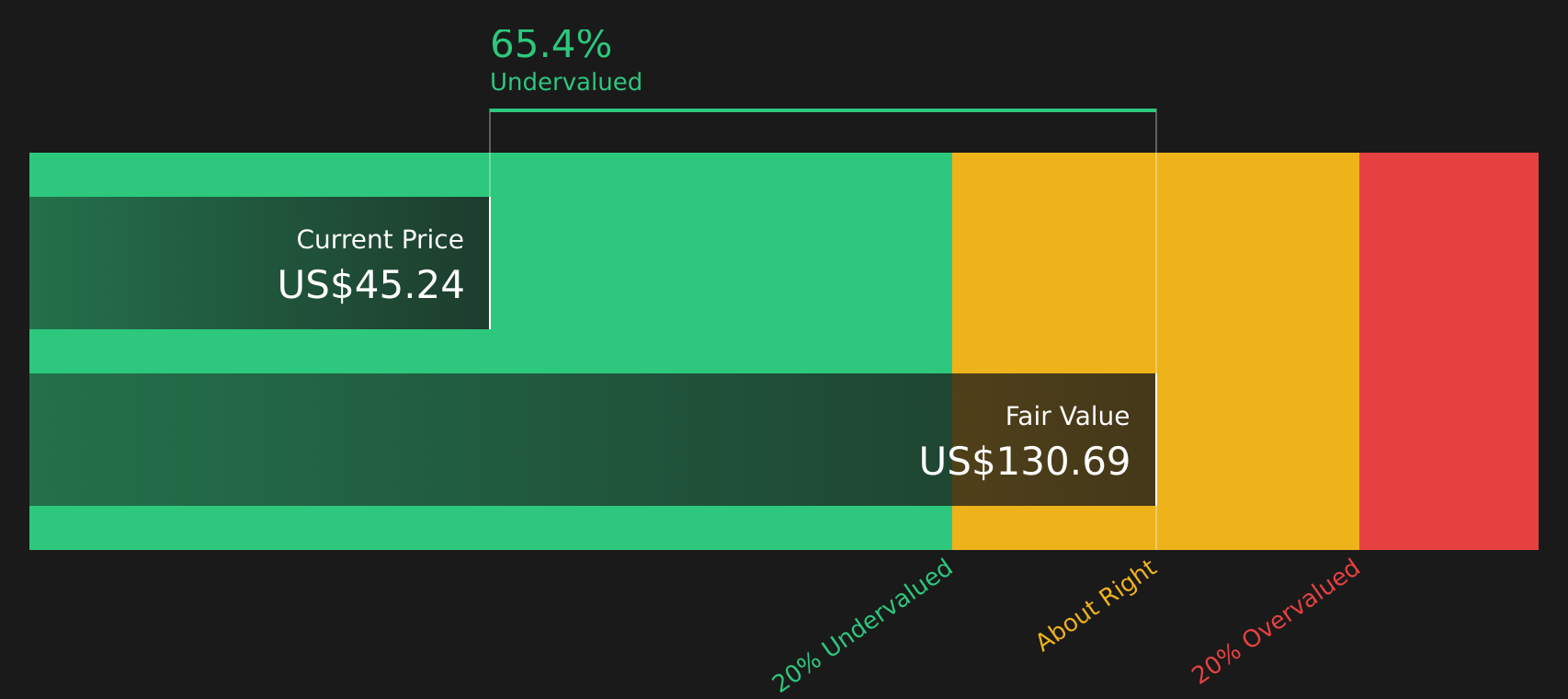

While the most popular community narrative pegs MP Materials as about 18.6% overvalued at a fair value of $50.85, the SWS DCF model reaches a very different conclusion. It provides an estimate of $115.15 per share, which is 47.6% above the current $60.29 price. So which story do you trust more: the crowd narrative or the cash flow math?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out MP Materials for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals on MP Materials so far, right? Take a closer look at the numbers, weigh the opposing arguments and check out the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond MP Materials?

If MP Materials has sharpened your focus on opportunities, do not stop here. Broaden your watchlist with other focused ideas that could suit your approach.

- Target potential mispricing by scanning companies that combine quality fundamentals with attractive valuations using the 44 high quality undervalued stocks.

- Strengthen your income focus by reviewing businesses with higher yields and resilient payouts through the 7 dividend fortresses.

- Prioritise resilience and capital preservation by filtering companies with historically lower risk profiles via the 66 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.