NextEra Energy (NEE) Stock Weighs Dominion Merger Hopes Against Conflicting Valuation Signals

NextEra Energy, Inc. NEE | 0.00 |

- If you are wondering whether NextEra Energy is priced fairly today, the key question is how its current share price lines up with its underlying value.

- The stock last closed at US$86.43, with returns of 0.2% over 7 days, a decline of 2.4% over 30 days, a 6.8% gain year to date, and gains of 24.6%, 27.8% and 33.1% over the past 1, 3 and 5 years respectively. These figures may have changed how investors think about its risk and return profile.

- Recent news around utilities, renewable energy policy, and interest rate expectations has kept investor attention on companies like NextEra Energy. This backdrop helps explain why the stock's moves have been closely watched, as market participants weigh long term growth drivers against funding costs and regulatory trends.

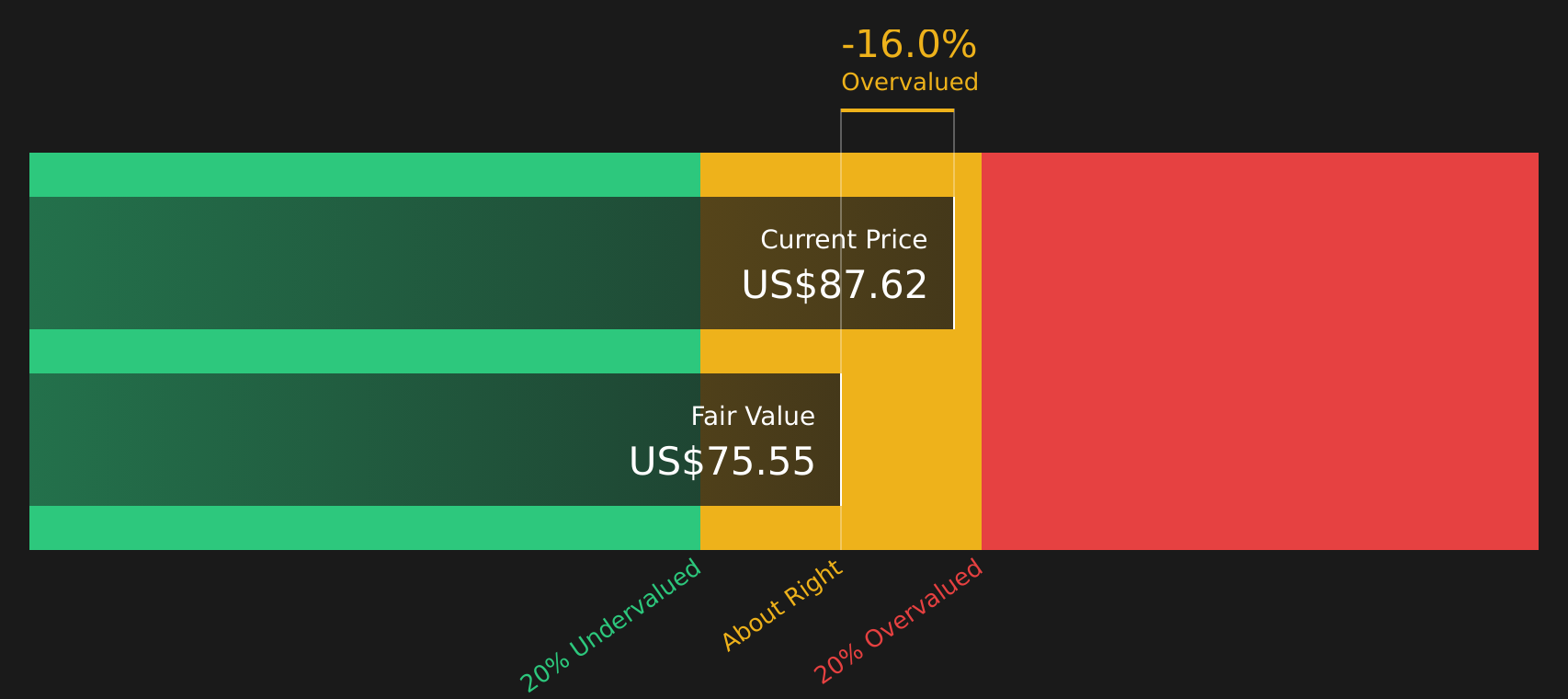

- NextEra Energy currently has a valuation score of 2 out of 6, which reflects how many of Simply Wall St's valuation checks suggest the stock is undervalued. This sets up a closer look at methods like discounted cash flow, multiples and dividends, with an even more holistic way to think about valuation at the end of this article.

