NCR Atleos (NATL) Teams With Sesami As Its Undervalued Narrative Stays In Focus

NCR Atleos Corporation NATL | 0.00 |

NCR Atleos (NATL) is drawing fresh investor attention after announcing a new collaboration with Sesami to resell and support CM-Series Intelligent Teller Cash Recycler solutions for banks and credit unions across the United States.

Even with the Sesami tie-up and recent agreements with credit unions and banks, NCR Atleos' share price has moved more gently, with a year-to-date share price return of 17.06% and a 1-year total shareholder return of 49.35%. This suggests earlier gains and momentum that has cooled in recent weeks, with a last close of $43.58.

If this kind of fintech partnership has your attention, it could be a good moment to see what else is emerging in the sector through the 61 profitable AI stocks that aren't just burning cash.

With NCR Atleos posting solid revenue and profit growth, a value score of 1, and a P/E of 19.22 that sits below its recent high, the key question is whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 13.3% Undervalued

At a last close of $43.58, the most followed narrative around NCR Atleos points to a fair value of about $50.27, framing the stock as modestly undervalued on those assumptions.

High recurring revenue mix (over 70% in Q2), significant productivity gains through AI-driven service optimization, and a rapidly scaling backlog are driving strong margin expansion and robust free cash flow, underpinning announced share buybacks and sustained EPS growth, suggesting current valuation does not reflect enhanced long-term earnings power.

Want to see what underpins that confidence in NCR Atleos? The narrative leans heavily on recurring revenue, ambitious earnings growth and a compressed future earnings multiple that many investors might not expect.

Result: Fair Value of $50.27 (UNDERVALUED)

However, the NCR Atleos story could shift if cash usage fades faster than expected, or if digital banking and fintech competition erode long term ATM demand.

Another View on NCR Atleos Valuation

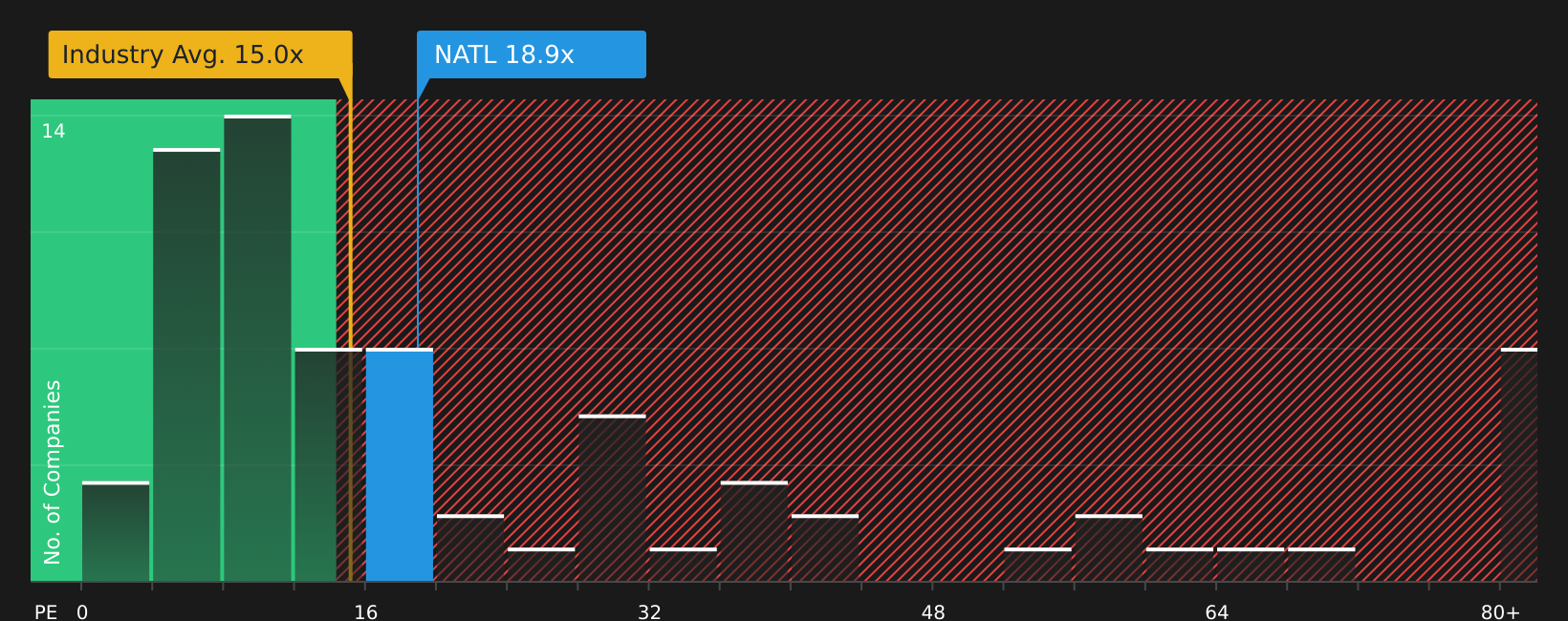

The popular narrative frames NCR Atleos as about 13.3% undervalued against a fair value of $50.27, yet the picture looks different when you focus on earnings. The current P/E of 18.9x is higher than both peers at 8x and the US Diversified Financial industry at 14.6x, even though it sits slightly below the fair ratio of 19.8x. This suggests there may be limited room for error if earnings or sentiment slip.

For a closer look at how this earnings based view stacks up against other lenses on NCR Atleos, take a moment with the See what the numbers say about this price — find out in our valuation breakdown..

Next Steps

Conflicted by the mix of optimism and caution around NCR Atleos? Take the opportunity to act while sentiment is still forming and weigh both sides by checking the 2 key rewards and 2 important warning signs.

Looking for more investment ideas beyond NCR Atleos?

If NCR Atleos has sharpened your appetite for opportunities, do not stop here. Broaden your watchlist with focused stock ideas built from clear financial filters.

- Hunt for quality at a discount by scanning companies that screen as 44 high quality undervalued stocks.

- Strengthen the foundation of your portfolio by reviewing stocks in the solid balance sheet and fundamentals stocks screener (48 results).

- Get ahead of the crowd by checking the screener containing 19 high quality undiscovered gems before attention fully shifts their way.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.