MP Materials (MP) Sues USA Rare Earth, Is The Stock Still Cheap?

MP Materials MP | 0.00 |

MP Materials (MP) has drawn investor attention after suing USA Rare Earth for alleged theft of proprietary magnet technology and recruitment of key engineers, raising fresh questions about talent, intellectual property, and future operations.

MP Materials' share price has softened in recent months, with the 90 day share price return down 5.49%, even as the 1 year total shareholder return of 15.74% and 3 year total shareholder return of 111.98% point to earlier, much stronger momentum.

If this legal dispute has you thinking more broadly about rare earth exposure, it could be a good time to scan the wider sector using the 30 best rare earth metal stocks.

MP Materials now trades at a steep discount to both analyst targets and an estimate of intrinsic value, yet the stock has cooled after the lawsuit headlines. Is the market rightly cautious, or is it overlooking the longer term story?

Most Popular Narrative: 35.1% Undervalued

Against MP Materials' last close of $52.21, the most followed narrative pegs fair value near $80, creating a wide gap that hinges on aggressive growth and margin assumptions.

The company is expanding its vertically integrated processing and magnet manufacturing capacity with the "10X" plant and a modular recycling facility. Together with significant CapEx support from Apple and the DoD, this is expected to capture more value added margins and potentially improve net profit and operating leverage as they ramp downstream operations.

Want to see what kind of revenue curve and profit swing this assumes for MP Materials? Short timelines, rising margins, and a rich future earnings multiple sit at the core of this valuation story.

Result: Fair Value of $80.44 (UNDERVALUED)

However, this MP Materials story can quickly look different if customer concentration becomes a problem or if the major government and Apple projects encounter delays or cost overruns.

Another View on MP Materials' Valuation

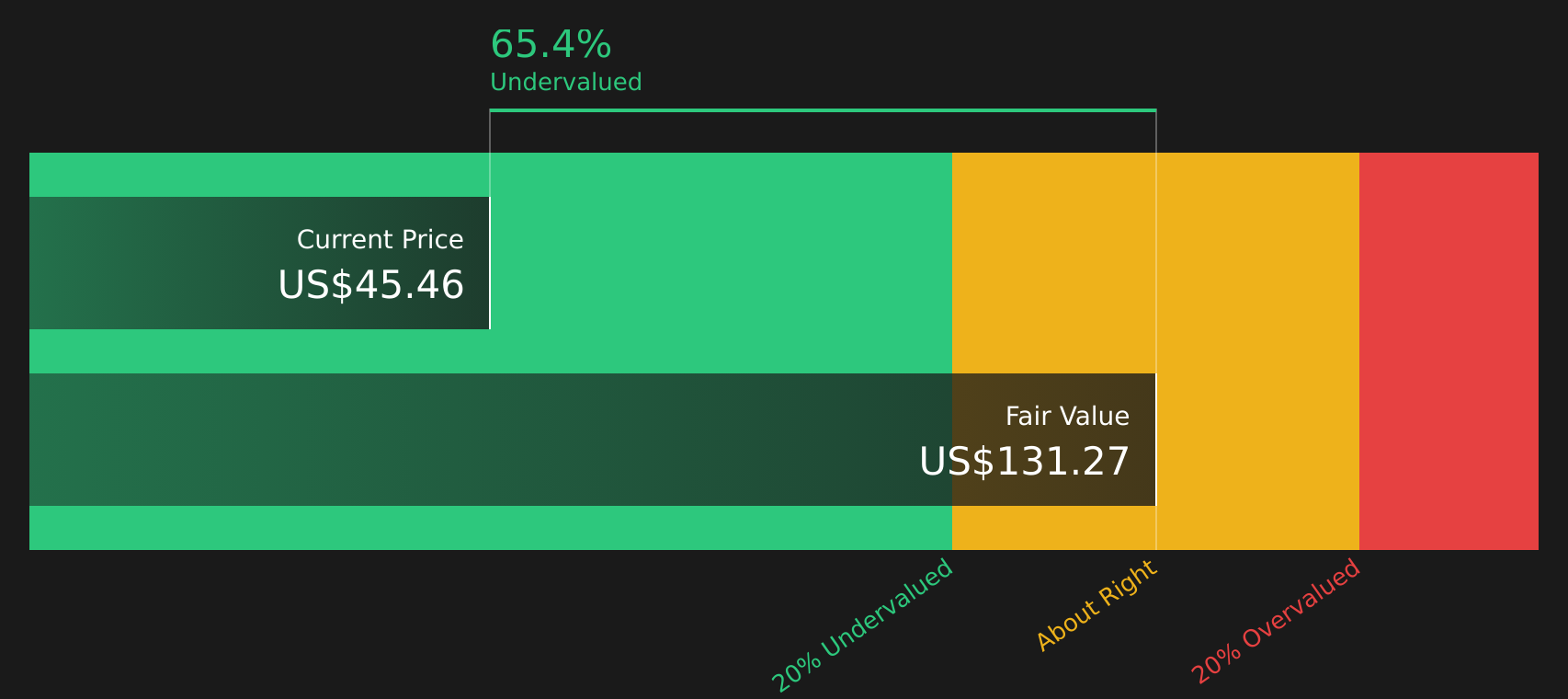

The popular MP Materials narrative leans heavily on discounted cash flows, with the SWS DCF model suggesting the stock trades about 60.5% below an estimated fair value of $132.02. That is a large gap to current pricing. The key question is whether those long term cash flow assumptions feel realistic for you.

Next Steps

If the mixed sentiment around MP Materials has you on the fence, consider using the full data set to clarify your view and make a more confident decision by weighing the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond MP Materials?

Before you move on from MP Materials, give yourself a wider field of options by scanning other stocks that match clear, objective criteria using the Simply Wall St Screener.

- Target income potential with companies that aim to combine higher yields and resilience by checking out 9 dividend fortresses.

- Zero in on quality at a reduced price by reviewing companies highlighted in the 44 high quality undervalued stocks.

- Prioritize resilience over excitement by focusing on companies featured in the 76 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.