News Corp (NWSA) Q2 Net Income Rebound Tests Bullish Earnings Narratives

News Corporation Class A NWSA | 25.33 | +1.20% |

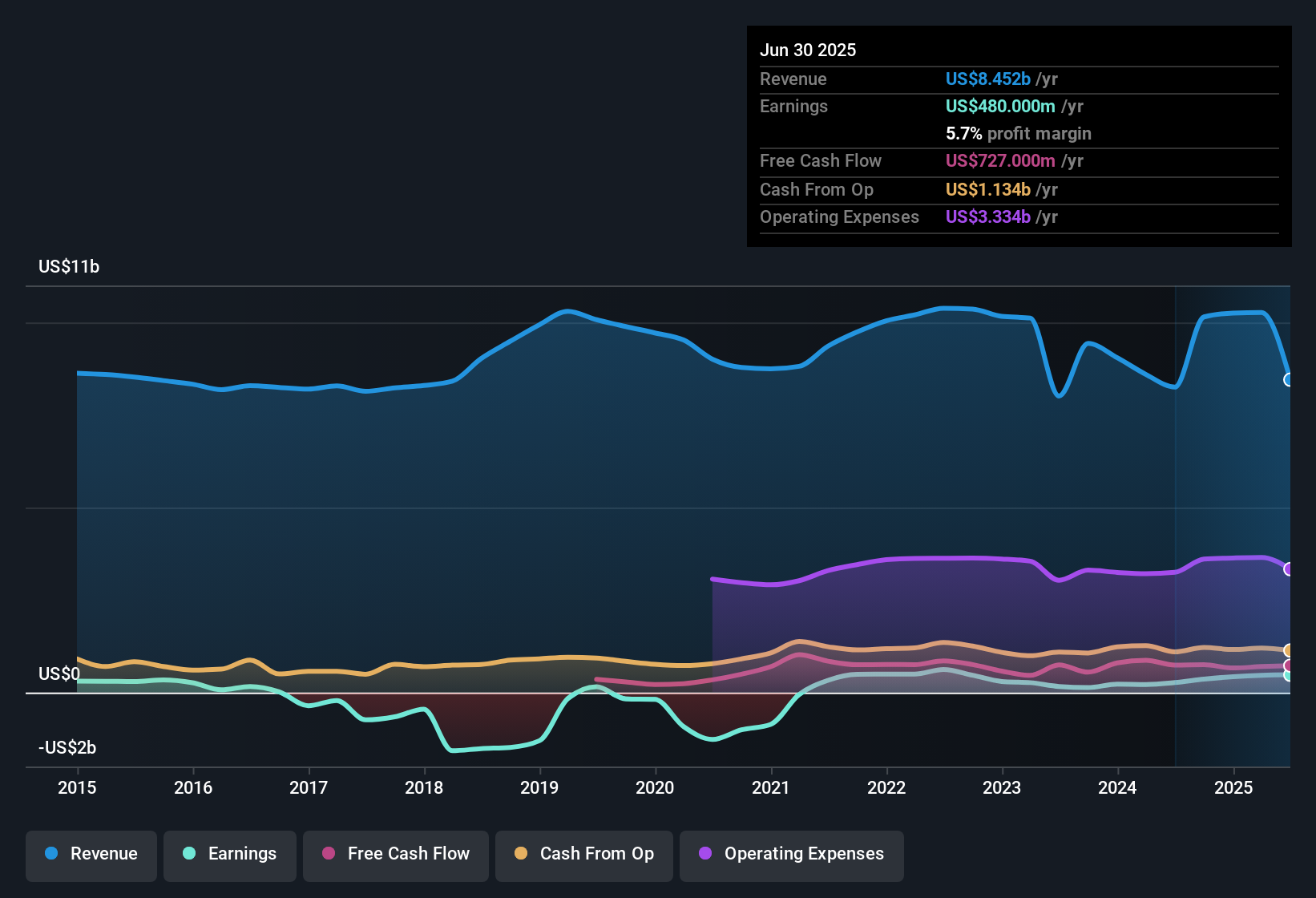

News (NWSA) opened Q2 2026 with total revenue of US$2.4b and basic EPS of US$0.34, alongside trailing twelve month revenue of US$8.6b and EPS of US$0.78 that frame the latest quarter against a wider run rate. The company has seen quarterly revenue move from US$2.1b in Q2 2025 to US$2.4b in Q2 2026, while basic EPS shifted from US$0.40 to US$0.34 over the same period. This sets up a read across between top line resilience and more mixed earnings per share trends as you think about how its 5.1% net margin fits into the story.

See our full analysis for News.With the headline numbers on the table, the next step is to set these results against the most widely shared narratives about News to see which views line up with the data and which ones the latest margin profile starts to question.

Q2 profit of US$193 million puts earnings on a steadier base

- News booked net income from ongoing operations of US$193 million in Q2 2026, up from US$112 million in Q1 2026 and higher than the US$81 million to US$118 million range seen in Q3 2025 to Q1 2025.

- What stands out is how this steadier profit base compares with past narrative focus on one off items, because:

- Trailing twelve month net income from continuing operations sits at US$439 million alongside US$712 million from discontinued operations, so the current quarter shows earnings without relying on those discontinued gains.

- Trailing EPS of US$0.78 sits below the earlier US$0.85 level, which keeps the bullish view in check even as Q2’s profit looks more grounded in the core business.

Curious how these numbers fit into the bigger story for News? 📊 Read the full News Consensus Narrative.

EPS trend steadies after a volatile year

- Basic EPS for the last four quarters ran at US$0.20, US$0.34, US$0.09 and US$0.14, so Q2’s US$0.34 sits near the top of the recent range and against trailing twelve month EPS of US$0.78.

- Supporters of a more optimistic view point to earnings forecasts of about 12.7% a year, and the historical 20.7% yearly EPS growth over five years, yet the numbers here also show:

- Trailing twelve month earnings only grew 1.9% over the past year, which is well below that 20.7% five year pace that bullish investors often highlight.

- With quarterly EPS swinging between roughly US$0.09 and US$0.40 in the past six reported quarters, the recent forecast growth story leans on smoothing out those ups and downs over time.

High P/E and modest margin keep valuation questions alive

- The shares trade around US$22.50, which is about 7.4% below a US$24.29 DCF fair value while sitting on a trailing P/E of 28.4x, compared with 14.8x for the US media industry and 18.1x for peers, on a net profit margin of 5.1%.

- Critics focus on that rich P/E relative to peers, and the data gives them a few anchors:

- Analysts’ implied upside of roughly 54.7% and the 3.7% revenue growth forecast rely on earnings growing faster than sales, which is a tall order with a current 5.1% margin that is not higher than last year in the dataset.

- The stock trading only modestly below the DCF fair value, despite the margin and 1.9% trailing earnings growth, suggests investors are already paying up for those forecast earnings improvements.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on News's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

Explore Alternatives

Q2’s rich 28.4x P/E on a 5.1% net margin, with only 1.9% trailing earnings growth, raises questions about paying up for this earnings profile.

If that mix of modest earnings momentum and a premium price makes you cautious, check out 53 high quality undervalued stocks that aim to pair stronger value signals with more attractive entry points.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.