New Navy Contract And Manufacturing Overhaul Could Be A Game Changer For CACI International (CACI)

CACI International Inc Class A CACI | 0.00 |

- Earlier in May 2026, CACI International secured a US$113.8 million U.S. Navy contract supporting Military Sealift Command integrated business systems, and previously named former L3Harris executive Christopher Monoski as Executive Vice President, Manufacturing to centralize advanced defense technology production.

- Together, the long-duration Navy work and new manufacturing leadership underscore CACI’s push into more complex, hardware-enabled national security programs that require scaled, high-reliability execution.

- With this new Navy contract extending CACI's role in Military Sealift Command systems, we'll assess how it reshapes the investment narrative.

Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

CACI International Investment Narrative Recap

To own CACI International, you need to be comfortable with a contractor that leans heavily on U.S. national security budgets and wins by executing complex, tech-heavy programs at scale. The new US$113.8 million Navy award reinforces that thesis and modestly supports the near term revenue and backlog catalyst, while the key risk remains execution and supply chain reliability as CACI leans further into hardware enabled offerings that must be delivered on time and at high quality.

Among recent developments, the appointment of former L3Harris operations leader Christopher Monoski as Executive Vice President, Manufacturing looks especially relevant here, because it directly touches CACI’s ability to scale production for advanced RF, photonics, and space systems. For investors watching contract momentum and margin resilience as primary catalysts, this combination of Navy work and centralized manufacturing oversight provides a clearer line of sight on how CACI is trying to manage execution risk in volume defense tech programs.

Yet beneath the contract wins, investors still need to watch how persistent manufacturing and supply chain pressures could impact...

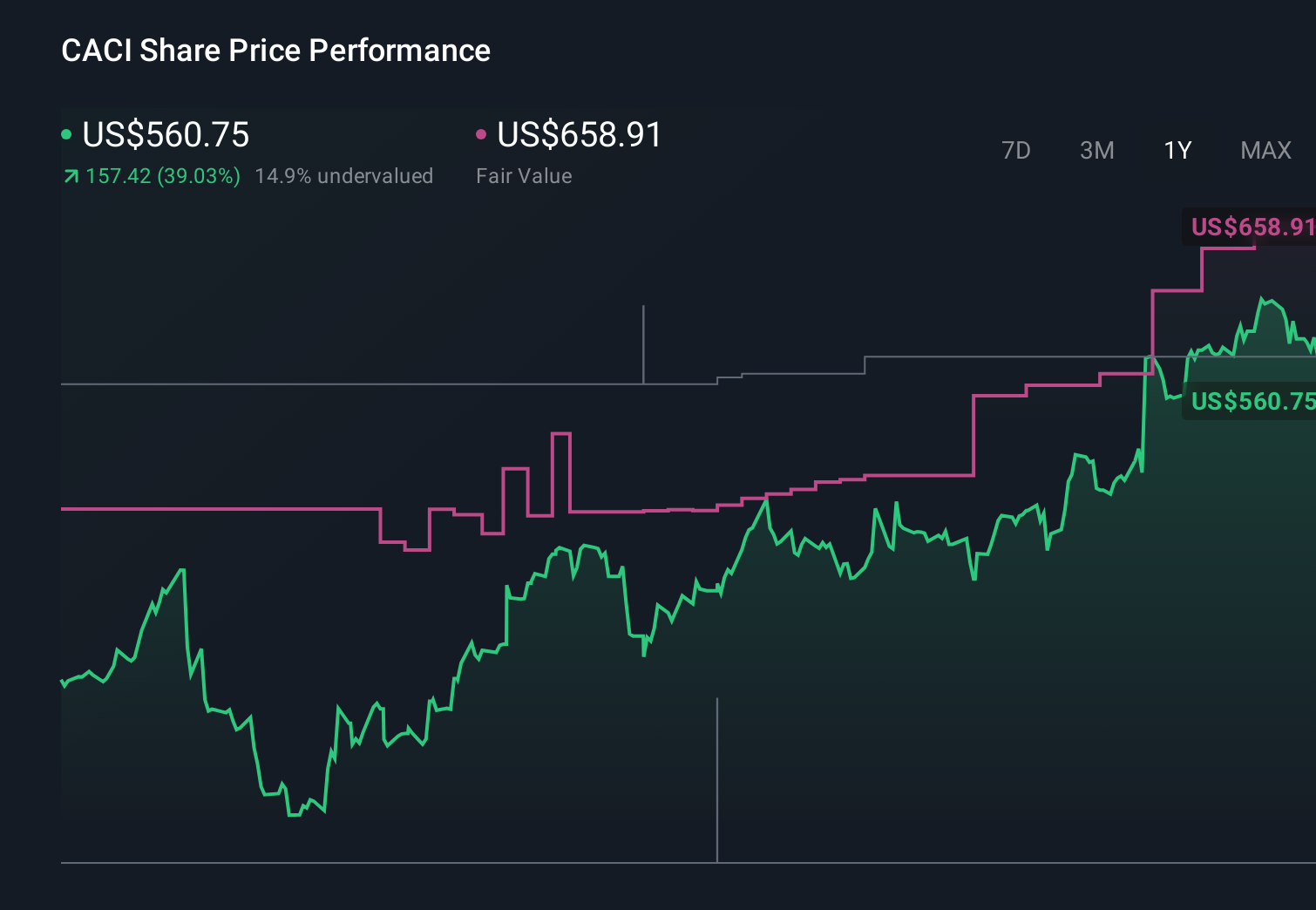

CACI International's narrative projects $11.9 billion revenue and $744.0 million earnings by 2029. This requires 10.0% yearly revenue growth and a $225.6 million earnings increase from $518.4 million today.

Uncover how CACI International's forecasts yield a $709.23 fair value, a 44% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected CACI to reach about US$12.9 billion in revenue and roughly US$745 million in earnings, so this Navy win may prompt them to revisit whether contract consolidation is a powerful tailwind or whether rising automation and commercial software preferences could still limit how much upside is realistically on the table.

Explore 3 other fair value estimates on CACI International - why the stock might be worth just $709.23!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your CACI International research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free CACI International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CACI International's overall financial health at a glance.

No Opportunity In CACI International?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

- Rare earth metals are the new gold rush. Find out which 28 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.