NextEra Energy scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: NextEra Energy Dividend Discount Model (DDM) Analysis

The Dividend Discount Model estimates what NextEra Energy stock could be worth by projecting future dividend payments and discounting them back to today. It focuses on how quickly dividends might grow and whether that growth looks sustainable.

For NextEra Energy, the model uses a current annual dividend per share of about US$2.71, a return on equity of 9.89% and a payout ratio of roughly 59.47%. Dividend growth in the model is capped at 3.54%, slightly below the 4.01% rate implied by the inputs, with an expected longer term growth assumption of 4.01%. This is intended to keep the projection more conservative while still reflecting ongoing dividend increases.

Using these inputs, the DDM arrives at an estimated intrinsic value of US$75.82 per share. Compared with the recent share price of US$86.43, the model indicates the stock is about 14.0% above this dividend-based estimate. On this metric alone, the stock appears overvalued.

Result: OVERVALUED

Our Dividend Discount Model (DDM) analysis suggests NextEra Energy may be overvalued by 14.0%. Discover 44 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: NextEra Energy Price vs Earnings

For profitable companies like NextEra Energy, the P/E ratio is a commonly used yardstick because it links what you pay for the stock to the earnings it currently generates. It gives you a quick way to compare how the market prices each dollar of profit across different utilities.

What counts as a “normal” or “fair” P/E depends on how the market views a company’s earnings growth potential and its risk profile. Higher expected growth or lower perceived risk can support a higher P/E, while lower growth expectations or higher risk usually justify a lower one.

NextEra Energy trades on a P/E of about 22.0x, which is close to both the Electric Utilities industry average of around 21.6x and a peer average near 22.3x. Simply Wall St also calculates a proprietary “Fair Ratio” of 26.9x for NextEra Energy, which reflects factors such as its earnings growth profile, industry, profit margins, market cap and risk characteristics. This Fair Ratio can be more informative than simple peer or industry comparisons because it adjusts for company specific fundamentals rather than assuming all utilities deserve the same multiple. Since the Fair Ratio of 26.9x is meaningfully above the current P/E of 22.0x, the stock appears undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your NextEra Energy Narrative

Earlier the DDM and P/E checks gave you two different answers for NextEra Energy, so this is where Narratives come in as a simple way to connect your view of the company’s story with a set of financial forecasts and a Fair Value that you can compare with the current share price.

A Narrative on Simply Wall St is your story for a stock. You set assumptions for future revenue, earnings, margins and the P/E you think is reasonable, then let the platform turn that story into a Fair Value estimate on the Community page that is used by millions of investors.

Because Narratives are tied to live company data, they are refreshed when new information comes through, such as merger news, data center power deals or earnings. Your Fair Value can move as the facts change rather than staying frozen in time.

For NextEra Energy, one investor might build a Narrative around the Dominion merger, AI data center demand and a Fair Value near US$112.00. Another might focus on regulatory and financing risks and arrive closer to US$72.89. Comparing each Fair Value with the current share price then helps each investor decide whether the stock looks attractive, expensive or somewhere in between on their own terms.

For NextEra Energy however we will make it really easy for you with previews of two leading NextEra Energy Narratives:

Fair Value: US$98.55 per share

Implied discount vs recent price: about 12.3% below this fair value

Revenue growth assumption: 11.89% a year

- Focuses on the Dominion merger, AI data center power demand and a large renewables and storage backlog as key supports for higher long term earnings.

- Assumes continued legislative support, a growing regulated rate base at Florida Power & Light and ongoing capital investment as anchors for relatively stable cash flows.

- Highlights risks from tax credit phase downs, higher financing costs and regulatory or permitting delays that could temper margins or slow some projects.

Fair Value: US$72.89 per share

Implied premium vs recent price: about 18.6% above this fair value

Revenue growth assumption: 4.95% a year

- Emphasizes the impact of expiring renewables tax credits, higher interest costs and stricter permitting on the economics of NextEra Energy's future projects.

- Flags the growth of distributed energy resources, high debt levels and a slower outlook at Florida Power & Light as potential constraints on earnings and dividend growth expectations.

- Accepts that long term electricity demand and existing renewable assets are valuable, but argues that merger approval risk and valuation sensitivity could limit upside.

These two Narratives give you structured, data backed paths to think about NextEra Energy, whether you lean toward the more optimistic or more cautious view. You can adjust the assumptions to match your own expectations before comparing the resulting Fair Values with the current share price. To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for NextEra Energy on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for NextEra Energy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.