NIKE (NKE) Slides As Brand Strength Narrative Keeps Valuation In Question

NIKE, Inc. Class B NKE | 0.00 |

NIKE (NKE) stock has come under pressure recently, with the share price down 6% over the past month and 20% over the past 3 months. This has prompted investors to reassess the company’s current valuation.

Looking beyond the recent pullback, NIKE’s share price return is down 33.91% year to date and the 5 year total shareholder return is down 70.60%. This points to fading momentum as investors reassess growth prospects and risk.

If NIKE’s recent slide has you reassessing your watchlist, this can be a good moment to broaden your search and check out 20 top founder-led companies

With NIKE’s share price under pressure and the stock trading below some analyst targets, the key question is straightforward: is this a reset that leaves NIKE undervalued, or is the market already pricing in its future growth?

Most Popular Narrative: 2.8% Undervalued

Based on the most followed narrative, NIKE’s fair value sits at $43.01, slightly above the last close at $41.82. This frames the current pullback as modestly undervalued according to that model.

Nike (NKE) is a well-positioned company with a globally recognized brand and a dominant market presence, with $101.5 billion in market cap. As the industry leader, Nike benefits from significant economies of scale, allowing it to negotiate favorable terms with suppliers and maintain cost efficiency.

Want to see what kind of revenue growth, margins, and future earnings multiple DS2invest plugged in to reach that fair value for NIKE? The narrative leans on brand strength, direct to consumer expansion, and capital returns to back its valuation case. The exact mix of assumptions is where the story really gets interesting.

Result: Fair Value of $43.01 (UNDERVALUED)

However, there are clear risks to that NIKE narrative, including pressure on margins if costs rise, as well as the possibility that direct to consumer efforts underwhelm expectations.

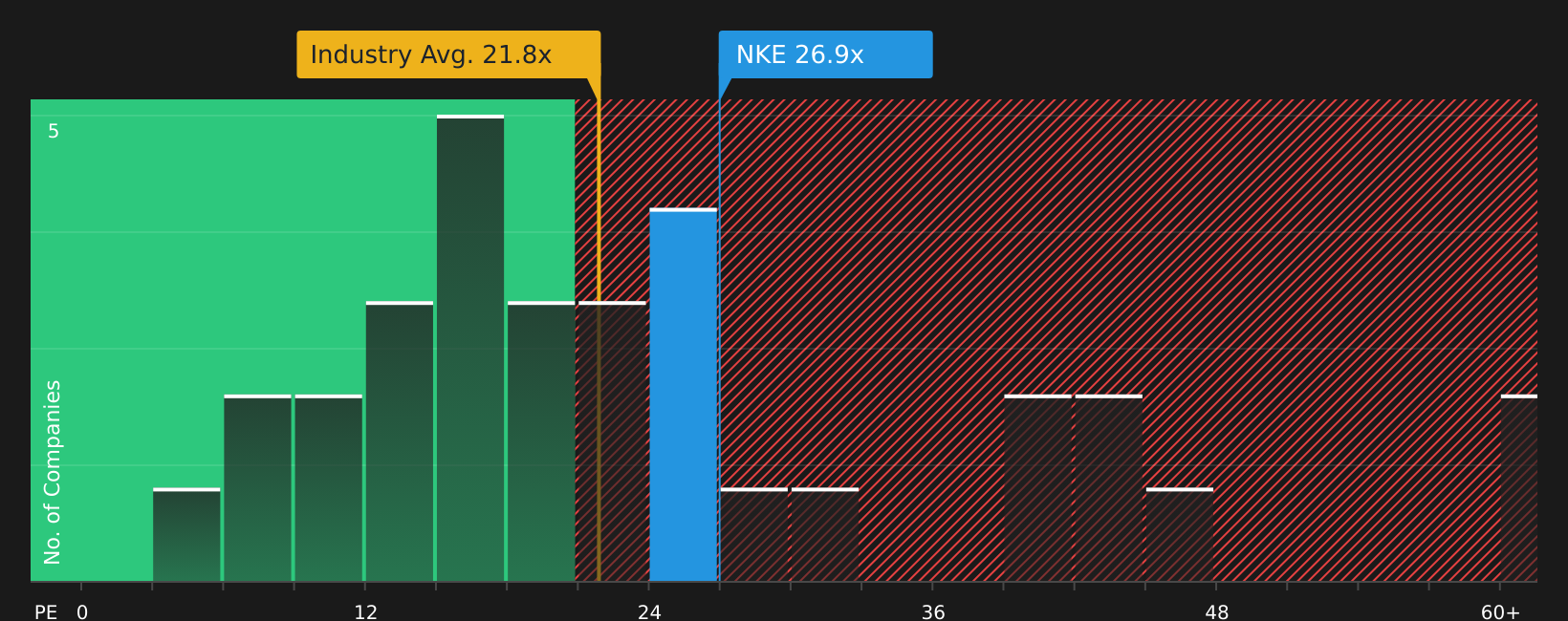

Another View: NIKE Through the P/E Lens

While the narrative and SWS DCF model view NIKE as about 4.6% undervalued, the picture looks more mixed when you look at the P/E ratio. At 27.5x earnings, NIKE trades above the US Luxury industry at 22.6x, slightly below peer average at 28.8x, and under its 29.5x fair ratio.

That combination suggests some valuation pressure from the wider industry, along with a small cushion versus peers and the fair ratio that the market could move toward over time. The key question is whether you see that gap as downside risk or room for re rating.

Next Steps

If the mixed sentiment around NIKE has you on the fence, take a closer look at the full picture of risks and rewards so you can move quickly and shape your own view with 2 key rewards and 2 important warning signs

Looking for more NIKE investment ideas?

If NIKE has your attention but you want a fuller opportunity set, do not leave potential standouts on the table when a few minutes of smart screening can broaden your options.

- Target potential upside by reviewing companies that our screener tags as attractively priced with strong fundamentals using 44 high quality undervalued stocks.

- Strengthen your income game by focusing on stocks with substantial yields and resilient payouts highlighted in the 7 dividend fortresses.

- Lower the stress in your portfolio by concentrating on companies that carry stronger risk profiles surfaced through the 69 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.