Nasdaq (NDAQ) Stock Could Be 8% Overvalued Despite Record Listing Growth

Nasdaq, Inc. NDAQ | 0.00 |

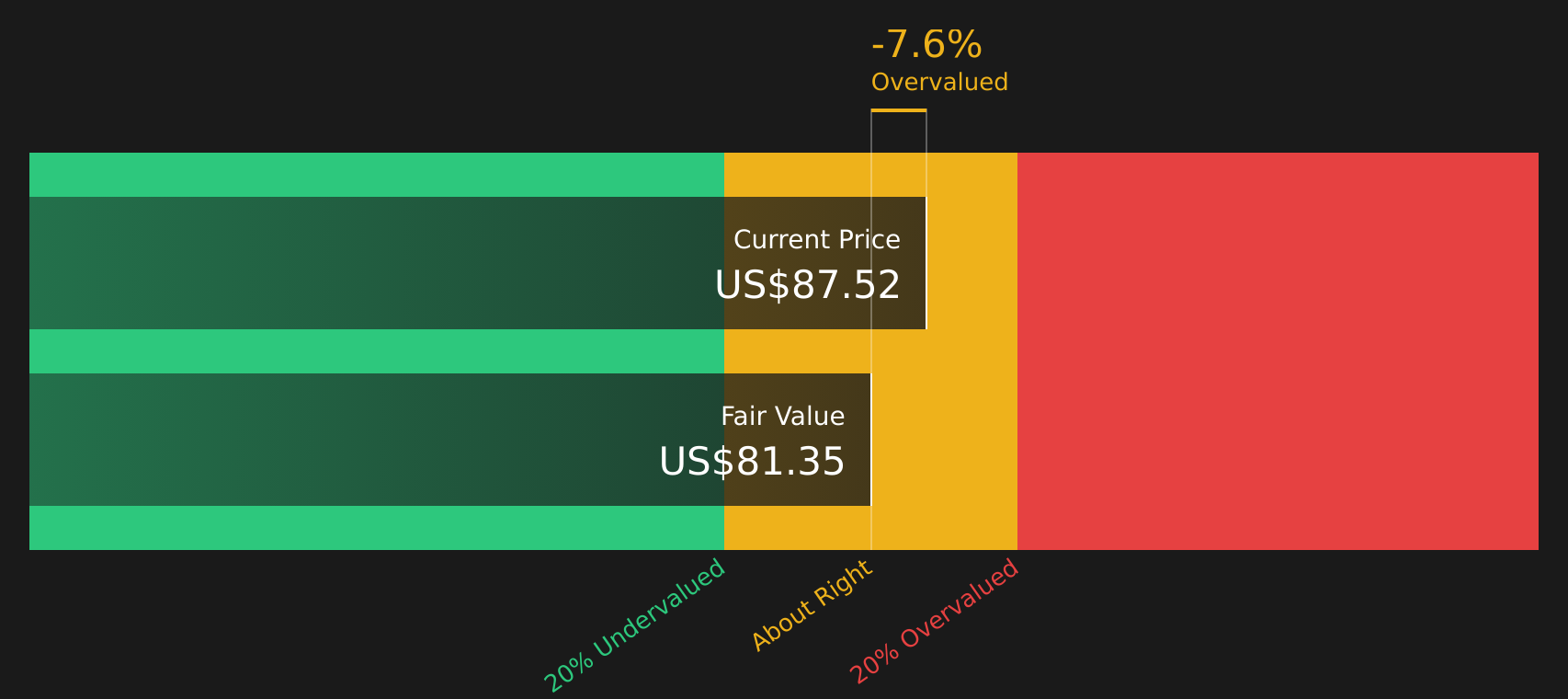

Nasdaq stock is coming off a strong 3 year run, yet its current checks suggest investors are paying close to what the intrinsic value estimate implies while traditional earnings multiples point to a richer price tag. With the shares last closing at US$84.39 and recent analyst sentiment upbeat, the question is how much of that optimism is already reflected in the valuation.

- Nasdaq has returned 75.9% over the past 3 years, which sets a high bar for any further gains to be supported by fundamentals.

- Record listing activity and a new US$1.5b revolving credit facility can support growth plans, while decisions around acquisitions and capital returns may still influence how investors view the stock's risk and reward profile.

- Nasdaq scores 3 of 6 on our valuation checks, a mixed picture rather than a clear bargain or clear overvaluation, which you can see in more detail on our 3 assessment.

The issue now is whether Nasdaq's current price offers enough potential upside relative to its intrinsic value estimate and richer earnings multiples to appeal to investors at this stage.

Is Nasdaq Fairly Priced on Excess Returns?

The Excess Returns model values Nasdaq by comparing the return it is expected to earn on its equity base with the return investors require. For Nasdaq, the inputs suggest solid profitability, with an average Return on Equity of 19.35% applied to a Book Value of $21.31 per share and a Stable EPS estimate of $4.44 per share, against a Cost of Equity of $1.87 per share. That gap produces an Excess Return of $2.56 per share and a Stable Book Value projection of $22.94 per share.

Putting these pieces together, the model arrives at an intrinsic value of $78.30 per share, which sits below the recent share price of $84.39. On this basis, the stock screens about 7.8% overvalued. Nasdaq’s recently secured $1.5 billion revolving credit facility, which provides flexibility for acquisitions and buybacks, may help explain why the market is currently placing a premium over what the Excess Returns math supports.

Overall, the Excess Returns model points to Nasdaq stock being roughly fairly valued, but leaning slightly overvalued at current levels.

Nasdaq is fairly valued according to our Excess Returns, but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Has Nasdaq Run Too Far on Earnings?

The P/E ratio works well for Nasdaq because earnings are a key focus for investors in established market infrastructure companies. On this measure, Nasdaq trades on a P/E of about 25.0x, which sits below the wider Capital Markets industry average of 40.4x and also below the peer group average of 34.9x.

However, the tailored fair P/E ratio for Nasdaq is 17.0x. This reflects what investors might typically pay given its earnings profile, margins, size and risk. Against that benchmark, the current P/E implies a clear premium, suggesting the market is assigning a higher price to each dollar of earnings than this framework supports.

Overall, Nasdaq appears overvalued on its P/E ratio, with the share price implying a richer earnings multiple than the fair benchmark suggests.

The Nasdaq Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Nasdaq pick up where the valuation puzzle leaves off by spelling out which assumptions about Nasdaq's future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today's price on the Community page. Each Narrative treats fair value as a thesis about the business that can be tracked over time, rather than just a single snapshot of what the stock might be worth today.

Be one of the first voices in the Simply Wall St community to set out a clear, number driven narrative on Nasdaq, weighing in on whether moves like the new US$1.5b revolving credit facility and record listing activity really support today's share price.

Share a thesis you can track over time as new results and developments land, and see how your view on Nasdaq's growth, margins and execution compares with what actually plays out.

Do you think there's more to the story for Nasdaq? Head over to our Community to see what others are saying!

The Bottom Line

Putting it together, Nasdaq looks close to its intrinsic value estimate from the Excess Returns model, while trading on an earnings multiple that screens as overvalued against its tailored fair P/E. The mixed valuation score underlines that this is not a clear bargain, but also not an obviously stretched story on every metric. From here, the key question is whether Nasdaq can deliver the growth and execution that keep investors comfortable paying a premium multiple on earnings, relative to what the intrinsic value math supports.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.