Myriad Genetics (MYGN) Losses Deepen 21.1% Annually, Value Appeal Tested Heading Into Earnings

Myriad Genetics, Inc. MYGN | 4.50 4.50 | +3.21% 0.00% Pre |

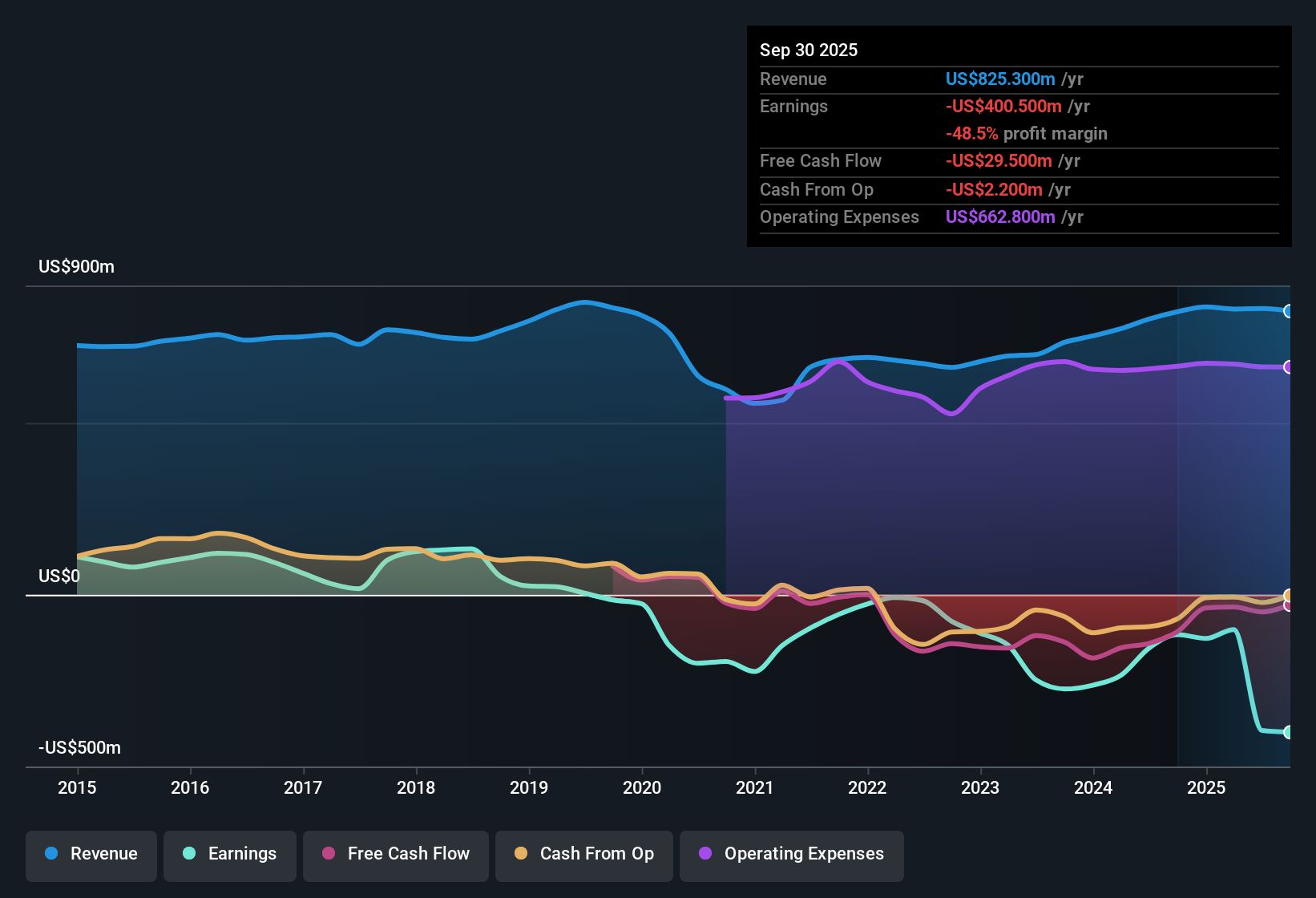

Myriad Genetics (MYGN) continues to face headwinds, with losses mounting at an average rate of 21.1% per year over the past five years and no meaningful progress toward profitability on the horizon. Revenue forecasts remain muted at an expected 4.5% annual growth, trailing the broader US market's 10.5% pace. For investors, the story centers on persistent unprofitability balanced by compelling value metrics, as the company's Price-To-Sales ratio of 0.7x looks attractive relative to sector peers, and the share price remains below its estimated fair value of $10.15.

See our full analysis for Myriad Genetics.The next section puts these headline figures in context, testing how they align or clash with the bigger narratives that drive investor sentiment around Myriad Genetics.

Margins Stay Deep in the Red

- Net profit margin remains negative and has not improved, staying well below the US Biotechs industry's average profit margin of 16.1%.

- The analysts' consensus view emphasizes that despite operational improvements and strategic partnerships, Myriad Genetics is expected to remain unprofitable for at least the next three years.

- This persistent unprofitability stands in contrast to strategic R&D investments and efforts to expand the test portfolio. Consensus expects these initiatives will eventually drive gross and net margin expansion, yet no turnaround is projected through 2026.

- Consensus points to high debt costs and continued reliance on mature products as underlying reasons profit margins are stalled. Long-term forecasts assume industry-like margins are a requirement for upside.

- To see how the ongoing margin struggle shapes the overall outlook, analysts urge checking the full consensus narrative for a balanced perspective. 📊 Read the full Myriad Genetics Consensus Narrative.

Analyst Target Signals Little Upside

- The current share price is $6.46, just 7.8% below the $8.29 analyst price target, highlighting muted near-term upside expectations from Wall Street.

- Consensus narrative notes that this tight gap suggests analysts widely believe Myriad Genetics is fairly valued today.

- Consensus expects that even if revenues reach $963.8 million and profit margins climb to the industry average by 2028, the implied P/E multiple of 5.8x would still lag sector norms. This helps explain the tepid price target.

- This perspective suggests that substantial operational improvement, not just growth, is necessary to support a higher target or a re-rating of the stock.

Valuation Cases Hinge on Deep Discount

- Myriad Genetics trades at a Price-To-Sales ratio of 0.7x, dramatically below the peer average of 9.1x and industry average of 10.8x. The current share price of $6.46 represents a significant discount to the DCF fair value of $10.15.

- Consensus narrative underscores that this discount frames Myriad as a value opportunity balanced by ongoing business risk.

- Analysts highlight the low valuation as providing a cushion against further downside, especially if efforts to grow new test volumes or win payer reimbursement accelerate revenue more than currently projected.

- However, the persistent lack of profitability and dependence on mature franchises keep risk high. Consensus considers the value case attractive only for investors who are willing to wait for improvements to play out.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Myriad Genetics on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have a different take on the data? It only takes a few minutes to shape your perspective and share your own narrative. Do it your way.

A great starting point for your Myriad Genetics research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

Myriad Genetics continues to struggle with persistent unprofitability, weak margins, and a heavy reliance on mature products, factors that hamper its earnings outlook.

If you’re looking for more consistent growth and robust results, compare your options using stable growth stocks screener (2077 results) for companies showing proven, reliable expansion year after year.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.