Navigator Holdings (NVGS) Could Be 16% Undervalued As It Sells $183 Million Of Assets

Navigator Holdings Ltd. NVGS | 0.00 |

Navigator Holdings (NVGS) has agreed to sell eight liquefied gas carriers and its stake in the Unigas International joint venture for about US$183 million, reshaping its fleet and capital allocation priorities.

Navigator Holdings’ latest vessel sale comes after a mixed few months in the market, with a 1 month share price return of 6.33% decline contrasting with a 22.77% year to date share price gain and a 5 year total shareholder return of 127.89%. Taken together, these figures suggest longer term momentum has been stronger than the recent pullback.

If this fleet reshaping has you thinking about where else capital could work hard, it may be worth checking a curated screener of 34 power grid technology and infrastructure stocks as another way to uncover potential opportunities tied to global infrastructure investment.

Bulls see Navigator Holdings using this US$183 million reshuffle to concentrate on higher value tonnage, while bears focus on recent earnings pressure and valuation risk. Which side do the numbers support as you weigh today’s price?

Most Popular Narrative: 15.6% Undervalued

At a last close of $21.30 versus a narrative fair value of $25.25, Navigator Holdings is framed as undervalued, with that gap supported by detailed earnings and cash flow assumptions.

The continued structural shift toward cleaner fuels (like LPG and ammonia), together with industrial growth and higher living standards in emerging markets, is driving rising demand for liquefied gas and petrochemical transport. Navigator is already seeing restored trade volumes post-Q2 disruption, supporting higher utilization and revenue growth.

Read the complete narrative. Read the complete narrative.

Curious what justifies a higher value for Navigator Holdings even as forecasts point to lower revenue, slimmer margins, and a richer future earnings multiple than the sector? The narrative leans on specific long term contracts, volume expectations, and a particular discount rate to bridge that gap between today’s earnings path and tomorrow’s price tag.

Result: Fair Value of $25.25 (UNDERVALUED)

However, investors still need to weigh the risk that higher vessel operating costs and regulatory driven fleet upgrades could squeeze margins and weaken the Navigator Holdings thesis.

Another View on Navigator Holdings’ Valuation

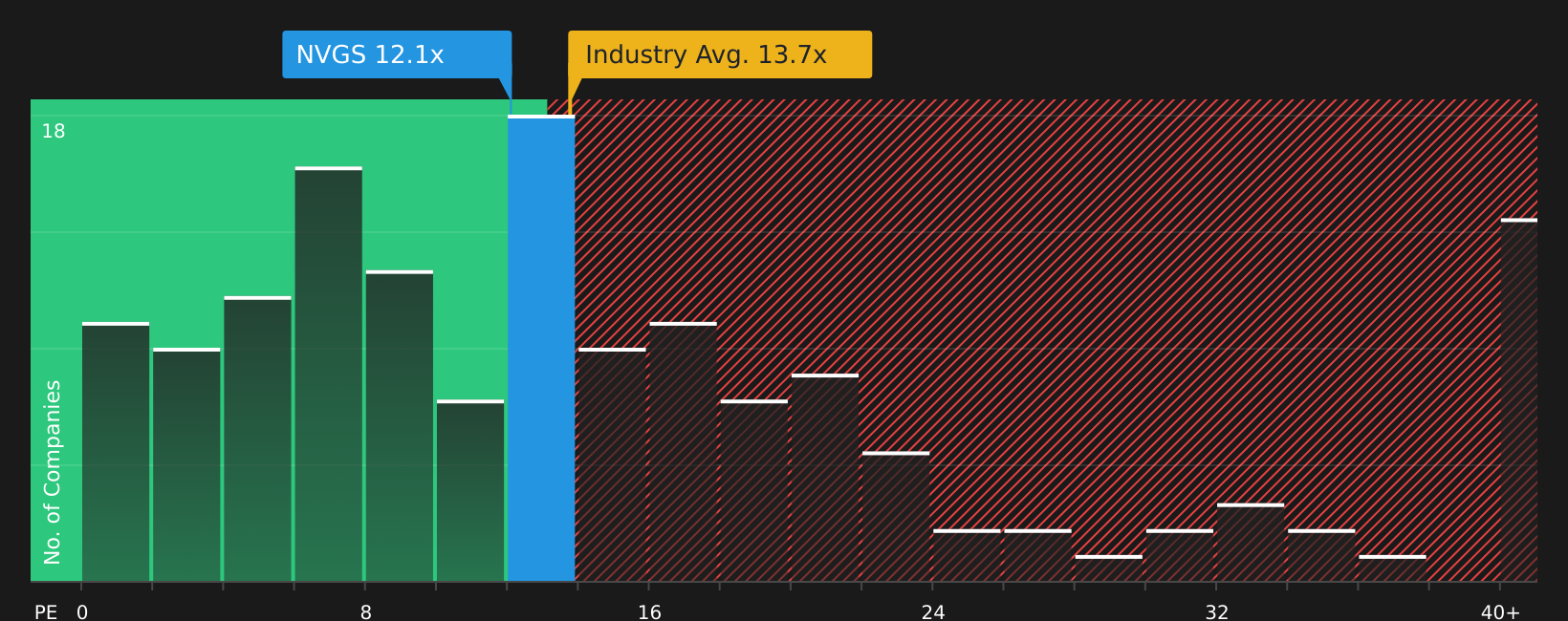

While the narrative fair value suggests Navigator Holdings is undervalued, the P/E picture is more complicated. The stock trades on a 12.1x P/E, well below the peer average of 22.4x, yet above a fair ratio of 7.8x that the market could move toward. That mix of “cheap versus peers” and “rich versus fair ratio” raises a real question about whether investors are being paid enough for the risk.

For a closer look at how these P/E gaps compare with peers and the fair ratio in practice, it is worth checking the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With both risks and rewards in play for Navigator Holdings, it makes sense to move quickly, review the underlying data yourself, and weigh the 2 key rewards and 4 important warning signs.

Looking for more investment ideas beyond Navigator Holdings?

If Navigator Holdings has your attention, do not stop there. Broaden your watchlist with other focused ideas that match your goals and keep new opportunities on your radar.

- Target potential mispricing by scanning a hand picked set of 47 high quality undervalued stocks that pair earnings quality with balance sheet strength.

- Build a steadier income stream by reviewing 10 dividend fortresses that combine higher yields with thorough fundamental checks.

- Dial back risk without giving up on growth by checking 78 resilient stocks with low risk scores that score well on resilience and financial health.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.